“It's just a job. Grass grows, birds fly, waves pound the sand. I beat people up.”

- Muhammad Ali

As a youngster growing up in southern Alberta, I was an enthusiast of Stampede Wrestling. Back in those days, before World Wrestling Entertainment began to dominate, professional wrestling was split into territories and Calgary-based promoter Stu Hart was recognized as one of the top promoters in the field. He had many colorful wrestlers in his stable, but one of the more interesting was Joe “Tweet Tweet” Tomasso.

Tomasso was a scrappy Italian from Hamilton, Ontario. He earned his nickname “Tweet Tweet” for talking about his imaginary pet bird (incidentally, he also spoke with a pirate’s accent). Tomasso had decent success in the ring and shortly before his retirement, the famed Stu Hart said, “He was an indestructible little bastard.” High compliments from the Canadian godfather of wrestling to a small undercard wrestler like Tomasso.

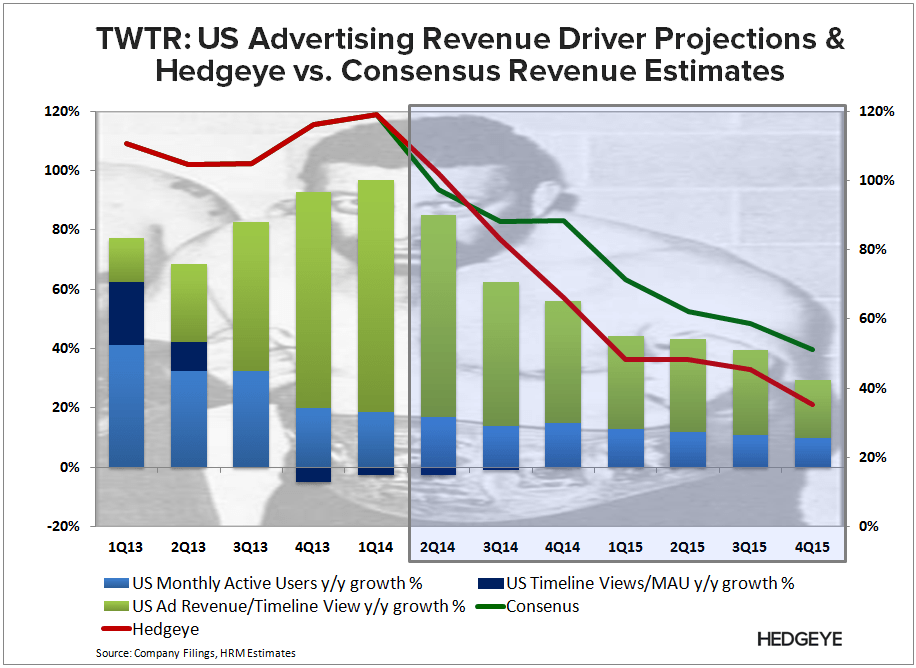

Speaking of imaginary tweets, Twitter (TWTR) reported earnings last night after the close. While the $250 million in quarterly revenue suggests the business model isn’t a total façade, the fundamental sell call we’ve been making on Twitter is playing out in spades with the stock down over -11% this morning to a new 52-week low.

(Our internet analyst Hesham Shabaan reiterated his thesis in this video.)

A few key takeaways from the quarter:

- User Growth: Decelerated sequentially. US was up 19% y/y vs. 20% in 4Q13. Global up 25% vs. 30% in 4Q13. Int’l slowed to 27% vs. 34% last quarter.

- Engagement (timeline views/user): Decelerated globally, decline moderated in the US (-2% vs. -5%), deteriorated in int’l (-10% vs. -2%). Users gravitating toward Tweetdeck will remain a secular headwind.

- Guidance: 2Q14 revenue of $270-$280 vs. consensus of $272. Raised 2014 range by $50M to $1.20B-$1.25B, ahead of the beat on 1Q guidance.

The best way to describe the Twitter quarter is Shakespeare’s oft used expression, “expectation is the root of all heartache.” At more than 20x this year’s market cap to revenue, Twitter’s expectations were high, indeed.

Back to the Global Macro Grind...

Staying on the stock specific side our wily veteran and head of Retail research Brian McGough is adding Target (TGT) to our Best Ideas list as a sell in a conference call today at 11 a.m. EST. According to McGough:

“The crux of our argument? Wall Street's perception of Target's financial trajectory is more upbeat than Main Street. When the stock glossed over the company's weak 4Q earnings report, it was because Steinhafel (CEO) issued guidance that he hoped the company would grow into if the Company repaired its reputation after the data breach - not guidance that he knew TGT could meet or beat. We don't think that the Street is giving TGT credit for a) a miss this year, and b) another one in 2015. The reality is that when a customer has a great experience in retail, they tell a friend. When a customer has a bad experience, they tell 20. Just ask JC Penney or Lululemon. Some of these 'fire your customer' events are worse than others, but there's one commonality - they take a very long time to recover.”

If you don’t currently subscribe to our Retail research and would like details on how to access the call, please email .

Keith was off seeing clients in the Midwest the last couple of days and, despite getting in late last night, hit us and subscribers on the “Direct From KM” list with some key thoughts this morning...

Buy in May, and pray? Not on the US consumer, social bubbles, or housing stuff – no thank you!

- Month End – as the Ides of April come to a close, US Consumer (XLY) and Financials (XLF) lead losers at -1.8% for APR, whereas slow-growth-yield-chasing (Utilities) XLU = +4%; if buying inflation and slow growth ain’t broke, don’t fix i

- #Bubbles – the WSJ is “cautious” on Twitter (TWTR) now – thanks for coming out. TWTR, YELP, and FB remain in Bearish Bubble Formations @Hedgeye!

- US Housing – nasty weekly mortgage demand print this morning out of MBA (total, purchase + refi, index) slammed for another -5.9% loss after last week’s -3.3% drop – Rates Down = Demand Down – Janet? Our Q2 Macro Theme of #HousingSlowdown remains intact

On the last point of housing, D.R. Horton, one of the nation’s largest homebuilders, recently announced they will build homes in the price range of $120,000 to $150,000. This appears to be a reaction to the obvious, which is that housing demand is tepid at best, and more aptly anemic for first time buyers. In fact, in February first time home buyers account for a mere 28% of purchases, which is the lowest level since October 2008 (the veritable apex of the financial crisis).

Not that we need more confirmatory data points, but U.S. MBA mortgage applications index came out this morning and showed applications down -4.4% for the most recent week and the total market index down -5.9%. This compares to -2.6% and -3.3% respectively in the prior week and is obviously a deceleration.

As mortgage applications go so goes housing demand and ultimately home prices. As home prices continue to stagnant or decline, it will be increasingly likely that the almighty Federal Reserve continues to be one of the more globally accommodating central banks, which will be negative for the dollar but continue to drive commodity prices higher. Reflexivity anyone?

Our immediate-term Global Macro Risk Ranges are now as follows:

SPX 1

Russell2000 1101-1155

UST 10yr Yield 2.63-2.73%

VIX 13.03-14.72

EUR/USD 1.37-1.39

Brent 108.02-110.67

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research