SUMMARY BULLETS:

- GREEN SCREEN MACRO: Paint whatever eco growth picture you want. And remember, when in doubt, herd your point estimate for growth right on the current consensus and… always, always, bake in the back-half ramp

- TRACKING THE BOUNCE: Is anyone not expecting a bounce in the reported March/April fundamental data? We continue to think the 2014, growth-slowing playbook remains the relevant one.

- INITIAL CLAIMS - April Flowers: A 4th week of accelerating improvement. The numbers for the MTD are supportive of a strong April jobs report.

- #InflationAccelerating: Food, energy, and housing are all key cost centers for the consumer and with inflation in each currently running at a premium to wage growth, share of wallet for other discretionary purchasing will remain under pressure

- #HousingSlowdown: The pervasive deceleration in housing activity to start the year has extended itself into March/April - across geographies. The West, not the Northeast, has looked the worst.

- Policy Thoughts: The Ticking Clock - The Fed needs to get out if only to allow themselves to (credibly) get back in. The tock is ticking on the current expansionary cycle.

Macro’s Green Screen

Listening to Yellen’s remarks and the referencing of her now enigmatic “dashboard” yesterday while staring at consensus growth estimates for 2014 provided his year’s most potent reminder that professional macro forecasting remains very much a storytelling exercise.

Indeed, for Fed tea leaf readers, the chess match that has become massaged messaging to markets under the Fed’s fledgling, increased transparency directive only adds another distortive layer to the storytelling.

For forecasters..remember, when in doubt, herd your point estimate right on current consensus (which at a round 3% is, itself, just an un-imaginative expectation for a return to pre-recession Trend line growth) and always, always, bake in the back-half ramp

SLOPE STACKING: Tracking the Bounce

With a host of domestic macro metrics recording some of the biggest sequential declines in history in the weather distorted, Dec-Feb period, is anyone not expecting a bounce in the reported March/April fundamental data?

What we’d like to see, in short, is the slope of growth track back towards the levels that characterized the heart of the 2013 acceleration.

Thus far, the March/April data has been mixed as most measures have shown sequential improvement, but haven’t exhibited a material, rebound effect that would be suggestive of deferred activity and certainly haven’t retraced the cumulative declines realized in the peri-new year period.

With the dollar holding in bearish formation, 10Y yields broken (& declining in the face of the last few, low volume equity rallies), and inflation still rising alongside increasingly harder growth/inflation comps through 3Q14, we continue to think the 2014, growth-slowing playbook remains the relevant one.

Initial Claims: April Flowers for Labor

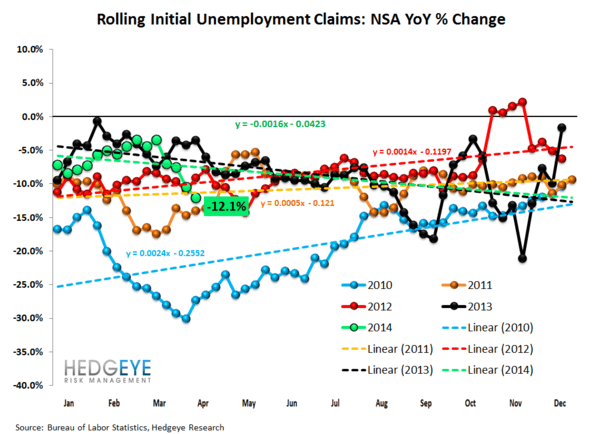

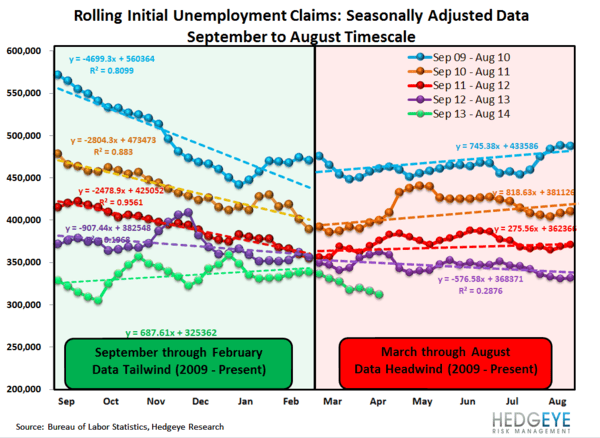

Initial Claims has been the notable positive diverger from a fundamental data perspective over the last month.

