#HousingSlowdown

We recently detailed our expectation for a #HousingSlowdown in our Q2 2014 Macro themes call. Incidentally, we’ll be launching comprehensive coverage of housing in the next few weeks.

The housing data of the last few days continues to offer further, positive confirmation of the marked, and geographically pervasive, slowdown in housing demand.

Home price growth follows the slope of demand and current demand measures (Existing/Pending/New Home Sales) continue to flag while mortgage application data through mid-April is signaling a further deceleration in forward transaction activity.

That the deceleration in activity is occurring in the face of both the positive shift in weather and declining interest rates makes it that much more notable.

While weather probably exaggerated some of the underlying weakness to start the year, we continue to think that the collective impact of stagnant income growth, declining affordability, a reversal in institutional interest, and the implementation of QM regulations will serve to pressure housing demand over the intermediate term.

Summary highlight of recent data

APRIL DATA: The NAHB HMI and weekly MBA mortgage data represent a couple of the most real-time measures of existent demand/sentiment trends and both continue to signal weakness.

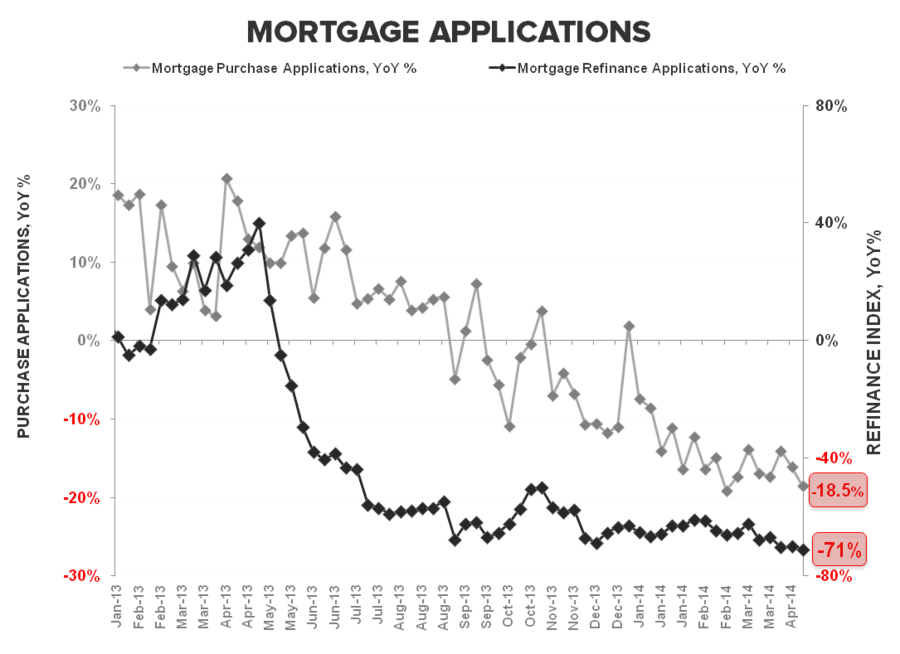

- Mortgage Applications: The composite mortgage application index declined 3.3% week-over-week as the Purchase Applications and Refinance sub-indices hit new lows in year-over-year growth. As it stands, Purchase Applications are down -19.3% off peak and -18.5% YoY while refinance activity is down -71% YoY!

- NAHB HMI: Headline NAHB confidence increased 1 point month-over-month in April versus the downwardly revised March print with builder confidence flat or down across geographies with the exception of the Northeast. Confidence in the West region slid for a third consecutive month, continuing its expedited 26 point drawdown from a peak reading of 71 just three months ago. The composite index is now down 10 points off its December peak of 57.

MARCH DATA: Home price growth decelerated and both Existing and New Home Sales slowed sequentially in March. The slowdown, coming post the weather inflection, was again pervasive across geographies, further confuting the "its the weather" in isolation thesis.

- Existing Home Sales: Existing Home Sales declined -0.2% MoM and -8% YoY – accelerating 70 bps versus the -7.3% decline in February. Sales were down across geographies with the West region again leading the declines.

