TODAY’S S&P 500 SET-UP – April 23, 2014

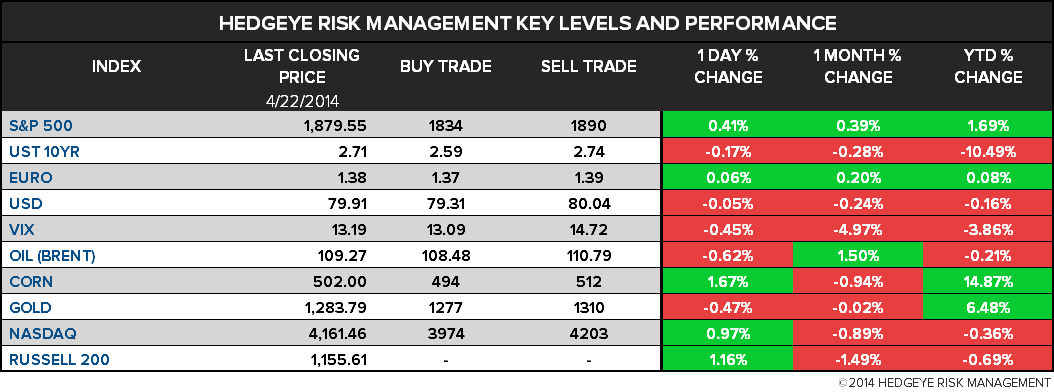

As we look at today's setup for the S&P 500, the range is 56 points or 2.42% downside to 1834 and 0.56% upside to 1890.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.27 from 2.31

- VIX closed at 13.19 1 day percent change of -0.45%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, April 18 (prior 4.3%)

- 9:45am: Markit US Manufacturing PMI, April, est. 56.0 (pr 55.5)

- 10am: New Home Sales, March, est. 450k (prior 440k)

- 10:30am: DOE Energy Inventories

- 11am: Fed to purchase $2b-$2.5b in 2021-2024 sector

GOVERNMENT:

- President Obama in Japan at start of 4-nation trip to Asia

- Congressional Delegation led by House Foreign Affairs Cmte Chairman Ed Royce in Ukraine for meetings with major presidential candidates, NGOs, members of minority groups

- House, Senate not in session

- 10:30am: FCC meets on proposed rule that would make up to 150 MHz of spectrum available for wireless broadband use in 3 MHz band

- 2:30pm: Consumer Financial Protection Bureau, other regulators at public forum on mortgage closing process

WHAT TO WATCH:

- Ukraine weighs move on militants in east amid Russia warnings

- Starboard asks Darden for investor say in Red Lobster spinoff

- Dish said to target summer release for U.S. Internet-TV

- Toyota outsells GM, Volkswagen in Jan.-March quarter

- Buffett’s pay principles put to test on Coke vote: Winters

- Apple’s slowing iPhone sales threaten stock after 5% slump

- PTTEP agrees to pay Hess $1b cash for Thai assets

- Australia to buy 58 more F-35 jets, scaling back initial plan

- Charter said to be near deal for divested Comcast subscribers

- Goldman unbowed as Barclays joins bank commodities exodus

- Citigroup says has no plans to exit core businesses in Korea

- Netflix said to expand into France by yr-end amid global push

- Genworth to raise as much as $700m in Australia offer

- LG Household considering making offer to buy Elizabeth Arden

- Caesars Entertainment bids to build $750m New York casino

- China manufacturing gauge signals economic weakness persists

- Euro-area industry surveys increase as price weakness persists

- Osborne hits U.K. deficit-reduction target; economy struggles

AM EARNS:

- Air Products & Chemicals (APD) 6am, $1.35

- Amphenol (APH) 8am, $0.96

- Avery Dennison (AVY) 8:30am, $0.66

- Biogen Idec (BIIB) 6:30am, $2.56 - Preview

- Boeing (BA) 7:30am, $1.54 - Preview

- Brinker Intl (EAT) 7:45am, $0.83

- Celestica (CLS CN) 7am, $0.20

- Delta Air Lines (DAL) 7:30am, $0.29 - Preview

- Dow Chemical (DOW) 7am, $0.71

- Dr Pepper Snapple (DPS) 8am, $0.59 - Preview

- EMC (EMC) 6:52am, $0.35 - Preview

- Gannett (GCI) 8:30am, $0.46

- General Dynamics (GD) 7am, $1.64 - Preview

- Gentex (GNTX) 8am, $0.45

- Ingersoll-Rand (IR) 7am, $0.26

- Johnson Controls (JCI) 7am, $0.65

- Lincoln Electric (LECO) 7:30am, $0.90

- Manpowergroup (MAN) 7:30am, $0.68

- Norfolk Southern (NSC) 8am, $1.15 - Preview

- Northrop Grumman (NOC) 7am, $2.15 - Preview

- Omnicare (OCR) 7am, $0.90

- Owens Corning (OC) 7:28am, $0.35

- Polaris Industries (PII) 6am, $1.16

- Popular (BPOP) 8am, $0.67

- Praxair (PX) 6:01am, $1.51

- Procter & Gamble (PG) 7am, $1.02 - Preview

- Reynolds American (RAI) 6:58am, $0.74 - Preview

- Ryder System (R) 7:55am, $0.87

- SEI Investments (SEIC) 8:30am, $0.40

- Supervalu (SVU) 7am, $0.15

- TD Ameritrade (AMTD) 7:30am, $0.34

- TE Connectivity (TEL) 6am, $0.91

- Thermo Fisher Scientific (TMO) 6am, $1.40 - Preview

- Tupperware Brands (TUP) 7am, $1.16

PM EARNS:

- Align Technology (ALGN) 4pm, $0.34

- Angie’s List (ANGI) 4:05pm, $(0.06)

- Apple (AAPL) 4:30pm, $10.17 - Preview

- AvalonBay Communities (AVB) 5:26pm, $0.82

- Cheesecake Factory (CAKE) 4:15pm, $0.49

- Chicago Bridge & Iron (CBI) 4:01pm, $1.12

- Citrix Systems (CTXS) 4:05pm, $0.59

- Crown Castle Intl (CCI) 4:01pm, $0.29

- E*Trade Financial (ETFC) 4:05pm, $0.23

- Equifax (EFX) 4:10pm, $0.87

- Everest Re Group (RE) 4:05pm, $5.42

- F5 Networks (FFIV) 4:05pm, $1.25

- Facebook (FB) 4:05pm, $0.24 - Preview

- Flowserve (FLS) 4:07pm, $0.75

- FNB (FNB) 4:15pm, $0.20

- Fortinet (FTNT) 4:15pm, $0.09

- Graco (GGG) 4:10pm, $0.82

- Ingram Micro (IM) 4:05pm, $0.48

- Lam Research (LRCX) 4:05pm, $1.17

- O’Reilly Automotive (ORLY) 6:30pm, $1.58

- Oceaneering Intl (OII) 4:01pm, $0.80

- Polycom (PLCM) 4:05pm, $0.14

- Qualcomm (QCOM) 4pm, $1.22

- Raymond James Financial (RJF) 4:16pm, $0.77

- ResMed (RMD) 4:05pm, $0.64

- Robert Half Intl (RHI) 4pm, $0.44

- Safeway (SWY) 4:05pm, $0.18

- ServiceNow (NOW) 4:01pm, $(0.08)

- Stryker (SYK) 4pm, $1.09

- Susquehanna Bancshares (SUSQ) 4:30pm, $0.21

- TAL Intl Group (TAL) 5:01pm, $0.96

- Teradyne (TER) 5:01pm, $0.06

- Texas Instruments (TXN) 4:30pm, $0.41

- Tractor Supply (TSCO) 4:01pm, $0.37

- TriQuint Semiconductor (TQNT) 4:02pm, $(0.12)

- Varian Medical (VAR) 4:02pm, $1.03

- Xilinx (XLNX) 4:20pm, $0.55

- Zynga (ZNGA) 4:04pm, $(0.01)

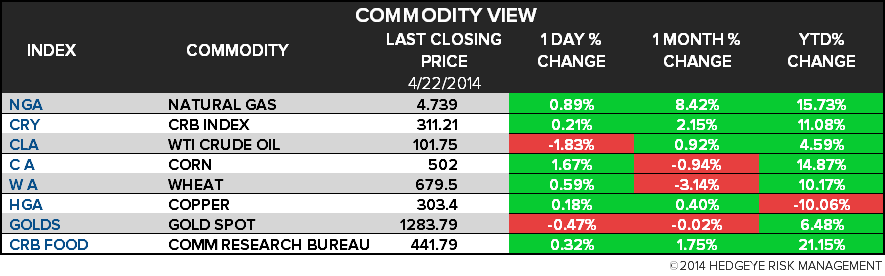

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Goldman Sachs Unbowed as Barclays Joins Commodities Exodus

- WTI Crude’s Discount to Brent Widest in Five Weeks on Supplies

- Investors Checking Out of ‘Hotel Mongolia’ in Limbo: Commodities

- Soybeans Post Longest Slump Since July as China Demand May Slow

- Copper Falls on China Factories as Nickel Touches 14-Month High

- Coffee Reaches 26-Month High as Brazil Drought Raises Volatility

- Gold Above 10-Week Low as Ukraine Weighed Against U.S. Recovery

- Rebar Advances Most in 2 Weeks on Inventory, China Reserve Ratio

- Monsoon Seen Below Normal to Normal in South Asia This Year

- LME Seeks to Lure Dinner Guests From Tables to Metal Trading

- Coal Glut Foils Price Rally With Miners Tied to Exports: Energy

- Japan May Offer Canada Head Start on Pork Duty to Sway U.S.

- China Move to ’Go Green’ May Mean Lower Copper Use

- Ukraine’s Unpaid Gas Bills Dwarf U.S. Offer Amid Shutoff Threat

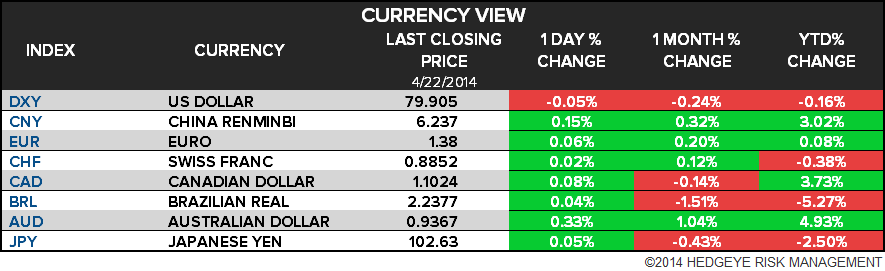

CURRENCIES

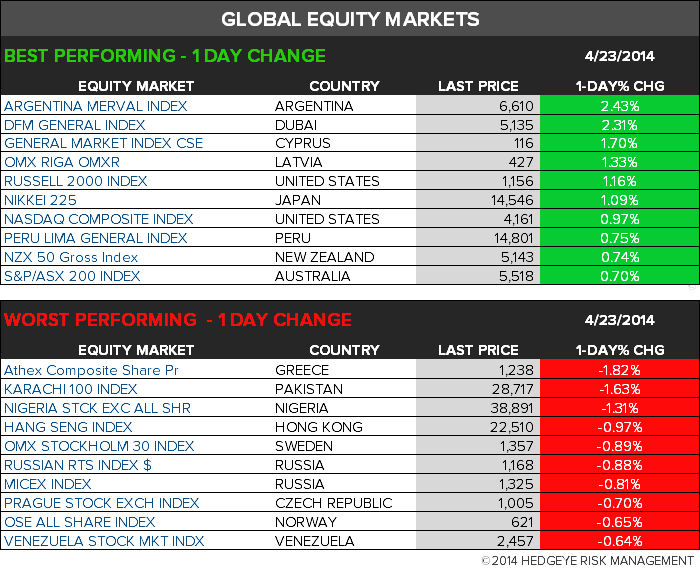

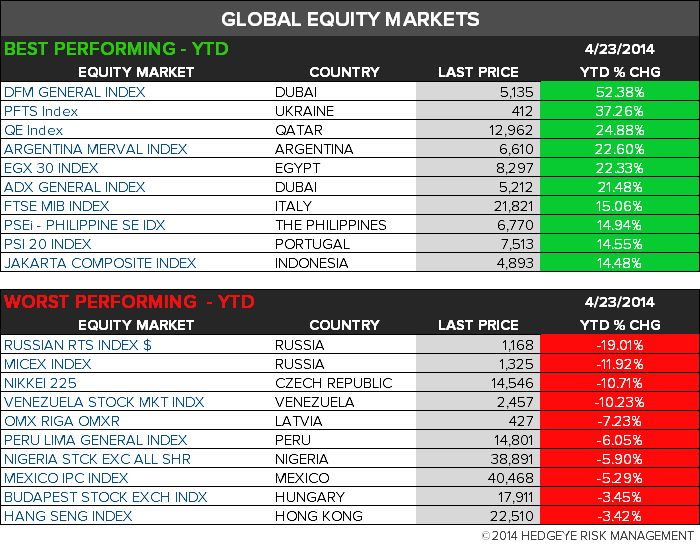

GLOBAL PERFORMANCE

EUROPEAN MARKETS

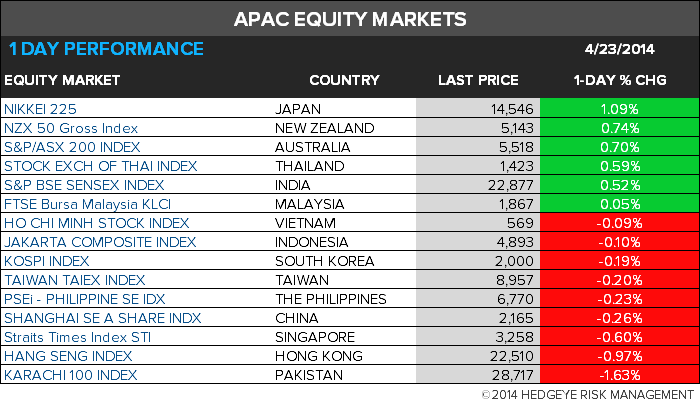

ASIAN MARKETS

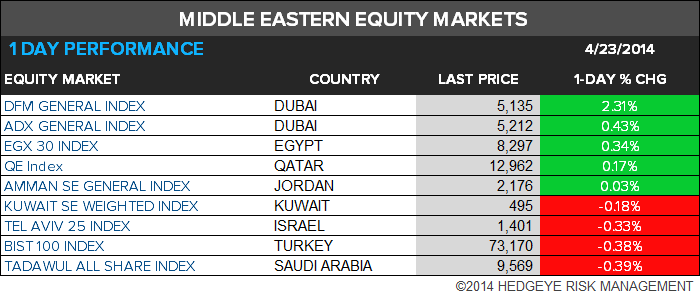

MIDDLE EAST

The Hedgeye Macro Team