TODAY’S S&P 500 SET-UP – April 24, 2014

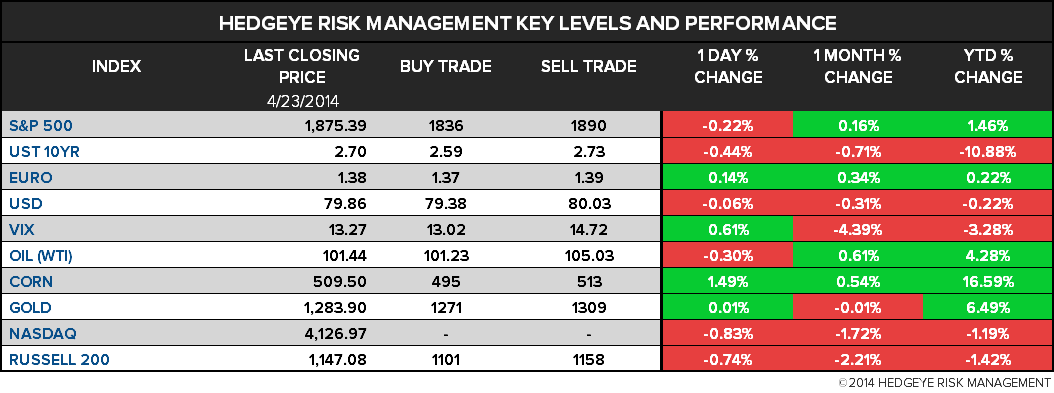

As we look at today's setup for the S&P 500, the range is 54 points or 2.10% downside to 1836 and 0.78% upside to 1890.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.26 from 2.26

- VIX closed at 13.27 1 day percent change of 0.61%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Durable Goods Orders, March, est. 2% (prior 2.2%)

- Durables Ex Transportation, March, est. 0.6% (prior 0.2%, revised 0.1%)

- Capital Goods Orders Non-def Ex-Aircraft, March, est. 1.5% (prior -1.3%, revised -1.4%)

- Capital Goods Shipments Non-def Ex-Aircraft, March, est. 1% (prior 0.5%, revised 0.6%)

- 8:30am: Initial Jobless Claims, April 19, est. 315k (prior 304k)

- Continuing Claims, April 12, est. 2.745m (prior 2.739m)

- 9:45am: Bloomberg Consumer Comfort, April 20 (prior -29.1)

- 10am: Kansas City Fed Manufacturing Activity, April, est. 8 (prior 10)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- House, Senate out of session on recess

- Obama in Japan, meets with Japanese PM Shinzo Abe, holds press conf., attends state dinner, speaks at youth event

- 8:45am: Export-Import Bank holds annual conf., President Fred Hochberg delivers opening remarks

- 12pm: Justice Samuel Alito speaks at Food and Drug Law Institute conference

- U.S. ELECTION WRAP: NYT Senate Poll; Tea Party Endorsements

WHAT TO WATCH:

- GE said to be in talks to buy Alstom for $13b

- Google to Netflix pay-for-access deals said to get FCC review

- Apple stock split removes obstacle to inclusion in Dow avg

- German business confidence unexpectedly rises in growth sign

- Obama says U.S. ready to move on additional Russia sanctions

- Nokia to exclude India plant from Microsoft deal on tax issues

- E-cigarettes to fall under FDA as U.S. seeks to tame trend

- Forbes sale said to founder with Axel Springer not bidding

- Gartner sees 12% rise in semiconductor cap equipment spending

- Spain auctions 10-yr bonds at 3.059%, lowest yield on record

- Williams Opal gas explosion cuts pipe flows as town evacuated

AM EARNS:

- 3M (MMM) 7:30am, $1.80

- Aetna (AET) 6am, $1.55 - Preview

- Alexion Pharmaceuticals (ALXN) 6:30am, $1.26

- Altria Group (MO) 6:58am, $0.57 - Preview

- AmerisourceBergen (ABC) 6:15am, $1.00 - Preview

- Avnet (AVT) 8am, $1.08

- BankUnited (BKU) 7:30am, $0.45

- Bemis (BMS) 7am, $0.57

- Brunswick (BC) 7:39am, $0.60

- Cameron International (CAM) 7:30am, $0.72 - Preview

- Caterpillar (CAT) 7:30am, $1.23 - Preview

- Celgene (CELG) 7:30am, $1.65 - Preview

- CMS Energy (CMS) 7:30am, $0.72

- Coca-Cola Enterprises (CCE) 7:30am, $0.44

- Colfax (CFX) 6:01am, $0.45

- Delphi Automotive (DLPH) 7am, $1.09

- Diamond Offshore Drilling (DO) 6am, $0.65 - Preview

- Domtar (UFS) 7:30am, $1.67

- DR Horton (DHI) 6am, $0.34 - Preview

- Dunkin’ Brands Group (DNKN) 6am, $0.36

- Eli Lilly & Co (LLY) 6:30am, $0.71 - Preview

- Entergy (ETR) 7am, $2.29

- EQT (EQT) 7am, $0.89

- First Niagara Financial Group (FNFG) 7:15am, $0.17

- Freeport-McMoRan Copper & Gold (FCX) 8am, $0.42 - Preview

- General Motors Co (GM) 7:30am, $0.04 - Preview

- GrafTech International (GTI) 7:01am, ($0.02)

