We are adding BOBE to the Hedgeye Best Ideas list as a LONG.

We have followed BOBE on and off over the years, but have never really gotten behind the story – until now. The restaurant industry has always been fertile ground for activists, but the level of activism has never been more rampant. In the past year alone, we've seen CBRL, DAVE, DRI, BJRI and BOBE attract largely uninvited attention from these investors.

We'll start off by saying that we have a ton of respect for the work Sandell Asset Management has done in the restaurant space over the years. Their recent slide deck on Bob Evans Farms is downright epic. It's the complete unveiling of a company plagued with so many issues that it is difficult to believe it has gone on for so long.

We believe that Sandell will be successful in getting control of the board and creating significant value for shareholders.

As you know, we are big supporters of change at DRI and feel that BOBE is in a very similar situation. BOBE, much like DRI, is a stodgy old company that has flown under the radar for far too long. In our view, both have multi-year histories of mismanagement evidenced by inappropriately bloated cost structures and considerable real estate exposure.

Unfortunately for these two aforementioned laggards, the era of unaccountability has passed. Interestingly, the first Bob Evans restaurant was opened in 1961 just seven years prior to opening of the first Red Lobster restaurant in 1968. Indeed, these two concepts have stood the test of time, but the times have changed – and so must they.

The similarities between DRI and BOBE are striking:

- Combined Chairman and CEO position

- Stale and entrenched Board of Directors

- New, opulent headquarters

- Corporate plane

- Excessive G&A spending

- Significant non-core business

- Inefficient remodel program

- Lackadaisical management

To summarize, both of these businesses have been woefully mismanaged. We believe that is set to change.

We have spent a significant amount of time working through Sandell’s investment thesis and concur with the vast majority of their conclusions. Having said that, we’d like to run through our thesis, which is similar to Sandell’s, but comes with a bit of a twist and centers on four critical themes:

- Separating the foods business from the restaurant business

- Improving store operating performance by moving to an asset light model

- Scrutinizing capital allocation and cutting the bloated cost structure

- The real estate opportunity

BOBE OVERVIEW

- Bob Evans was founded in 1948, when the company’s namesake began making sausages on his farm in southeastern Ohio. The business was incorporated in Ohio in 1957 and became publicly traded in 1963.

- Bob Evans Farms Inc. operates in two primary business segments: Bob Evans Restaurants and Bob Evans Farms Foods (“BEF Foods”).

- Bob Evans Restaurants owns and operates 562 full-service restaurants in 19 states across the United States, primarily in the Midwest, mid-Atlantic, and Southeast.

- BEF Foods produces and distributes a variety of refrigerated and frozen food items to more than 30,000+ retail locations across the United States and Mexico.

THE BOBE TIMELINE

If you haven’t been following the Bob Evans / Sandell saga closely, we suggest you begin to. We like Sandell’s relentless resolve and believe they have identified several, feasible opportunities to unlock shareholder value. As such, we believe BOBE represents an attractive entry point on the long-side for investors that don’t mind seeking strong returns from special situations. Before we run through our analysis, we thought it’d be helpful to provide a brief timeline of events below.

January 28, 2013 – Bob Evans Announces Agreement to Sell Mimi’s Cafe

After several years of underperformance, Bob Evans announces an agreement to sell Mimi’s Café to LeDuff America for $50 million. BOBE purchased the French-inspired casual dining restaurant for $183 million back in 2004. Under Bob Evans watch, Mimi’s Café hadn’t recorded an increase in same-store sales since 2005. SEC Filing

July 16, 2013 – Sandell’s Initial Discussion with CEO Steven Davis

August 5, 2013 – Sandell Reaches Out to Lead Independent Director

Sandell sent a letter to Lead Independent Director, Michael Gasser, discussing key matters and potential ways to unlock significant shareholder value.

