SUMMARY BULLETS

- ATTRITION APPEARS MORE LIKELY: The larger the increase in enrollment on the public exchanges, the greater the IFP attrition risk to EHTH. The 8M enrollment estimate from President Obama suggests the risk is considerable.

- IFP MEMBERSHIP TO DECLINE 1Q14: The brunt of the cancellation risk will emerge in the 1Q print, while membership flow-through from Open Enrollment will be recognized over the 4Q13-2Q14 period.

- GUIDANCE CUT?: We believe top-end cut to 2014 revenues is likely, but not a definite. Management could choose to wait until it no longer can; in the interim preaching the long-term story.

ATTRITION APPEARS MORE LIKELY

HHS hasn’t releases March enrollment numbers yet. However, President Obama announced that 8M members have enrolled in private plans on the public exchanges (HIXs). The size of the addressable uninsured population (ex Medicaid eligible) is ~27M according Census data. So if every one of those 8M members were previously uninsured, the public HIXs penetrated ~30% of the uninsured market. However, we believe much of that enrollment data comes from the previously insured.

For perspective, when CHIP was expanded in 2009, only 1/6 of eligible parents (16%) applied for coverage for their children (link). So it’s hard to assume those 8M enrollees are purely organic (previously uninsured), especially since there isn’t much data to support that claim. McKinsey had previously estimated that 89% of the public HIX applicants were previously insured (link), but that data is somewhat dated at this point.

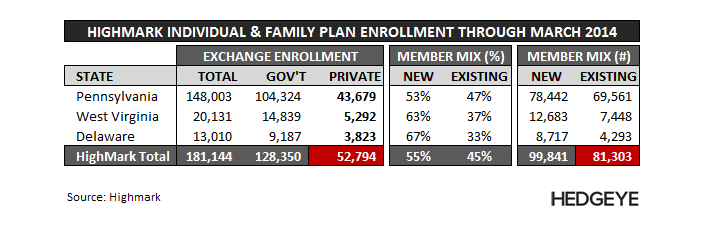

A more telling and current example is reported enrollment metrics from Highmark (link), which may be the only MCO that has disclosed both its enrollment mix between public and private HIXs, and the percentage of those enrollees that were previously insured by the company. The data suggests that 45% of its enrollees were previously insured by Highmark.

But more importantly, Highmark’s total enrollment into new private HIXs plans during Open Enrollment (~53K) is less than the number of its existing members that chose new plans (~81K). In short, the private HIXs ceded existing Highmark members to the public exchanges. That is attrition.

IFP MEMBERSHIP TO DECLINE 1Q14

A competitor published a note summarizing a meeting it had with EHTH CEO Gary Lauer in late March. The glaring takeaway from the report was that EHTH knew the churn status on less than 50% of its individual book; however EHTH IR refuted that comment when we contacted them. If it is true, that’s a scary statement this late into the year. If not, we still believe that membership will decline in 1Q14 regardless.

The main reason is that the brunt of EHTH's 2014 IFP cancellations will be recognized in 1Q14 because the company will be able to estimate the impact of forced plan terminations from ACA non-compliance (EHTH doesn't know until members stop paying).

At the same time, the bulk of approved members from Open Enrollment applications were either recognized in 4Q13 or will be recognized in 2Q14 given the timing of demand for health insurance and the lag to approval. We illustrate the latter point using EHTH's comScore web traffic and Google search traffic for Health Insurance in the charts below.

In short, this is the reverse setup of 4Q13 when we didn't know the cancellation data, but saw some of the flow-through in new membership from ACA open enrollment. Now the cancellation data will be exposed, and new membership will not be able to offset.

<chart5>

GUIDANCE CUT?

We believe top-end cut to revenues is likely, but not a definite. Management could wait until 2Q after seeing membership data from March applications and the trend in application volumes thereafter (which we expect to decline y/y).

At that point, 2014 may become less relevant as the "promise" of 2015 draws closer, especially since management will be doing everything they can do pump up the longer-term growth story. There isn't a near-term catalyst to refute the 2015 growth narrative, so unbridled bullish sentiment could take hold again; the same way it did in 2H13 through its 2014 guidance release when reality set in.

We remain short given the fundamental setup in the intermediate term. Our concern is the return of undue optimism on the longer-term story. You can read more about our longer-term concerns here (EHTH: Déjà vu)

Hesham Shaaban, CFA

@HedgeyeInternet