Key Callouts:

The main risk callout this morning is the ongoing compression in the yield spread. The 2-10 yield spread ended 2013 at 265 bps. As of Friday's close it stood at 223 bps, a decline of 42 bps. In the latest week, we saw a further 9 bps of decline. The compression of the yield curve is seemingly at odds with the generally strong labor market data we've seen recently. So, what's causing this? There are two possible explanations.

- First, investors should look back historically at the correlation between the Fed's holdings of treasury and mortgage securities and the level of the 10-year treasury yield. What they will find is that QE1 and QE2 did effectively reduce long-term yields. However, interestingly, rates dropped MORE at the end of QE1 and QE2. Why would yields drop when Fed purchasing ends? The simple answer is concerns around growth slowing. It's possible that the market is following the same playbook, although in slow motion.

- Second, banks have stepped up their purchases of treasury securities since the start of this year. This is partly a natural response to decelerating loan growth, but also partly driven by liquidity requirements. Interestingly, as per a Bloomberg article out this morning, bank holdings of treasury securities are near their late-2012 highs. In late 2012 the 10-year was at or near its all time low of 150 - 170 bps.

Aside from what's happening in rates, it's generally quiet across the Financials landscape. The following are a few of the key callouts from this week's RM.

*2-10 Spread – Last week the 2-10 spread tightened to 223 bps, -9 bps tighter than a week ago.

*U.S. Financial CDS - Swaps tightened for 25 out of 27 domestic financial institutions. The Global US banks (with the exception of BAC, which saw no change) were tighter, by an average of 2 bps w/w, and 6 bps on a m/m basis. The specialty finance companies we track were tighter on the week and on the month with the biggest moves coming from the mortgage insurers, MTG & RDN and Sallie Mae.

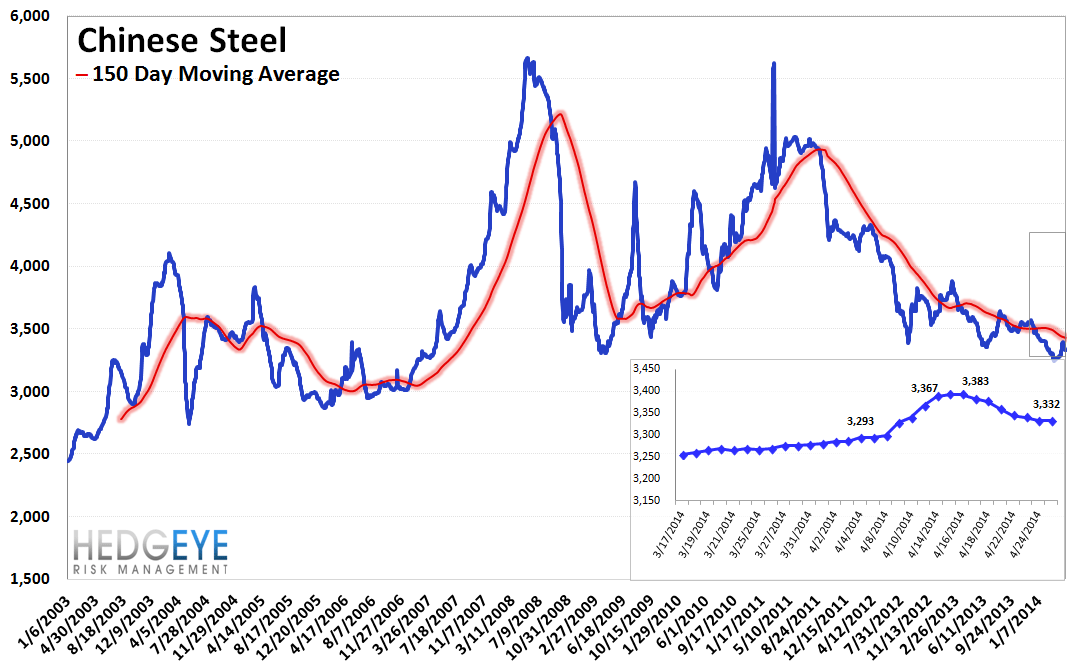

*Chinese Steel – Steel prices in China fell 1.3% last week, or 45 yuan/ton, to 3,332 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 4 out of 12 worsened / 7 of 12 unchanged

• Intermediate-term(WoW): Positive / 7 of 12 improved / 1 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Positive / 4 of 12 improved / 2 out of 12 worsened / 6 of 12 unchanged

1. U.S. Financial CDS - Swaps tightened for 25 out of 27 domestic financial institutions. The Global US banks (with the exception of BAC, which saw no change) were tighter, by an average of 2 bps w/w, and 6 bps on a m/m basis. The specialty finance companies we track were tighter on the week and on the month with the biggest moves coming from the mortgage insurers, MTG & RDN and Sallie Mae. The bond guarantors saw large w/w improvements. Notably improved were AGO, whose swaps tightened by 44 bps w/w, and MBI, whose swaps tightened by 31 bps w/w.

