SUMMARY BULLETS

- 1Q14 FAIRLY STRONG...AT FACE VALUE: YELP beat revenues by $1.5M, Showing relatively strong growth across all its major cohorts. Additionally, its "customer repeat rate" hit a new high

- UNDER THE HOOD: 1Q14 marks YELP's smallest top-line beat since 3Q12. 2Q Guidance calls for marked deceleration in revenue growth. More importantly, It's customer repeat rate is misleading, and is somewhat distorted. Net-net, new account growth is slowing, while its attrition rate is not improving.

- HEADS THEY LOSE, TAILS THEY LOSE: We expect YELP's attrition rate to accelerate alongside slowing new account growth in 2014. The 1Q print didn't show us anything to suggest otherwise. If not, it just creates a more challenging setup for 2015. The stronger 2014, the more bearish we become for 2015. See notes below for more detail.

1Q14 fairly STRONg...at face value

At face value, everything looked good.

- Revenues: YELP beat revenue estimates by 1.5M, ahead of its 1Q14 guidance by $2.5M at the midpoint. Raised 2014 Revenue Guidance by $10M at the midpoint.

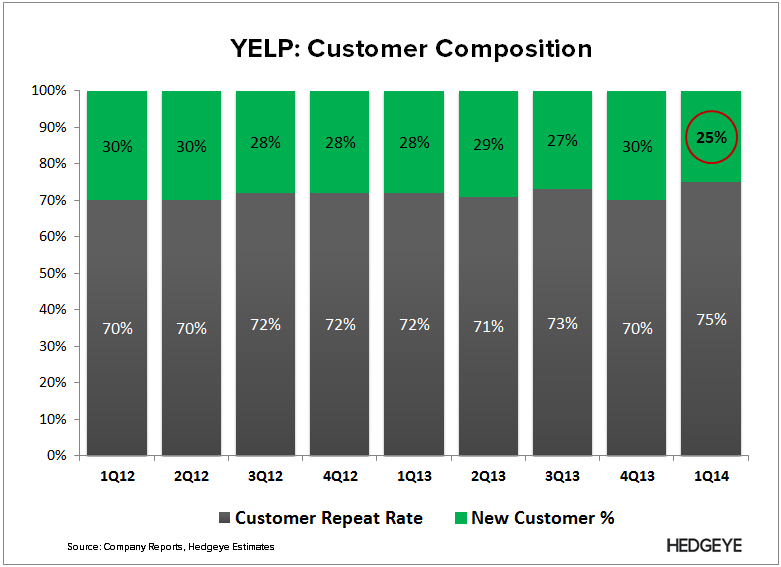

- Active Customers: Ending Customers increased to 74K, up 64% y/y vs. 68% growth in 4Q13. Customer Retention rate accelerated to 75% (from 70% in 4Q13), marking a new high for YELP

- YELP Cohort Growth: YELP's legacy cohorts (2005-2006 & 2007-2008) continued its strong growth trajectory, only showing mild deceleration from 4Q13. The 2009-2010 cohort accelerated, while the later cohorts decelerated

UNDER THE HOOD

YELP's 1Q14 top-line results were not that impressive, beating consensus by 1.8%, its lowest level since 3Q12. It's 2Q guidance calls for a marked slowdown in revenue growth (56% at the high end of guidance vs. 66% in 1Q14). But more importantly, its operating metrics are somewhat misleading.

The customer repeat rate is not its retention rate. It's customer mix. This is how Yelp defines it,

"Our customer repeat rate, defined as the percentage of existing customers from which we recognize revenue in the immediately preceding 12-month period"

YELP hit an all-time high in its customer repeat (75%); that means that the

- Existing customers % of total is at a reported all-time high, and

- New customers % of total is at a reported all-time low.

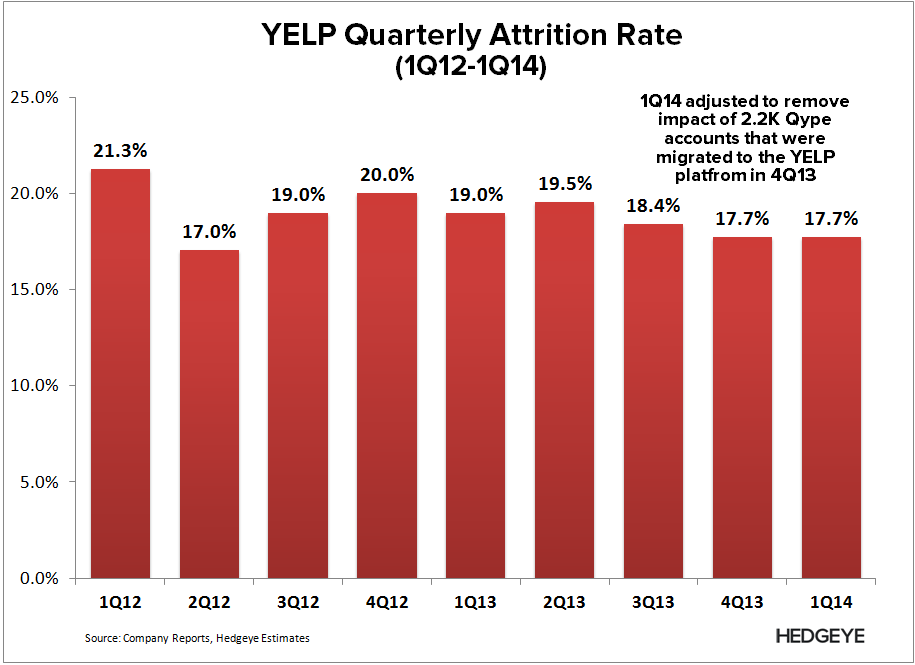

Now, in terms of attrition rate, which we calculate using its stated "customer repeat rate" [customer mix], the rate did improve to 17.2% in 1Q14 vs. 17.7% in 4Q13. However, there is some distortion from the 2.2K Qype accounts that YELP migrated to its platform in 4Q13. In actuality, those are acquired accounts.

If we back those accounts out from both periods, the attrition rate held constant at 17.7%, so net-net, we haven't seen any material improvement in attrition.

In aggregate, when we break this down, 1Q14 results suggest that attrition is accelerating, while new account growth is flattening. We measure this on a per-market basis to net out the impact of geographic expansion, which only has a limited runway.

Each new market that YELP enters will have a lower TAM than than its current footprint, so breaking down these metrics on a per-market basis is a glimpse as to what YELP will be facing as they yield from geographic expansion continues to slow.

New Account growth on a per-market basis will eventually slow then decline. Attrition on a per-market basis will only intensify as its account base grows. It's nasty long-term setup that show no signs of abating.

HEADS THEY LOSE, TAILS THEY LOSE

We expect YELP's attrition rate to accelerate alongside slowing new account growth in 2014. The 1Q14 Release didn't show us anything to suggest otherwise

But what if it doesn't? Let's say that new account growth accelerates, and the attrition rate holds constant. All that does is create a more challenging setup for 2015. It's starting customer base [attrition pool] would be larger, and any strength in 2014 is essentially pulled froward from later periods given its limited TAM.

The stronger 2014 is, the more bearish we become in 2015. You can read more about our Short Thesis in the notes below.

If you have any questions, or would like to discuss further, let us know

Hesham Shaaban, CFA

@HedgeyeInternet

YELP: The Sad Truth

04/28/14 01:49 PM EDT

http://app.hedgeye.com/feed_items/35069

YELP: Death of a Business Model

04/04/14 10:05 AM EDT