August 19, 2013 – BOBE Announces Incremental $150 Million Share Repurchase Authorization

In the August 19th earnings release, Bob Evans announced an incremental $150 million share repurchase authorization. However, to Sandell’s dismay, the release made no other mention of the key matters addressed in its recent letter to Mr. Gasser. SEC Filing

September 23, 2013 – Sandell Recommends the Sale of BEF Foods

Sandell Asset Management, 5.1% owner of Bob Evans at the time, sent a letter to the company’s Board of Directors recommending the separation of BEF Foods through a sale or a spinoff. The activist also recommended management consider conducting a substantial sale-leaseback and implementing an aggressive share repurchase program. Sandell released a comprehensive investor presentation, highlighting its strategy to unlock significant shareholder value. Sandell estimated the stock would be worth $73 - $84 per share if its recommendations were put into action. The activist also called the recent four-year extension of Chairman and CEO Steven Davis an “ill-justified reward” for overseeing years of mismanagement and underperformance. SEC Filing; Sandell Presentation

October 11, 2013 – Sandell Holds Discussion with Mr. Davis and CFO Paul Desantis

Mr. Davis assured Sandell the Board would review their ideas in “due time.”

November 11, 2013 – Sandell Launches Proxy Fight

Sandell announced it retained a proxy solicitation firm, MacKenzie Partners. In the filing, Sandell noted it was “profoundly concerned by the Board’s lethargic approach to taking action to enhance shareholder value” and criticized the Board for its apparent indifference. Sandell cited its intent to explore a consent solicitation in order to seek change. SEC Filing

December 4, 2014 – Dismissive Comment by CEO Davis on 2QF14 Earnings Call

In his comments, Mr. Davis rebuffed Sandell’s three principal ideas including its call for a sale leaseback, a spinoff of BEF Foods and accelerated share repurchases. Transcript

December 9, 2013 – Sandell Announces Intent to Commence a Consent Solicitation

Sandell, owner of 6.5% of BOBE at the time, released a letter stating its intention to seek a consent solicitation. In the letter, the activist claimed it has been met with “near indifference” by management and the Board of Directors. Sandell also denounced the Board for its “history of inaction” and highlighted what it believes to be the “strategic irrationality” of operating a restaurant and packaged foods business under the same corporate umbrella. SEC Filing; Sandell Presentation

January 14, 2014 – Sandell Sues Bob Evans

Sandell filed a lawsuit against Bob Evans after the Board of Directors voted to require a supermajority (80% of shareholders) to make bylaw changes. This change came back in 2011, just three months after shareholders voted to reduce the company’s bylaws to only require a simple majority to affect change. In a separate lawsuit, the Oklahoma Firefighters Pension & Retirement System also accused Bob Evans of raising the threshold for bylaw changes without the approval of, and against the desire of, shareholders. SEC Filing

January 28, 2014 – Bob Evans Amends Bylaws

Facing significant legal pressure, the Board of Directors amended Bob Evans’ bylaws to allow a simple majority of shareholders the ability to affect change. The company also revealed in a press release that one, and up to three, new independent directors would be appointed to the Board prior to the 2014 Annual Meeting. SEC Filing; Amended Bylaws

January 29, 2014 – Sandell Comments On Reversal, Blasts Board

Sandell publicly announced that it was pleased with the Board’s decision to reverse an ill-advised bylaw amendment and planned to withdraw its lawsuit. Despite this, Sandell went on to voice its continued displeasure with the highly conflicted Board, referring to it as “one of the most insidious examples of cronyism demonstrated by a publicly-traded company.” SEC Filing

February 25, 2014 – Industry Expert Becomes Critical of BOBE

Jonathan Maze of Restaurant Finance Monitor wrote an article criticizing the way Bob Evans has dealt with Sandell Asset Management. The article features Chris Davis, chair of the Investor Activism Group for Kleinberg, Kaplan, Wolff and Cohen, who had the following to say about the Board’s dismissive tactics: “That is, in 2014, just an ill-advised play by management. To completely stonewall an activist is the height of poor judgment.” Article

April 24, 2014 – Sandell Nominates Eight Independent Directors

Sandell released a letter in which it identified and nominated eight independent candidates to Bob Evans’ Board of Directors. The nominations include a wide range of talented, proven leaders with varying specialties:

- Doug Benham: Former President and CEO of Arby’s Restaurant Group

- Charles Elson: Director of the John L. Weinberg Center for Corporate Governance at the University of Delaware

- David Head: Former President and CEO of O’Charley’s Inc.

