This note was originally published at 8am on April 17, 2014 for Hedgeye subscribers.

“Ambition is the germ from which all growth of nobleness proceeds.”

-Oscar Wilde

As an equity investor if you are early on growth in owning a stock, that is usually a very good thing. Parabolic growth can propel a stock to, as they say, “infinity and beyond.” On a macro level the same lesson applies. We’ve obviously been vocal and early on our view of growth slowing this year and the sub-sector performance of the SP500 has reflected that in spades.

On a more micro level, we’ve also been pretty negative on social media stocks, in particular Twitter (TWTR) and Yelp (YELP). Admittedly on Twitter, we were early as we were literally negative from the IPO, but as TWTR’s first earnings report showed us, expectations will eventually meet the gravity of reality.

In adding YELP to our Best Ideas list as a short, our timing has been much better. The key tenets of the short thesis on YELP are that customer attrition is a major issue, which no one is focused on, and also that the addressable market is much smaller than the management team is pitching to investors. The combination of attrition and a smaller market makes us believe that revenue growth will eventually disappoint. (If you’d like to get on the distribution list of Hesham Shabaan, who runs our Internet research team, please email sales@hedgeye.com.)

Even as we believe that certain social media stocks are getting ahead of themselves, it is hard to deny their ambitious growth. The boot strapping startup stories of the likes of Twitter and Facebook are worthy of admiration. In what direction these business models evolve will be the true test of longevity, but it is hard to deny the potential of a company like Facebook where 1/8 of the planet uses the application and 64% of users visit the site daily.

Another growth area we have been focused on has been electronic cigarettes, or e-Cigs. This has been reflected on our Best Ideas list with a long in Lorillard (LO). For the most part, LO is a boring tobacco stock, but has an underlying growth engine in its e-Cig business, which makes its growth prospects much more exciting. Although, admittedly, it is hard to call this noble growth.

The research on e-cigs naturally led us to also look at the burgeoning medical marijuana market. In states that have recently legalized marijuana it has been a boon to state tax coffers and to the extent that this legalizing expands, it is likely that tobacco companies enter the field. But before we dive into research and start doing calls on the topic, we’d like to get your view.

In our poll of the day that will circulate later today, we will be asking the question: Would you invest in a company that produces medical marijuana? We look forward to your responses and in getting the crowds view on whether medical marijuana is noble growth.

Back to the Global Macro Grind . . .

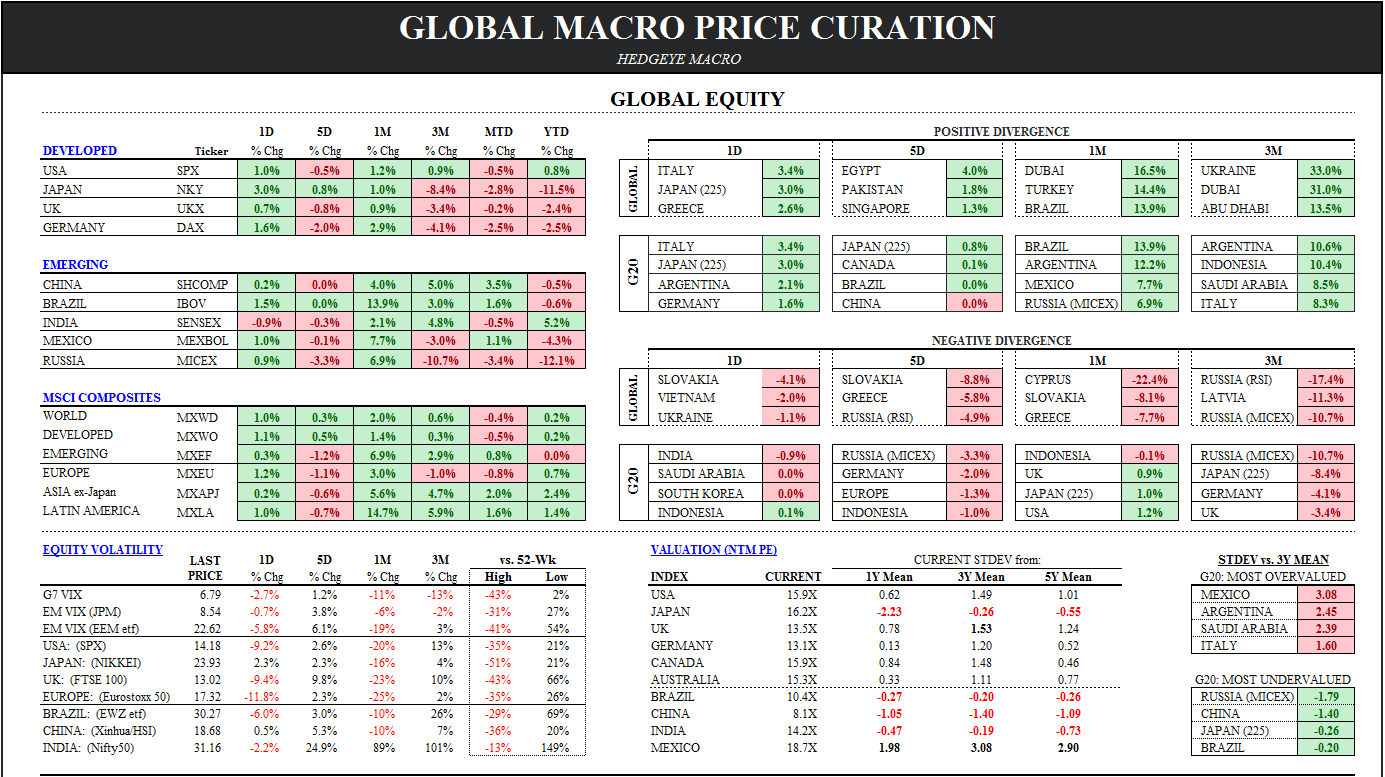

Heading into the long weekend, many business people and investors will be taking stock of the score in the year-to-date. In the chart of the day, we have attached one of a number of the quant screens that we circulate internally daily that show relative asset class performance.

One interesting chart looks at P/Es for countries versus their 3-year mean. Based on that metric the three most overvalued countries are Mexico, Argentina, and Saudi Arabia. Meanwhile, the three most undervalued are Russia, China, and Japan. There is some global macro performance to be found in that group to be sure!

Speaking of performance, it likely has not been a great year for the average long only fund as the SP500 is up a dreary +0.75% (certainly much different than what the Barron’s round table projected to start the year) and the hedge fund industry hasn’t fared much better. According to data from Preqin, the average hedge fund returned 1.23% in Q1, which is the worst start since 2008.

Interestingly, the one strategy that has worked well is activist investing. According to the same data, activist funds on average were up 3.3% in Q1. We have also been very vocal on one major activist name, the restaurant behemoth Darden (DRI). And this may fall in the category of growth that isn’t noble as well, but you should expect to see more activist ideas come from us as the year continues.

As we noted earlier, based on a comparison to the 3-year mean in forward P/E, Japanese equities are screening as cheap. The question that arises is whether Japan is cheap for a reason. Certainly, one potential negative catalyst for Japan is the VAT tax. March department store sales were up an astonishing 25.4% year-over-year in March ahead of the VAT tax that was implemented on April 1st.

Meanwhile, despite buying a lot, the confidence of consumers in Japan actually declined in March. According to the Japanese consumer confidence index, confidence declined to 37.5 in March from 38.5 in February. Clearly not an earth shattering breakdown in confidence, but likely a leading indicator of future declines now that the VAT tax is in place.

Clearly, the Japanese policy makers are going to have some interesting decisions to make in coming months and most of them are unlikely to bode well for the Yen. Japanese leadership may be wise to consider the words of Nascar legend Dale Earnhardt:

“You win some, lose some, and wreck some”

Ultimately, Japanese policy makers will have to decide whether growth by devaluation is truly noble growth.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1811-1881

Nasdaq 3959-4203

Nikkei 13699-14598

USD 79.11-80.03

EUR/USD 1.37-1.39

Nat Gas 4.49-4.72

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research