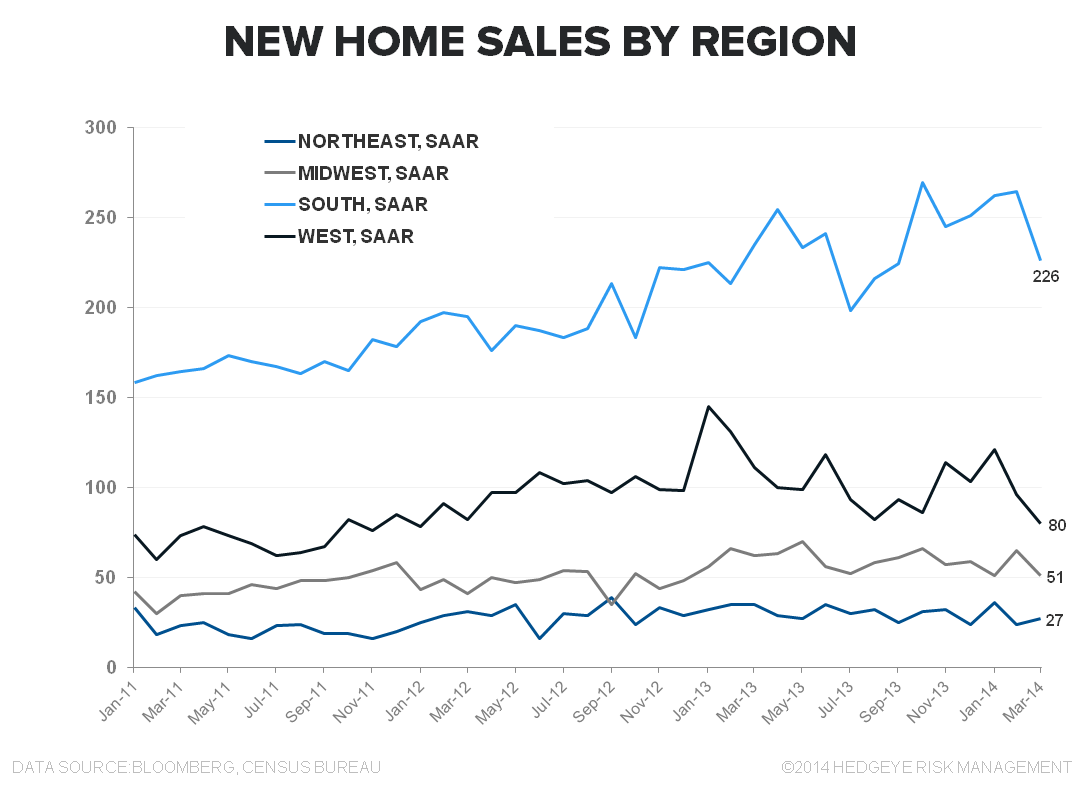

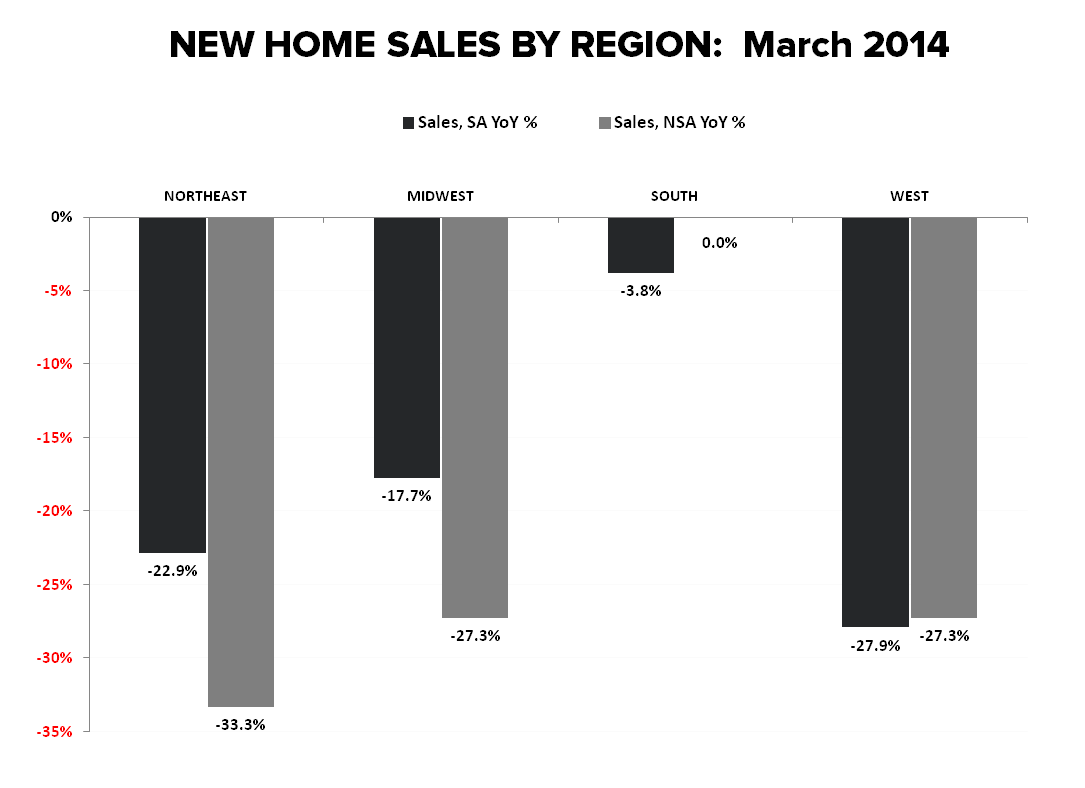

- New Home Sales: New Home sales declined -13% YoY, marking the 1st month of negative year-over-year growth since September of 2011. The Northeast was the lone region recording a MoM increase in sales while year-over-year sales growth declined across all geographies.

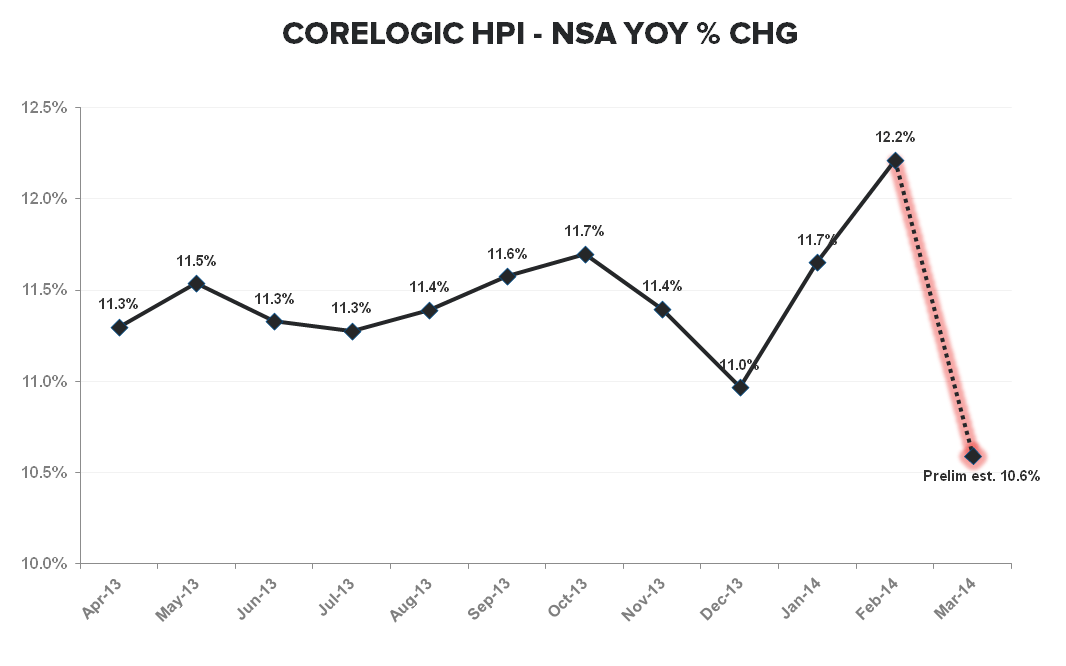

- Corelogic HPI: The preliminary estimate is for a sequential deceleration of 160bps in home price growth in March – the slowest pace of growth in 13 months and the largest sequential deceleration since June of 2006. As a reminder, the March/April data will be the first to reflect any early impacts of QM implementation, which went into effect on January 10.

* * * * * * *

Editor's Note: This note was originally sent to subscribers on April 23, 2014 by Hedgeye Macro Analyst Christian Drake. Follow Christian on Twitter @HedgeyeUSA.