Editor's Note: This research note was originally sent to subscribers on April 29, 2014 by Hedgeye Macro analyst Matt Hedrick.

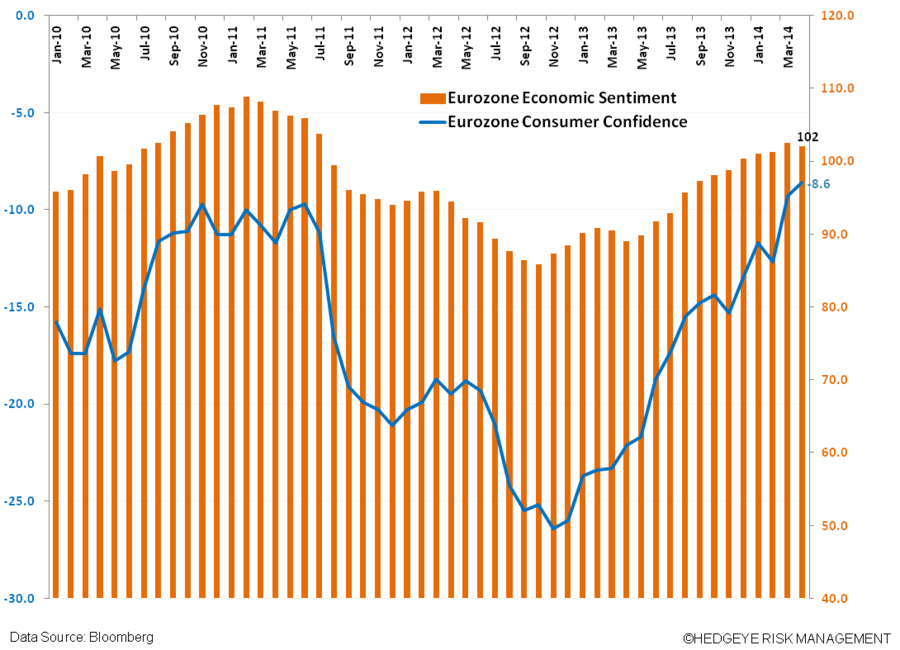

This morning we received Eurozone confidence figures for the month of April. As the charts below show, the data took a step down versus the prior month, and matches confidence figures from the major Eurozone countries that mostly slowed and fell in the April/May period.

We think this inflection lower is but one data point, but indicative of what could play out as a slower growth environment for the remainder of 2014 as the overhangs of high unemployment rates, anti-Euro sentiment, and a sluggish global economy persist. We saw moves higher in confidence figures over the last 12-16 months reflecting improved economic and political outlook, which may now be fully priced in.

- Germany GfK Consumer Confidence 8.5 MAY (8.5 est.) vs. 8.5 prior

- Germany ZEW Economic Expectations 43.2 APR (45 est.) vs. 46.6 prior

- Germany IFO Business Expectations 107.3 APR (105.8 est.) vs. 106.4 prior

- France INSEE Consumer Confidence 85 APR (88 est.) vs. 88 prior

- Italy ISAT Economic Sentiment 88.8 APR vs. 89.5 prior.

- Italy ISAT Business Confidence 99.9 APR (99.5 est.) vs. 99.3 prior

- Italy ISAT Consumer Confidence 105.4 APR (101.2 est.) vs. 101.9 prior

From a quantitative perspective, we maintain our marginally bullish stance on European equities over U.S. equities, and signaled early this week that the German DAX broke its TREND level of support. Below we offer up its new levels (see chart below).

From a policy perspective, we continue to expect ECB President Mario Draghi and the Eurocrats to manage expectations over the medium to long term. On Monday Draghi was reported to have said to a German lawmakers that a QE program is relatively unlikely now. We’ll take the comment at face value and believe that opportunistically Draghi will continue to have QE in his back pocket, which should encourage European equities higher. We also underline that Draghi is managing his inflation target of 2.0% over the longer term, and already there are encouraging signs that inflation is percolating:

- Germany Preliminary CPI rose 1.3% in April Y/Y (1.4% est.) and 1.0% prior

We expect interest rates to remain “accommodative” = at the present rate or lower, as the bank works on schemes to better unlock lending to the real economy (especially SMEs).

On the currency front, the EUR/USD is trading in a bullish formation, above its TRADE, TREND, and TAIL levels of support, as outlined in the chart below. We expect the cross to trade higher as Eurozone QE remains on hold and as Fed Head Janet Yellen continues her dovish policy stance.

UK Bulls

The UK economy is following our playbook: tighter monetary policy = stronger currency = stronger purchasing power, home price appreciation, and confidence. UK GDP ramped to +3.1% Y/Y in Q1 (double what we’ve forecast in the USA).

BOE Governor Mark Carney recently said that he’s optimistic about the economy’s recovery, comfortable with the current level of interest rates, and reiterated that when it does see increases in interest rates they will be gradual and limited. This week Lloyd’s Business Barometer showed a meaningful move higher, to 66 in April vs. 44 in the prior reading.

We remain bullish on the equity market (despite being essential flat YTD) and the GBP/USD.

Our bullish levels on the GBP/USD are outlined below: