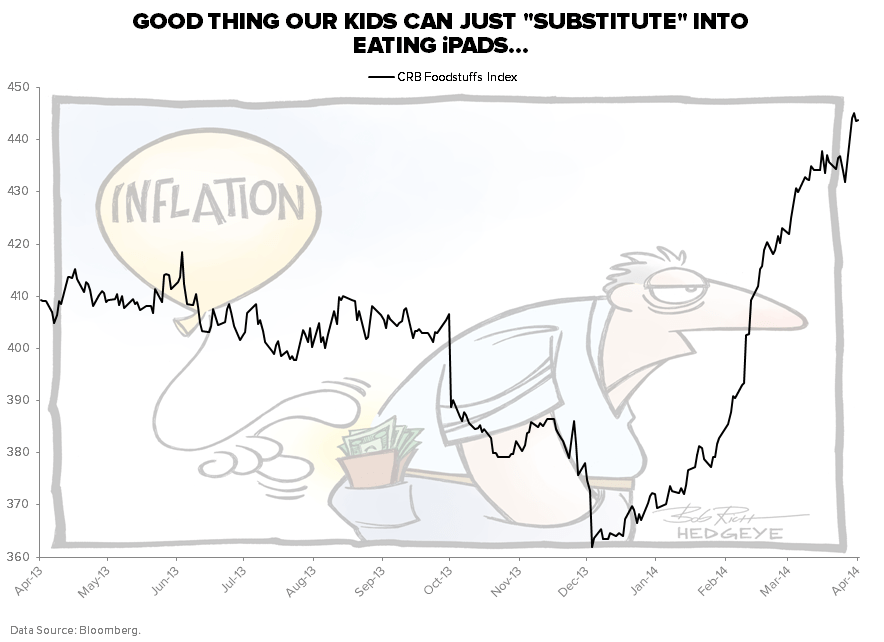

The CRB Food Index jumped another +2.7% last week. It’s now closing in on +22% year-to-date.

Soybeans were up +3.8% last week to just shy of +19%, Coffee was up another +0.3% to over +77%, etc, etc.

This is a major tax on US #ConsumerSlowing.

Our advice? Stick with the inflation slows consumption growth theme.