- Steve Lynn: Former Chairman and CEO of Sonic Corporation

- Annelise Osborne: Senior Credit Officer at Moody’s Investor Service

- Aron Schwartz: Former Managing Director at Fenway Partners

- Michael Weinstein: Former CEO of Triarc Beverage Group (Snapple Beverage Group)

- Lee Wielansky: Chairman and CEO of Midland Development Group

Sandell also released its most comprehensive presentation yet, which highlights Bob Evans’ underperformance, the Board’s history of inaction and opportunities to unlock significant shareholder value. SEC Filing; Sandell Presentation

April 28 – BOBE Appoints Three New Board Members

Shortly after Sandell’s nominations to the Board, BOBE appointed the following individuals to its Board of Directors: Kevin Sheehan, President and CEO of Norwegian Cruise Line, Kathy Lane, former CIO of TXJ Companies and Larry McWilliams, Co-CEO of Compass Marketing. The company also announced the retirement of two long-standing directors, Larry Corbin and G. Robert Lucas and the resignation of West Virginia University President Gordon Gee. SEC Filing

April 28 – Sandell Responds to BOBE’s ‘Knee-Jerk Reactionary’ Moves

Sandell referred to the aforementioned Bob Evans’ announced as a “half measure,” stating it was taken as a “knee-jerk reactionary” response to significant outside pressure. In a press release, Tom Sandell delivered a damning interpretation of the move saying: “In our view, this is yet another cynical attempt by the Board of Directors of Bob Evans to pose as a Company that embraces good governance after forcing shareholders to suffer years of underperformance under the supervision of what we view as a stale and entrenched Board.” Sandell also stated that its nominees compare favorably to the three newly appointed Board members. SEC Filing

1. SPINOFF BEF FOODS

BEF Foods is a producer and distributor of pork sausage product and a variety of complementary home-style refrigerated side dishes and frozen food items primarily under the Bob Evans, Owens, and Country Creek brand names. These food products are distributed primarily to warehouses that distribute to grocery stores throughout the United States. Additionally, they manufacture and sell similar products to foodservice accounts, including Bob Evans Restaurants. Other restaurant operators are a negligible part of the business.

Importantly, the food processing business is linked to the founding of the company. Although we fully appreciate the desire to maintain tradition within a business, we believe this connection is severely limiting the company’s potential. By way of background, BOBE’s founder bought a farm in Rio Grande, Ohio many years ago and began making sausage for his family and friends. Before long, the response was so overwhelmingly positive that he needed to build a restaurant in order to accommodate everyone. Today, however, it is the unfortunate truth that BEF Foods’ connection to Bob Evans Restaurants represents a substantial burden to its operations. Major protein products traditionally sell seamlessly into the restaurant industry and tend to generate substantial revenue for the seller. However, in today’s world, very few, if any, restaurant companies are compelled to buy product from another restaurant company.

Other than the historic connection between BEF Foods and Bob Evans Restaurants, there are very few synergies between the protein business and the restaurant business. In fact, relative to the high return "asset light" restaurant business, food processors are low margin, highly volatile businesses that trade at compressed multiples. We also believe BEF Foods would fare better as an independent company, separate from the restaurant business. BEF Foods’ sales to the foodservice business (including other restaurants) only accounts for 20% of revenues. In FY13, the 10 largest customers represented approximately 60% of BEF Foods’ total revenues. The top two customers represented approximately 30% of BEF Foods’ revenues.

In our opinion, there is substantial room for BEF Foods to grow and the potential to increase sales in foodservice while further diversifying the customer base more than justifies a separation of the business.

2. TRANSITION TO AN ASSET LIGHT MODEL

Bob Evans’ significant real estate holdings give management the ability to convert to an asset light model in order to significantly enhance shareholder value. In the restaurant industry, there have been a number of public companies that have pioneered such a transition. We point to JACK as the most recent success story, but numerous others have successfully sold restaurant assets as well.

Two direct competitors in the family dining segment, Denny’s (DENN) and IHOP (DIN), are nearly 100% franchised. Burger King (BKW) has also made an aggressive push to an asset light model in order to generate substantial value for shareholders.

In the restaurant space, franchisees have been known to run restaurants better than the franchisors running the brand. We don’t see why this would be different in the case of BOBE and believe there would be a significant appetite to sell off large blocks of stores.

Finding a few strong franchisee partners would help the Bob Evans brand effectively address some of the operational issues facing the company – and there are plenty. For one, the average check is far too high. Average per-guest checks in FY13 for breakfast, lunch and dinner were $8.47, $9.24 and $9.07, respectively. While we assume BOBE has some loyal breakfast customers, the $9.24 average lunch check is not nearly competitive enough in today’s restaurant environment. The big national casual dining chains are currently promoting $6-7 lunch price points on national TV.