This morning’s labor data extended the streak of accelerating improvement to four consecutive weeks as the 4-wk rolling average in non-seasonally adjusted claims improved to -12.1% YoY vs. -10.5% the week prior.

The trend in headline, seasonally-adjusted claims was similar with the 4-wk rolling average falling -4.25K WoW to 312K, the lowest level since August of 2007.

As Josh Steiner, our head of Financials research at Hedgeye, re-highlighted this morning:

The weather's turn, particularly in the Northeast, remains coincident with the turn in the claims data. Based on the numbers so far, it looks like the April job's report will come in quite strong.

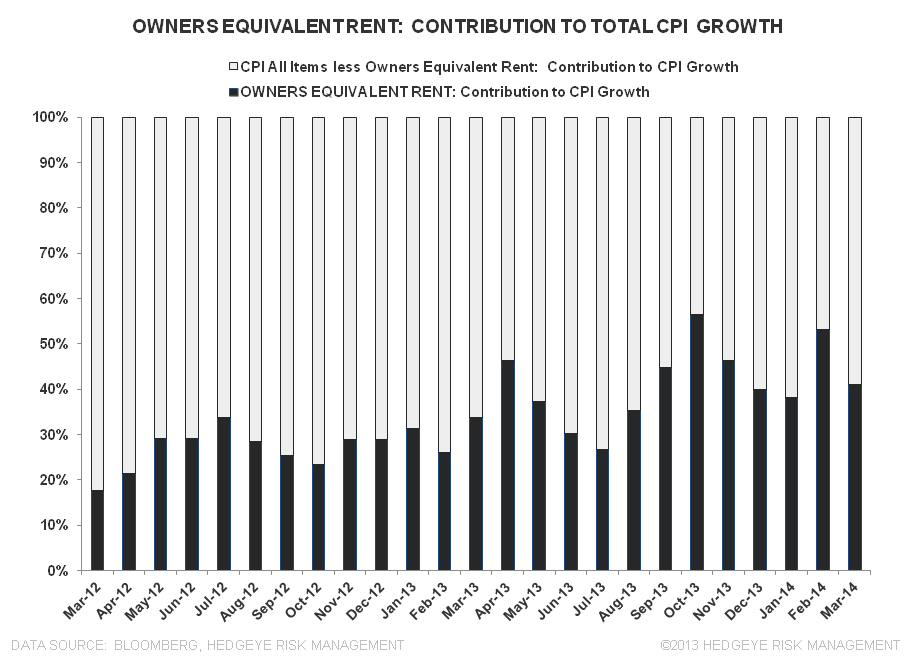

#InflationAccelerating: Headline CPI inflation accelerated +40bps sequentially to +1.5% YoY while Core CPI accelerated +10bps to +1.7% YoY in March. Under the hood, the existent trends extended themselves as food, energy, and shelter price growth all continued to accelerate.

Real Hourly Earnings of Production & Non-Supervisory Employees grew +0.8% YoY in March according to BLS data released Tuesday – a sequential deceleration of 70bps vs. the +1.5% YoY growth recorded in February – and nominal spending continues to grow at a positive spread to incomes

Food, energy, and housing are all key cost centers for the consumer and with inflation in each currently running at a premium to wage growth, share of wallet for other discretionary purchasing will remain under pressure.

Further, with household savings rates already at the low end of the historical range, consumer credit growth (ex-auto’s & student loans) tracking sideways, equities down YTD and housing slowing, the capacity for non-wage related factors (i.e. credit, reduction in savings, wealth effect) to support incremental consumption growth appears constrained.

Core PCE inflation, meanwhile, continues to list at ~+1.0% YoY. Persistent, sub-2% PCE inflation gives the Fed latitude to further talk down the dollar which, in our view, will only perpetuate rising inflation and, by extension, a slowdown in domestic consumerism.

Source: Hedgeye Financials

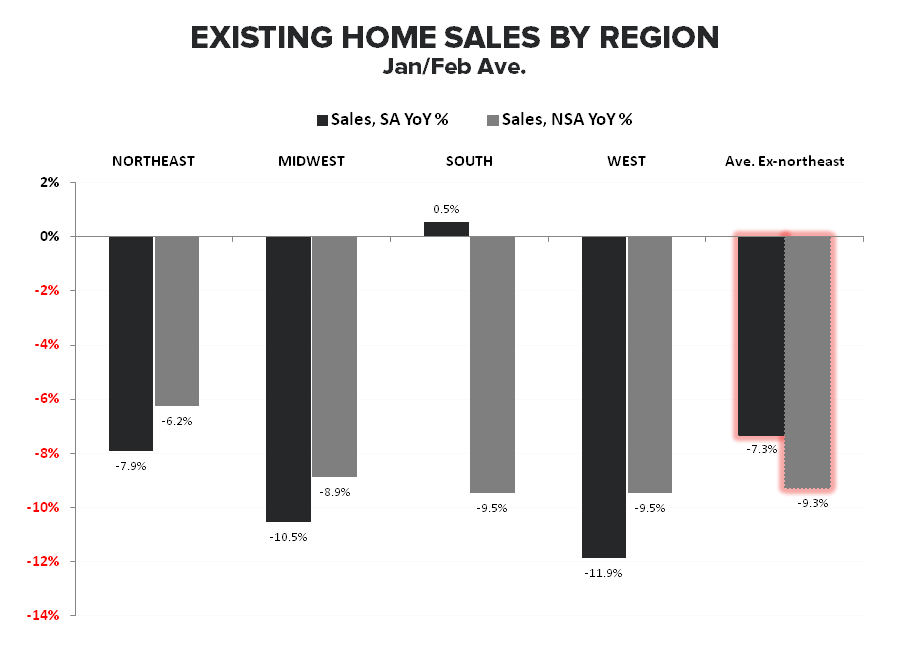

#HousingSlowdown: The pervasive deceleration in housing activity to start the year has extended itself into March/April - across geographies. The West, not the Northeast, has looked the worst.

- NAHB HMI: Headline NAHB confidence increased 1pt MoM in April vs the downwardly revised March print. Notably, with the exception of the Northeast, builder confidence was flat or down across geographies. Confidence in the West region slid for a third consecutive month to 45, continuing its expedited drawdown from a peak reading of 71 just three months ago.

- Mortgage Applications: Yesterdays purchase application index rose 1.3% WoW but remains -17% off the May 2013 peak. Similarly, the composite index (purchase + refi) gained +4.3% WoW but remains in free fall at -58% YoY. We continue to believe the confluence of QM implementation, declining affordability, and a slowing consumer will drag on housing demand, with home prices responding on a lag.

- Housing Starts/Permits: Housing starts rose 26K MoM but missed estimates by a comparable amount while Building Permits went sub-1MM, declining -2.4% MoM to 990K. On a relative basis, supply/demand/price dynamics in the new home market continue to compare favorably to those in the existing market. Buyer demographics and the cumulative deficit in new housing units built since the recession should help buttress the relative downside in new construction activity.

Quasi-random policy thoughts: The Ticking Clock

By FOMC admission, the juice on QE has been largely exhausted and the risk/reward balance has shifted. If anything at this point, the Fed needs to get out if only to allow themselves to (credibly) get back in.

A cessation of QE alongside decent macro data accomplishes two things.

First, from a messaging perspective, it signals confidence in the ability for the private sector to carry the recovery forward.

Second, stopping QE while the fundamental data is supportive implies that QE was (at least in part) effective in its objective. Some measure of perceived effectiveness by the market allows them to come back to it should they need to.

Perma-QE, however, is de-facto admission of its ineffectivenss, leaving it largely impotent as a forward policy tool.

The line of thinking above isn’t necessarily new or novel but, as of April, the duration of the current expansion stands at 59 months – exactly the mean duration of expansions following recessions over the last 100 years.

Sure, balance sheets recessions are defined by slower recoveries with lower amplitude, but you think the Fed is completely unaware of the ticking clock?

Enjoy the long weekend.

Christian B. Drake

@HedgeyeUSA