Tightened the most WoW: AGO, MTG, PRU

Tightened the least WoW: HIG, BAC, C

Tightened the most WoW: AIG, GNW, MS

Widened the most MoM: MBI, AGO, JPM

2. European Financial CDS - It was a mixed bag for European swaps this past week. 25 swaps widened and 13 swaps tightened. The Greek banks continue to tighten notably, dropping an average of 33 bps in the past week and 185 bps in the past month. Belgian banks also tightened considerably, dropping an average of 9 bps w/w. Russia’s Sberbank, Germany's IKB, and France's Societe Generale all widened w/w, by 25, 15, and 11 bps, respectively.

3. Asian Financial CDS – Last week Chinese and Indian banks widened nominally, while Japanese financials tightened by an average of 1.3 bps w/w.

4. Sovereign CDS – European Sovereign Swaps mostly tightened over last week. French sovereign swaps tightened by -3.9% (-2 bps to 46 ) and Portuguese sovereign swaps widened by 1.8% (3 bps to 173).

5. High Yield (YTM) Monitor – High Yield rates fell 0.8 bps last week, ending the week at 5.62% versus 5.63% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 1.0 points last week, ending at 1854.

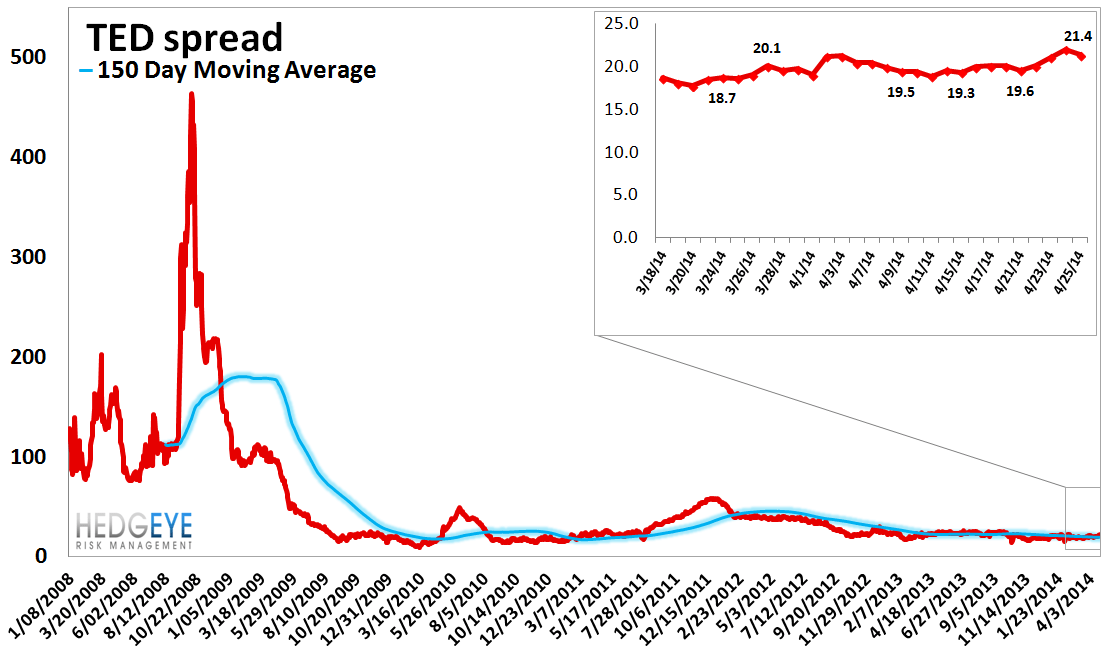

7. TED Spread Monitor – The TED spread rose 1.3 basis points last week, ending the week at 21.4 bps this week versus last week’s print of 20.09 bps.