- Graphic Packaging Holding (GPK) 7:30am, $0.13

- Helmerich & Payne (HP) 6am, $1.48

- Hershey (HSY) 6:58am, $1.14

- JetBlue Airways (JBLU) 7:30am, $0.07 - Preview

- KKR & Co LP (KKR) 8am, $0.51

- Lorillard (LO) 7am, $0.72

- Mead Johnson Nutrition (MJN) 7:30am, $0.91

- NASDAQ OMX Group (NDAQ) 7am, $0.71

- New York Times (NYT) 8:30am, $0.03

- Nielsen Holdings NV (NLSN) 7am , $0.41

- Nucor (NUE) 9am, $0.38

- Patterson-UTI Energy (PTEN) 6am, $0.24

- Peabody Energy (BTU) 8am, $0.01 - Preview

- Potash (POT CN) 6am, $0.35 - Preview

- PulteGroup (PHM) 6:30am, $0.20 - Preview

- Quest Diagnostics (DGX) 7am, $0.88 - Preview

- Raytheon (RTN) 7am, $1.77

- Reliance Steel & Aluminum (RS) 8:50am, $1.23

- Royal Caribbean Cruises (RCL) 8:31am, $0.27

- SCANA (SCG) 7:30am, $1.15

- Sigma-Aldrich (SIAL) 7am, $1.03

- Sirius XM Holdings (SIRI) 7am, $0.02

- Sonus Networks (SONS) 7am, ($0.01)

- Southwest Airlines (LUV) 6:35am, $0.17 - Preview

- Stanley Black & Decker (SWK) 6am, $0.96

- Starwood Hotels (HOT) 6am, $0.56

- T. Rowe Price (TROW) 7:29am, $1.04

- Time Warner Cable (TWC) 6am, $1.67 - Preview

- Timken (TKR) 7:30am, $0.81

- Under Armour (UA) 7am, $0.05 - Preview

- United Continental (UAL) 7:30am, ($1.36)

- United Parcel Service (UPS) 7:45am, $1.08 - Preview

- USG (USG) 8:30am, $0.19

- Valley National Bancorp (VLY) 7am, $0.14

- Verizon Communications (VZ) 7:30am, $0.87 - Preview

- Waste Management (WM) 7:30am, $0.45

- Wyndham Worldwide (WYN) 6:29am, $0.75

- Yandex NV (YNDX) 6am, $8.77

- Zimmer Holdings (ZMH) 7am, $1.47

PM EARNS:

- Altera (ALTR) 4:15pm, $0.32

- Amazon.com (AMZN) 4pm, $0.23

- Baidu (BIDU) 4:30pm, $6.24

- Barracuda Networks (CUDA) post-mkt , $0.01

- Broadcom (BRCM) 4:05pm, $0.46

- Cerner (CERN) 4:01pm, $0.37 - Preview

- Chubb (CB) 4:03pm, $1.56

- Cincinnati Financial (CINF) 4:05pm, $0.54

- Cirrus Logic (CRUS) 4pm, $0.32

- Cliffs Natural Resources (CLF) 4:22pm, ($0.23)

- Deckers Outdoor (DECK) 4pm, ($0.14)

- Eastman Chemical Co (EMN) 4:36pm, $1.59

- Edwards Lifesciences (EW) 4:01pm, $0.69 - Preview

- Freescale Semiconductor (FSL) 4:05pm, $0.25

- KLA-Tencor (KLAC) 4:15pm, $1.11

- Las Vegas Sands (LVS) 4:22pm, $0.94

- Leggett & Platt (LEG) 4:05pm, $0.38

- Maxim Integrated Products (MXIM) 4pm, $0.39

- Microsoft (MSFT) 4:01pm, $0.63 - Preview

- Newmont Mining (NEM) post-mkt , $0.19 - Preview

- Noble Energy (NBL) 5pm, $0.75

- Olin (OLN) 5pm, $0.34

- Pandora Media (P) 4:01pm, ($0.14)

- PerkinElmer (PKI) 4:05pm, $0.44

- Principal Financial Group (PFG) 4pm, $0.92

- Regal Entertainment Group (RGC) 4pm, $0.19

- Republic Services (RSG) 4:05pm, $0.44

- Starbucks (SBUX) 4:03pm, $0.56 - Preview

- Stericycle (SRCL) 4:01pm, $0.99

- SunPower (SPWR) 4:05pm, $0.32

- Superior Energy Services (SPN) 4:05pm, $0.21

- Swift Transportation Co (SWFT) 4:01pm, $0.12

- Synaptics (SYNA) 4:05pm, $0.57

- Universal Health Services (UHS) 5pm, $1.22

- Validus Holdings (VR) 4:15pm, $1.56

- VeriSign (VRSN) 4:05pm, $0.63

- Visa (V) 4:05pm, $2.18

- Weatherford International (WFT) 4:40pm, $0.11

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Goldman Sets Out Case for Commodity Holdings as Rivals Cut Back

- WTI Trades Near Two-Week Low as Stockpiles Climb; Brent Steady

- Coffee’s Prayers for Rain Met With Threat of Deluge: Commodities

- Banks Reducing Commodity Trading Seen Ending Link to Equities

- LME to Start Clearing Collateral in Yuan as Asia’s Power Rises

- Copper Touches Three-Week High as Growth Rebound May Spur Demand

- Gold Trades Near 10-Week Low as U.S. Data Weighed With Ukraine

- Arabica Coffee Drops as Rain Heads for Brazil; Sugar Also Falls

- Rebar in Shanghai Rises to 1-Wk High on Demand Pickup, Inventory

- U.K. Shale Could Spark $55 Billion in Investment, E&Y Says

- Marubeni Says China May Have Detained Three Grains Unit Staff

- Deadly Illegal Mining Booms Below South Africa’s City of Gold

- Asia Energy Bull & Bear Pit China Reforms vs. OPEC: BI Outlook

- Castoffs in Barrick Newmont Merger May Become $4 Billion Rival

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team