First, to state right up front, it’s been well over a year since we have shorted the financials. Currently, the XLF is the only sector in the market not trading above the TAIL line (three years or less). As steep as the yield curve looks right now and as good as the ted spread looks – this is, by definition as good as it gets for credit and the financials.

On top of all this, the dollar is teetering on a major breakdown below the 78 line. The dollar is currently down 12% since March – we call that a crash. We view the XLF as the most politically compromised sector in the market because financials have the most political dependence, which helps to fix the earnings power of the industry. What the government giveth, it can also take away!

Last week, Ben Bernanke proved to the world that he is staying with his politicized strategy by keeping the low end of the curve at 0%. As the rest of the world moves on from the financial crisis, there are many countries that may not invest in the politically compromised U.S. Financial services industry. This fits our thesis of “buy what china needs and not what we want them to need.” The US government wants China to buy US dollars and US treasuries, but our belief is that China’s central bankers will decide that they need to diminish their exposure, a conclusion that will be made easier by the politics of the situation.

Provided that we keep the low end of the curve at 0% in the US, there is no incentive to save in this country, and economics 101 has taught us that savings need to equal investment over time. Investment is perpetuated by a country that has cash and savings – think China (although it’s easy to hoard when all property and income belongs to the state).

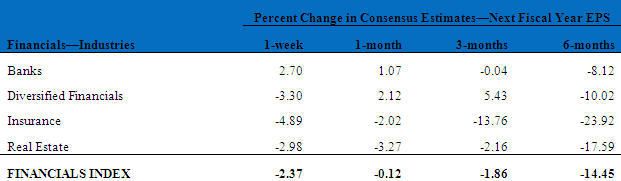

The bulk of the XLF is made up of the Diversified Financials (55%), which include the industry heavy weights JPM, BAC, GS and MS. Banks make up 20% of the ETF with Insurance and Real Estate companies accounting for the balance.

The earnings trends for the Real Estate and insurance companies have been disastrous all year and did not find much support going into 2Q earnings season. The Banks, those best levered to taking advantage of the steep yield curve, have shown the most positive earnings revisions trends of the past week and month. Overall however, earnings revisions for the XLF continue to be negative.

Since the XLF bottomed on March 5th, 2009 at $6.24, we have seen a generational short squeeze that most investment managers missed. The XLF has rallied +102% largely on the back of a massive recovery in earnings sponsored by the US taxpayer. As you can see in the chart below, earnings for the XLF declined significantly in 2H08, have since recovered in 1Q09 and continue to improve in 2Q09. While 2Q09 was strong for the financials, it appears that the bulk of the earnings recovery is behind us as there was a sequential deceleration in improvement. Going forward, the pace of sequential improvement in the XLF EPS will continue to slow, declining to 9% in 4Q09. These estimates are based on a compromised yield curve. If our 4Q inflation call proves to be correct, interest rates are headed higher. What will happen to Q4 numbers if the yield curve flattens?

It is our conclusion that things can only go downhill from here for the majority of the financial sector for the immediate and intermediate duration. As always, we are data dependent and will be testing our thesis as new data emerges.

Howard W. Penney

Managing Director