8. CRB Commodity Price Index – The CRB index rose 0.3%, ending the week at 311 versus 310 the prior week. As compared with the prior month, commodity prices have increased 2.2% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

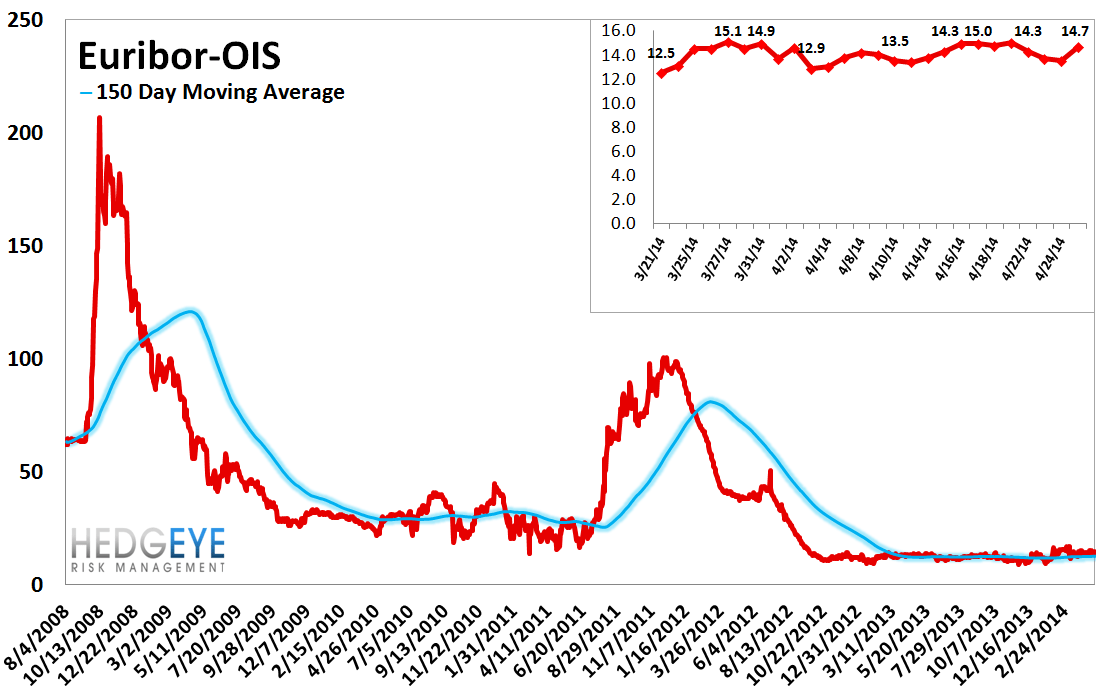

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread did not change from the previous week, remaining at 15 bps.

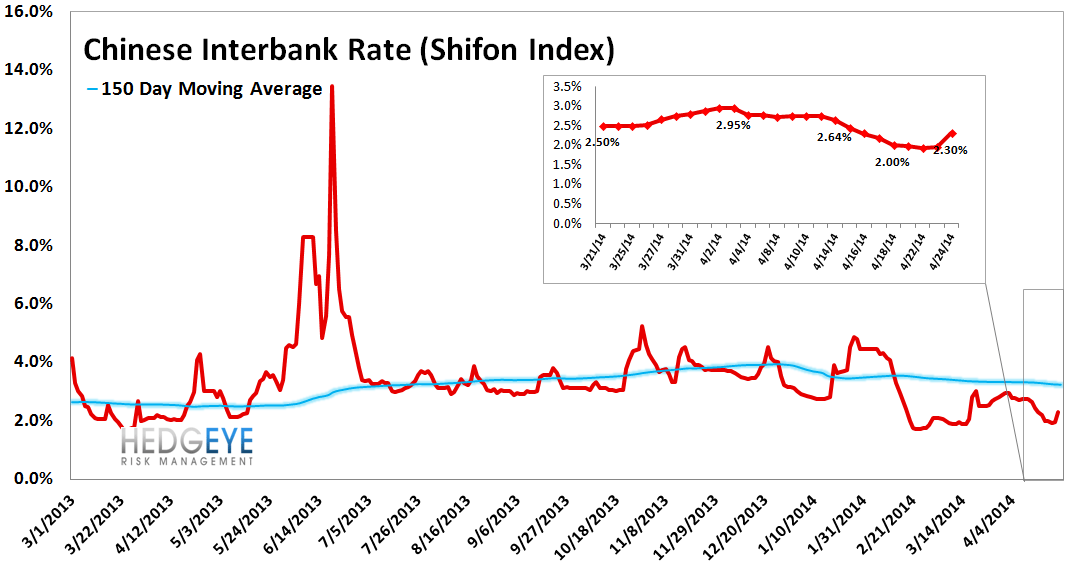

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 30 basis points last week, ending the week at 2.3% versus last week’s print of 2.0%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 1.3% last week, or 45 yuan/ton, to 3332 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

12. 2-10 Spread – Last week the 2-10 spread tightened to 223 bps, -9 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.6% upside to TRADE resistance.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT