PNRA remains on the Hedgeye Best Ideas list as a SHORT.

Panera beat muted 1Q14 estimates, posting top line and bottom line surprises of 147 and 225 bps, respectively. Company same-store sales of +0.1% also bested the consensus estimate of -0.6%, driven by +1.7% price and +1.2% mix.

A quick glance at the headline numbers, however, could be materially misleading as the underlying numbers and trends continue to indicate a much longer turnaround than the street expects. Management guided 2Q EPS to $1.70-1.76, well below the current street estimate for $1.84 and tightened its FY14 same-store sales range to 2.0-3.5%. Despite this, they essentially maintained FY14 EPS guidance, tightening the high end of the range by $0.05 to arrive at a new target of $6.80-$7.00.

The release didn’t surprise us one bit and neither has today’s stock action. This morning’s earnings call was, in our opinion, rather painful to listen to – imagine how the bulls felt! All told, we came away from the call with greater conviction in our short thesis. In our view, management sounded unsure of itself and failed to effectively explain why its full-year guidance is not aggressive considering weak transaction trends, commodity inflation and the significant investment ahead. Notably, several analysts sounded increasingly bearish in the question and answer session which we would attribute to an increasingly cloudy outlook. As a result, we expect FY14 street estimates to be revised down over the current quarter. Until we see a meaningful acceleration in trends or a material boost from key initiatives, we continue to believe FY15 estimates are aggressive as well.

What we liked in the quarter:

- Revenues of $605.34 million beat the consensus estimate by 147 bps

- Adjusted EPS of $1.52 beat the consensus estimate by 225 bps

- Company same-store sales of +0.1% beat the consensus estimate of -0.6%

- Over 80% locked on commodity inputs in FY14

- Have slightly less than $200 million remaining under current repurchase plan

- Rapid Pick-Up will be implemented system-wide by year end

- Sandwich production times have improved materially, down 35 seconds on average

What we didn’t like in the quarter:

- Management lowered 2Q guidance but essentially held FY14 guidance flat

- Narrowed same-store sales guidance to 2.0-3.5% growth

- Transaction growth -2.8% y/y

- Operating margins -250 bps y/y

- Cost of sales +30 bps y/y led by higher paper costs and commodity inflation

- Labor expenses +40 bps y/y led by the addition of 35 hours per week to stores

- G&A and D&A +80 bps and +60 bps y/y and will ramp throughout the year due to planned investment in Panera 2.0

- Limited visibility around impact from materially higher marketing spend as the results vary on market-to-market basis

- Catering hubs will be dilutive to returns for at least the next year

- Management’s inability to clearly explain its full-year assumptions

- Management’s apparent lack of confidence

- Management’s ongoing commitment to new unit growth

- Overall uncertainty and volatility surrounding the Panera 2.0 rollout

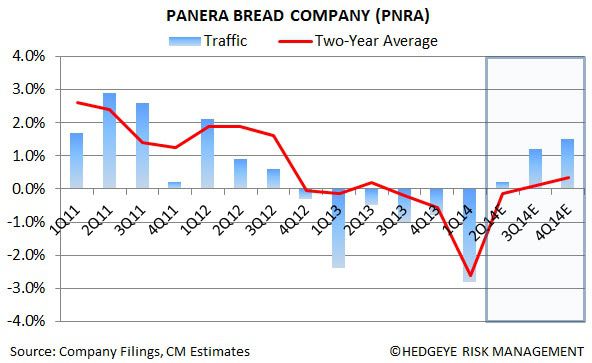

Same-store sales trends are abysmal and we believe the street is taking a leap of faith in its 3Q and 4Q estimates.

Traffic growth will be vital in the coming quarters and we will need to see this downward trend reverse meaningfully before we begin to get less bearish.

The street currently expects operating margins to increase on a year-over-year basis by 4Q. We don’t believe this will happen and, considering the bulk of Panera 2.0 will be rolled out in FY15, think next year’s margin assumptions are aggressive as well.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst