WWW blew away the consensus by 27% -- coming in at $0.38 vs. expectations of $0.30 – and right in-line with our model sans a slightly higher tax rate. We’re not making any substantive changes to our model, and maintain our view that WWW will beat the company’s stated long-term plan (and consensus) by over 40%.

WWW is easily the most frustrating Retailer/Wholesaler we follow – but it’s also one that offers perhaps the best opportunity. The reality is that the Street latches on to every little negative data point about a specific market for one of WWW’s 16 brands – even if it ultimately does not negatively impact consolidated financial results. Seriously, 80-90% of the questions we field from the investment community have to do with Sperry, despite the fact that it accounts for less than 20% of WWW’s sales. When Sperry first weakened in January, the stock lost $900mm in value, or about 30% of total market cap, because people were afraid of losing 4% of cash flow. And that ignores the potential to turn Sperry’s $450mm in sales into $1bn.

Unfortunately, this unbalanced and outsized reaction does not reciprocate to the upside – positive datapoints and anecdotes on any of the brands are often discarded. We’re not arguing that people should give the stock credit for individual wins on the part of the brands in certain product lines or markets. That would be irresponsible and unrealistic. But we also can’t justify it on the downside, either.

This tells us that before you touch this stock, you need to ask yourself if you can stomach owning a(nother) portfolio or not. It’s one where you’ll have to deal with a lot of negativity around anecdotes into specific pieces of the portfolio – but you’ll get paid when the company ultimately has to release earnings and show the world that it a) knows how to run a portfolio, b) has far more assets that are winning than assets that are losing. This is all about execution. Pull up a 10-year stock chart. If you want to bet against that, be our guest.

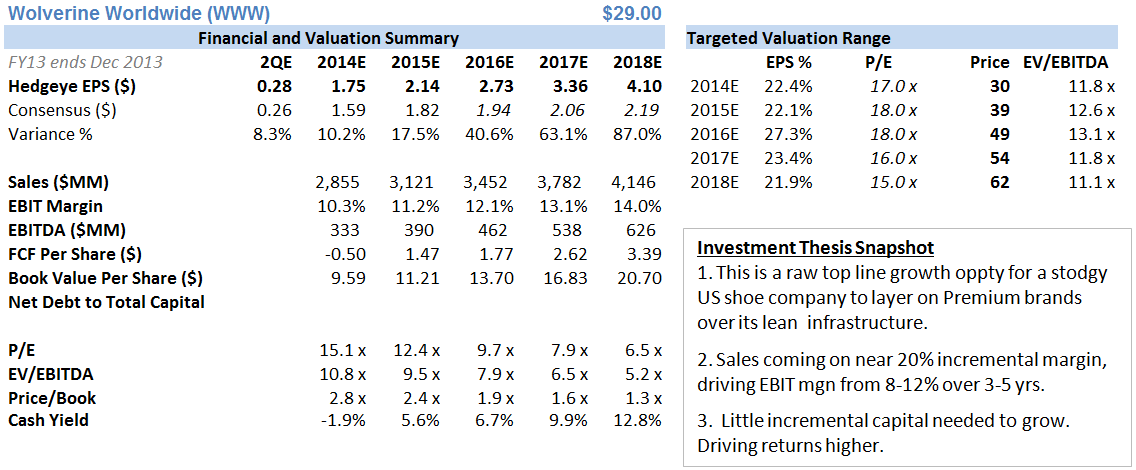

But we need far more than a good track record to want to own a stock like WWW. We need superior earnings power, and a disproportionately low valuation. That’s what we have here. Despite the company’s tepid long-term guidance, we’re coming up with a far superior EPS growth CAGR of 23%. A 17x p/e (14x next year) might seem rich for those who think that WWW is a low-teens grower. It certainly would to us if we had their model. But the problem is that those people have the ‘E’ part of the equation wrong. They were wrong this quarter. And they’re going to be wrong again next quarter. The company might have a heavy hand in setting conservative guidance, but ultimately the truth will come out in the numbers. In addition, with Sperry being down in the upper teens this quarter and the stock reacting instead to the 26% consolidated earnings beat, this gives us a glimmer of hope that maybe the WWW conversation is shifting away from Sperry on the margin.

KEY FINANCIAL MODEL ASSUMPTIONS

HERE'S A NOTE WE PUBLISHED LAST WEEK OUTLINING 3 KEY QUESTIONS FOR MANAGEMENT

04/25/14

WWW – 3 KEY QUESTIONS

As we’ve done with a host of other companies recently, here’s our ‘3 Key Questions’ that we’d ask WWW’s CEO if we had a 5-minute one-on-one. The company is reporting its 1Q14 earnings on Tuesday, April 29th, so timing is key here.

Here goes…

1. Revenue? Please justify your 4-6% top line guidance this year and explain why this is not the ‘year of revenue growth’. If the following narrative is wrong, please tell us why.

- 2012 was the year of the PLG deal. It was big, and painful initially – no EBIT, just interest from $1.2bn in debt.

- 2013 was the year of integration. In 1H people moved around, brands were repositioned, and management realigned. Then in 2H the chessboard was largely set, but they had to seal the deal with an SAP implementation, which went without a hitch.

- Then comes 2014 – which should be all about revenue growth. Your global salesforce, which is the most efficient footwear distribution operation on the planet, has four new major tools (brands) in its toolbox. You’ve been lining up international distribution arrangements over the past 18 months. And while you strike new ones every day (we know it takes time), each of them is cumulative (i.e. signing three per month means that by now there should now be over 40). Aside from each of those arrangements getting more productive, there’s still another 150 that could be added by our estimates.

So, with Merrell reaccelerating under Gene McCarthy’s leadership (the guy is money), Keds on its way to becoming one of the top 5 brands in the portfolio ($110mm today on its way to $400mm), Sperry not pulling a face-plant this Spring like so many seem to be hoping for, and international finally being a driver for the new brands – at a time when Europe is undeniably strengthening for most Consumer companies, how can this year NOT be a year of significant revenue growth? Your guidance of 4-6% revenue growth seems ridiculous (see point below on your inability to give good guidance).

2. Why do you give guidance? You stink at it. Sorry to sound harsh, but the reality is that you guide down nearly every quarter, and then come back 13 weeks later and print earnings above where the consensus was in the first place. In theory, earnings growth will ultimately drive the stock price, but all too often your ‘earnings beat’ is never appreciated by the market because you’re simultaneously trying to set a low hurdle for the next quarterly report. Even your long-term guidance is flawed. You gave 5-year revenue and profit projections that suggest $3.70 in EPS. But your EPS figure is $2.90. And what about that $1bn in free cash flow you should generate over that time period? That alone should pay down nearly all your debt, and save $0.30 per share in interest expense (that’s 21% EPS accretion). Add all that up and we get to EPS that’s 45% above your guidance. So the question is why not either a) give guidance in the ballpark of what you know you can really hit or b) get out of the guidance game – one that you so rarely win.

3. Why do you allow the conversation around the WWW story to revolve around Sperry? You have a $2.7bn revenue base, and less than $500mm of that is Sperry. Yet it is impossible to find a Wall Street research note (except ours) where Sperry is not discussed in the first bullet point. We know Wall Street can be short-sighted and myopic, but seriously, you have to control the conversation. Our math suggests that there’s $80mm at risk if the boat-shoe trend in the US rolls over (which is not happening this Spring as some feared), but another $300mm opportunity outside the US as the brand finally taps markets it’s been absent from pretty much forever. Anything wrong with our logic? If not, please take ownership of this debate, because certain parties on Wall Street that love to hate you are having a field day with it.

OUR LONG TERM THESIS

This is the most global footwear company in the world (legacy WWW). It sells about 65% of its units outside the US, and has seamless and sophisticated systems (SAP) such that all distributors speak the same language. The PLG brands, which we think are better quality overall, sell only 5% overseas, and that's simply because its former owner (Collective Brands) spent capital first on Sperry, then on US Payless stores, and did not have anything left in the kitty for international distribution of PLG brands. So now WWW can scale this superior content over its existing lean/mean infrastructure. We think it will drive an incremental $2bn in revenue over 5-years and an extra 400bp of margin. In the end, we get to earnings power of about $4.20, which is 45% ahead of what management guided at its recent analyst meeting. We're the first to admit that WWW probably won't make you rich here, as it will likely take a good 3-4 years to double. But in the meantime you're paying less than 12x next year’s earnings for a 22% EPS grower -- and this company has one of the best track records of anything in consumer.