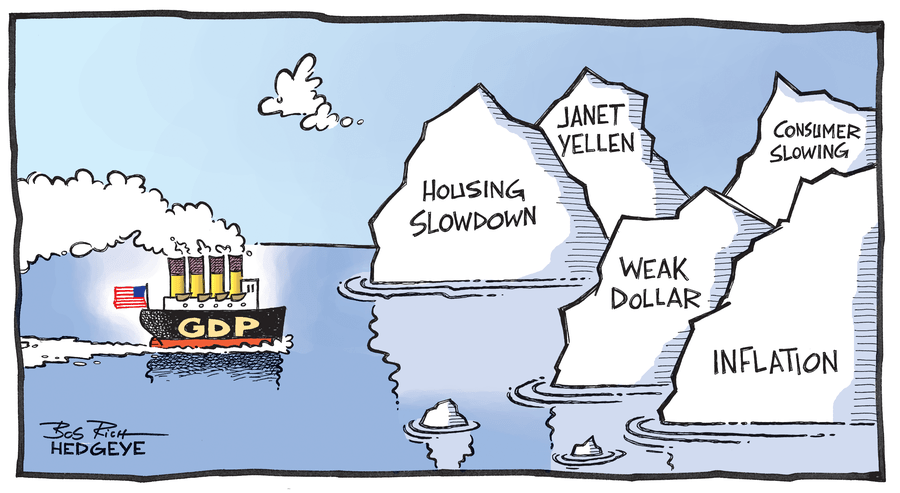

Takeaway: Q1 GDP will likely have a 1% handle on it (down hard from the sequential peak of +4.1% in Q413). No worries, it was just the weather. Right?

Takeaway: Q1 GDP will likely have a 1% handle on it (down hard from the sequential peak of +4.1% in Q413). No worries, it was just the weather. Right?

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.