This note was originally published at 8am on April 14, 2014 for Hedgeye subscribers.

“When you are stuck down a well, someone is bound to throw a rock on your head.”

-Chinese Proverb

So don’t get stuck down a performance well. Rocks to the head hurt. Technically, I’m on vaca with my family this week. But, since I don’t really see what I do (read and write) as a job, I do more of the reading part while I’m watching my kids cannonball one another at the pool.

The aforementioned quote comes from a fantastic Chinese/British economic #history book titled The Opium War. It was describing how English Naval Officer, Charles Elliott, felt after Lin Zexu dumped 20,000 chests of opium into the sea.

This happened in 1839 and became “one of the most celebrated moments in 19th century Chinese history” (pg 69). But it also gave birth to a major economic phase transition. The British found a new island to anchor their opium vessels. It’s called Hong Kong. Changing their position worked.

Back to the Global Macro Grind…

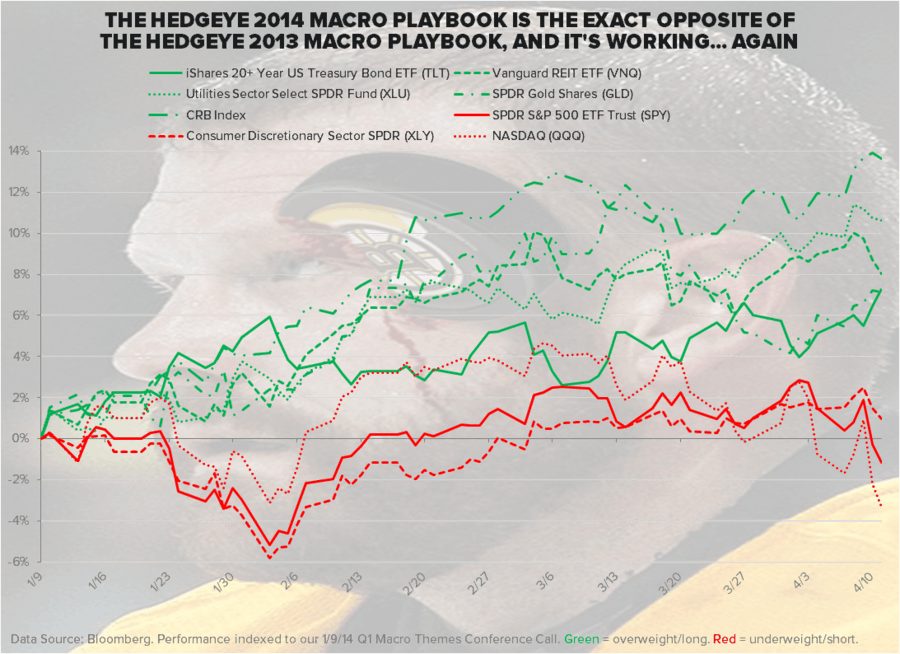

The Russell 2000, Nasdaq, and SP500 were down -3.6%, -3.1%, and -2.6% last week to -4.5%, -4.2%, and -1.8% for 2014 YTD. The current “corrections” for the Russell, Nasdaq, and SP500 are -8.0%, -8.2%, and -4.0%. If you are levered long high-multiple growth, those are rocks to the head.

Thankfully, the feedback from our battle tested long-only customers is that they didn’t do that. Instead, they are long of inflation in inflation terms (Food, TIPs, Gold, etc.) and they are long of US #ConsumerSlowing in slow-growth-yield-chasing terms (Utilities, Bonds, etc.).

Feedback from our most astute macro hedge fund subscribers couldn’t be better. Not only can they be long inflation slowing growth, but they can be short of who is taking the brunt of all this (US consumers) in one of the deepest and most liquid markets in the world (US Equities).

Here’s the US Equity Sector Return Score for the YTD:

- US Consumer Discretionary Stocks (XLY) down another -3.7% last week to -6.9% YTD

- S&P Utilities Sector ETF (XLU) UP another +0.6% in a down tape last week to +9.8% YTD

In other words, as the social media bubbles crash (single stocks down -30-50% from their early March peaks - and we remain The Bears on names like Twitter (TWTR) and YELP), there have been plenty of places to make money, never mind “hide” from US growth beta.

In the face of the US centric bubble popping, check out last week’s top Global Macro performers:

- Gold up another +0.6% to +9.6% YTD

- Emerging Market Equities (MSCI Index) +1.3% to +1.3% YTD

- Emerging Markets LATAM (MSCI) +2.2% to +2.9% YTD

Emerging what?

Yep, lots of our Global Macro value buyers were simply waiting for the rockstar of all Emerging Market Equity catalysts to re-emerge – a Down Dollar. Last week, the US Dollar Index was down another -1.2% to re-test her YTD lows; in kind, Emerging Market Equities hit YTD highs.

I know, so easy a Mucker can do it.

Back to who gets pulverized by an un-elected US Policy To Inflate (courtesy of the Federal Reserve), don’t forget that there are winners who emerge versus US #ConsumerSlowing losers à the countries who get the purchasing power of their people (stronger currencies) back.

To a Keynesian central planner, all of this sounds so 16th century solar system, I am sure. But reality is that reality is priced in local currency terms – and YTD, for the US consumer at least, reality bites.

Here’s how some commodities (priced in Burning Bucks) did last week:

- Coffee up another +8.8% to +76.8% YTD

- Natural Gas up another +4.1% to +12.8% YTD

- Oil (WTIC) up +2.6% last week to +5.9 YTD

Sure, if you back all that out – and blame the weather (which last I checked is fantabulous)… there is no inflation.

But there is some serious YTD absolute and relative return performance!

Which, at the end of the day is what we are all after, is it not? Why would you pay 20x revenues for anything when 2 of the biggest Macro Risk Factors that matter to any economy (GROWTH and INFLATION) are going the wrong way?

Remember, it’s not about absolutes. It’s about rate of change, and:

- US inflation is accelerating

- US growth is slowing

Our competition can blame YTD lows in the 10yr bond yield (2.63% = down -39bps YTD) on anything but the most obvious. They can blame me, the weather – or whatever… but they’re stuck in a proverbial well of YTD macro market scores that disagree.

And unless they want to keep taking pucks to the head from a bunch of hockey players, they better find a new narrative come summer time…

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.60-2.72%

SPX 1786-1832

Nasdaq 3953-4158

VIX 14.52-17.99

USD 79.11-80.01

WTIC Oil 101.73-104.99

Gold 1300-1329

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer