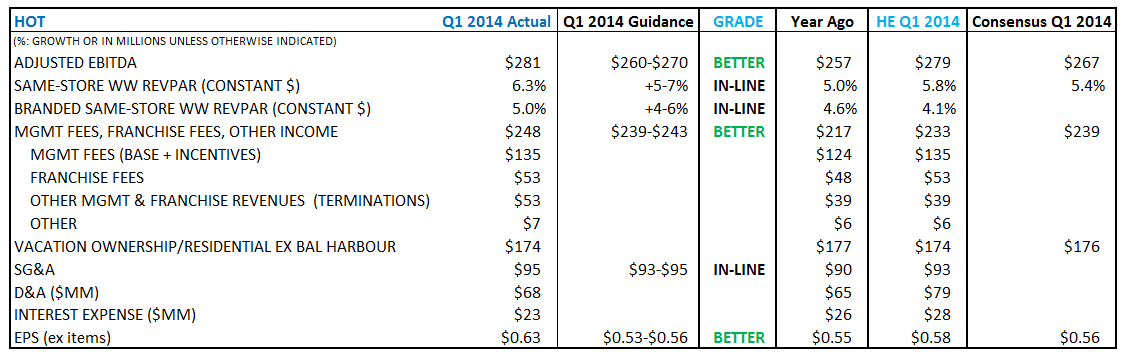

In an effort to evaluate performance, we compare how Q1 2104 measured up to previous management commentary and guidance

OVERALL:

BETTER - The fears surrounding an emerging markets slowdown didn't show this quarter and as a result adjusted EBITDA exceeded our our higher than consensus forecast. Management, Franchise and Other Fees were higher than forecast as well. No problems with management's operating ability but the company's financial policy continues to hold the stock back.

North America:

- BETTER:

- Occupancy at record highs

- Late cycle: RevPAR should be rate driven, but several years away from new supply in most markets - especially at the high end

- Momentum continuing into Q2, we expect North American REVPAR growth to continue to pace in the upper half of the range of 5 to 7%.

- Adjusting for the Easter shift, into April, this momentum has continued into Q2.

- PREVIOUSLY:

- North America picking up steam

- We’ve seen three quarters in a row of record occupancy

- The lodging recovery in North America continued unabated

- Owned hotels saw REVPAR up nearly 10% and margins up 350 bps

- We expect North American REVPAR growth at the upper end of our 5% to 7% outlook range, with rate accounting for 75% to 80% of the increase

Europe:

- SAME:

- RevPAR 2.5% but Q1 is slow season

- We need to see better rate gains in Europe and we need more robust demand. Until that happens Europe growth will stay in the 2% to 4% range like we experienced for the past two years

- PREVIOUSLY:

- Ended the year well, with REVPAR up over 4% in local currencies in Q4

- Occupancy remained high, nearly 68% for the full year 2013

- European economies remain fragile and the euro could still be an issue, we’re hopeful that the improving trend will continue

- In Q4, we saw mid-single digit REVPAR growth in: Spain, Italy, and the U.K - only Germany was a little soft

- We assume Europe REVPAR growth in 2014 will be at the low end of our worldwide outlook range

- Europe also had a good January, but it’s the low season

- We’ll have to wait until March and April to get a better sense of the European trend in 2014

China:

- BETTER:

- performance stronger than expected

- Expect Q2 slightly slower following strong Q1 results

- RevPAR +12% driven by Sheraton Macau with 90% occupancy

- ex Sheraton Macau (Mainland China) 6% RevPAR growth

- promoting the company across all segments, markets, and channels

- >70% occupancy PRC nationals

- Results driven by increasing occupancy and not rates

- PREVIOUSLY:

- China now represents a meaningful piece of our global business, accounting for 13% of our fee revenues

- China is rebounding

- Expect Asia REVPAR to continue to grow at the high end of our global REVPAR outlook range of 5% to 7%

Latin America:

- SAME:

- Mixed, emerging two-tier region

- Mexico & central: combined revpar +14%

- 2nd Tier: Venezuela, Brazil, Argentia - struggling, f(x) issues

- PREVIOUSLY:

- REVPAR is forecasted to grow in the lower half of our 5% to 7% outlook range

- Same-store owned REVPAR to grow 4% to 6% in local currencies globally, with margin gains of 75 to 125bps

- Disparate results across the region

- Mexico continued to rebound, starting with resorts and followed by urban locations

- Brazil’s the outlook remains unclear but The World Cup should help Brazil and the Sheraton Rio is coming out of renovation

- Argentina was still a mess and reaching the acute stag

- Even with the most recent peso devaluation, the gap between the official and unofficial exchange rate remains large

Group:

- SAME: Group business continues to pace in the mid-single digits with smaller group corporate business especially strong while larger group Association business remains weak. All in all rates are in the mid-single digits in some of these corporate negotiated rates certainly corporate groups are the healthiest of all the group business. Corporate group business does tend to be booked were shorter lead times

- PREVIOUSLY:

- Negotiated corporate rates are up in the mid-single digits for 2014

- Group pace for 2014 is pacing in the mid-single digits

- We are starting to see the return of incentive travel

Costs:

- SAME: SG&A are expected to increase by approximately 3% to 5%.

- PREVIOUSLY:

- SG&A growth is expected to stay in the 3% to 5% range, even as we make infrastructure investments in growth markets and in new capabilities

Share buyback/dividends:

- WORSE:

- no share repurchase activity during Q1 nor QTD in Q2 - investors disappointed, as they should be - ridiculously low leverage

- constantly recalibrating how to return to shareholders will use dividend, special dividend and share repurchase avenues

- special dividends: not adverse to one-time, like flexibility of quarterly

- PREVIOUSLY:

- For 2014, we’ll work hard to continue returning cash to shareholders via - Ordinary dividends, Special dividends, and share repurchases

- Four planned special dividends associated with the $500 million in cash from the completion of the Bal Harbour project.

- We have a healthy dividend with an almost 50% payout ratio and a 1.8% yield

- The Company’s share repurchase authorization has increased by an additional $250 million. As of October 30, 2013, the total amount available under the authorization is approximately $614 million.

Asset sales:

- SAME:

- Asset sales

- now have more asset for sale since the global financial crisis

- North American portfolio, as well as assets in Europe and Asia

- Asset buyer profile

- Europe/Large one-offs: UHNW family or person, sovereign wealth

- US: portfolio sales to PE, funds, or private buyer

- Geographic: Middle East and ethic Chinese around the world

- PREVIOUSLY:

- The (buyers) markets are becoming deeper, and there are more buyers now seeking to deploy larger amounts of money.

- Used to be the public REITs buying single assets, we now see portfolio buyers, and we believe private equity buyers have returned and soveigns are definitely back.

- This is prime time for asset sales and we intend to fully take advantage of it.

- Cap rates: we’ve seen sub-5% cap rates on some of our better hotels and 6% to 7% on some of the more suburban and airport hotels.

- We certainly don’t want to wait until the 11th hour. On the other hand, being patient in selling assets up until now, I think, has worked in the interest of shareholders, not the other way around