On the most recent DENN earnings call, CEO John Miller spoke to this process in working with franchisees when he said, “We will continue to work closely with our franchisees in identifying opportunities to reinforce the traffic and frequency driving aspects of the $2, $4, $6 and $8 Value Menu, while continuing to look for ways to improve food costs, margins, flow-through and ultimately store level profits.”

Notably, private equity restaurant acquisitions approched record levels in 2013 and are off to a fast start to-date in 2014. While some PE firms have been looking to harvest investments made over the past four years, others have become increasingly active in purchasing franchisee operations. Acquiring franchisees lets the firms focus on restaurant-level execution rather than running an entire chain’s operations and allows them to benefit from significant cash flows.

Second, selling off a number of stores in the Midwest will diversify the revenue stream and should help BOBE demand an improved valuation. An overwhelming majority of restaurants are located in Ohio and other parts of the Midwest. More specifically, BOBE has 241 or approximately 43% of its restaurants located in Michigan and Ohio.

In an asset light model, we believe BOBE would be able to collect as much as 10-12% of revenues in rent and royalty on a per-store basis. This compares favorably to the current 7% operating margin. In addition, we estimate the company could generate $300-600 million pre-tax in asset sales. The cash generated would allow the company to reduce its current outstanding share count by 20-30%.

Changes of this magnitude will undoubtedly take time, but the numbers suggest the stock would see meaningful upside.

3. POOR CAPITAL ALLOCATION = DECLINING PROFITABILITY

Over the past year, management has ramped up capital spending to support a new remodel program coined “Farm Fresh Refresh.” The company has spent approximately $225,000 per store – and the results are nothing short of a disaster. As capital spending has increased, BOBE’s return on incremental invested capital has plummeted. This has resulted in a significant decline in the company’s profitability, best measured by net cash flow from operations versus net income. All things considering, we are comfortable saying the company is on a disastrous path.

4. REAL ESTATE

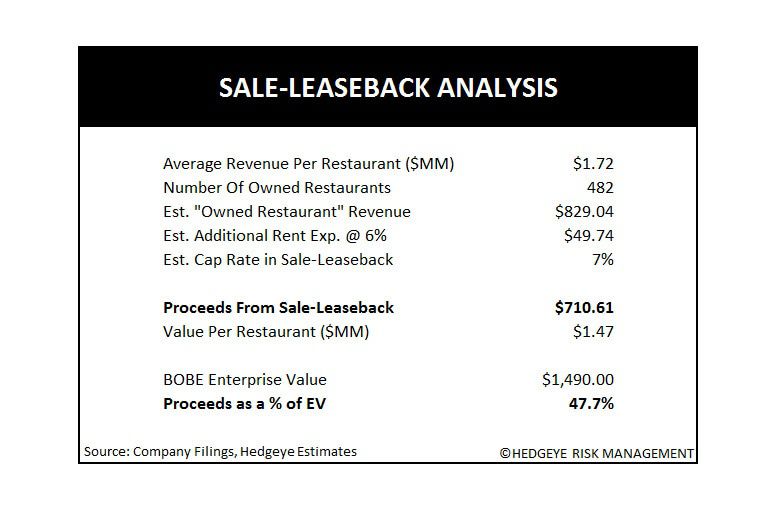

We outline our real estate analysis in the table below. Our valuation assumes an incremental rent expense equal to 6.0% of owned restaurant revenue that is capitalized at a 7.0% cap rate, which is conservative when compared to recent restaurant sale leaseback transactions.

We believe this $710.6 million estimate of BOBE’s real estate value is conservative, as it works out to $1.47 million per owned restaurant, which is significantly below the company’s stated cost to build a new restaurant.

Sentiment

We are surprised to see that sentiment has turned decidedly against Sandell. Since the beginning of the year, short interest has jumped from 6% to 12.9% as the sell-side has become increasingly bearish. We'll happily take the other side of that trade.

SUMMARY

To conclude, we believe there is significant value to be had for BOBE shareholders if Sandell's recommendations are implemented. In addition, we believe investors would be best served if BOBE were also to refranchise its restaurant business. Ultimately, we think Sandell's resolve will win out and believe the stock currently offers an attractive opportunity for investors with multi-year horizons to get long the name.

Howard Penney

Managing Director

Fred Masotta

Analyst