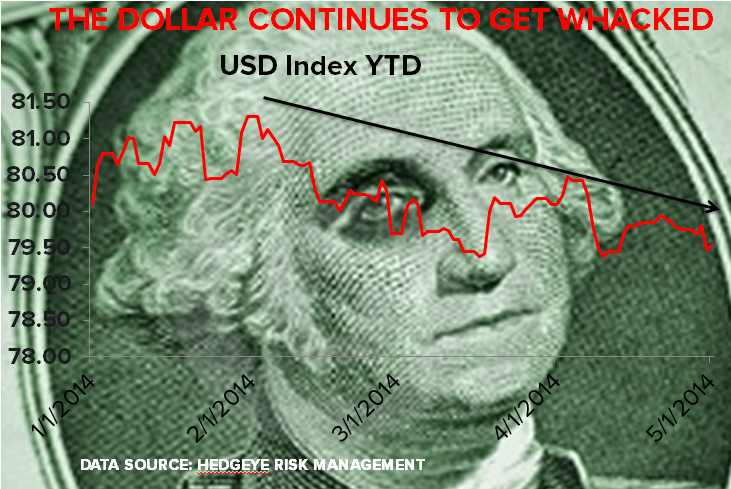

The US Dollar is on its knees (at year-to-date lows) following the massive 0.1% U.S. GDP miss. Incidentally, if all the so-called economic “weather experts” nailed the weather, why didn’t they nail this number?

Right now, it looks like both the currency and bond markets are front-running a Yellen “un-taper” in May. We shall soon see.