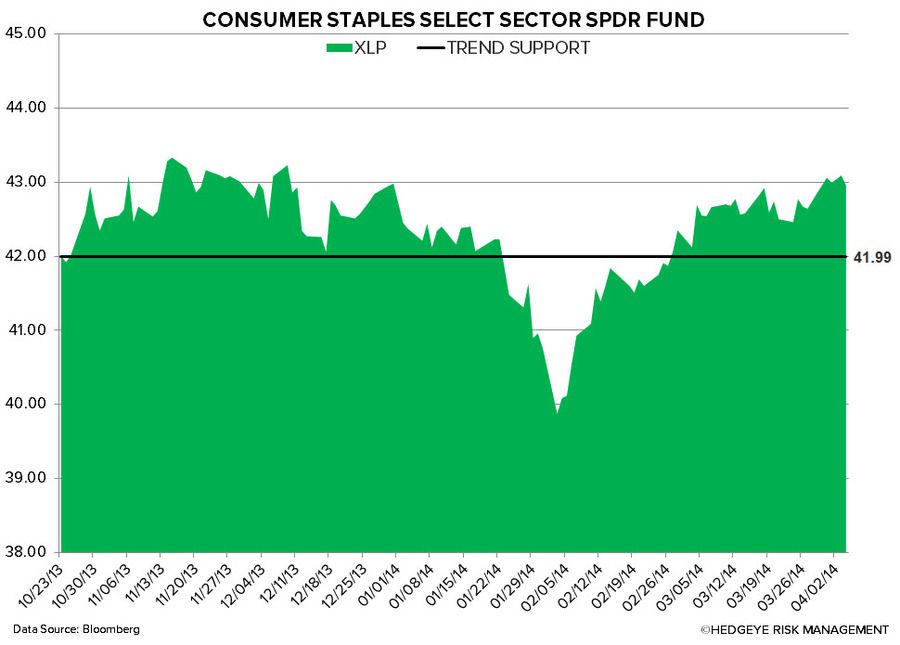

Consumer Staples (XLP) outperformed the broader market last week, falling -0.5% versus the S&P 500 at -2.6%. XLP is down -0.5% year-to-date vs the SPX at -1.8%.

For a sixth straight week, XLP is bullish on immediate term TRADE and intermediate term TREND durations from a quantitative set-up. This is a material shift as the sector traded bearish TRADE and TREND for the majority of the year-to-date.

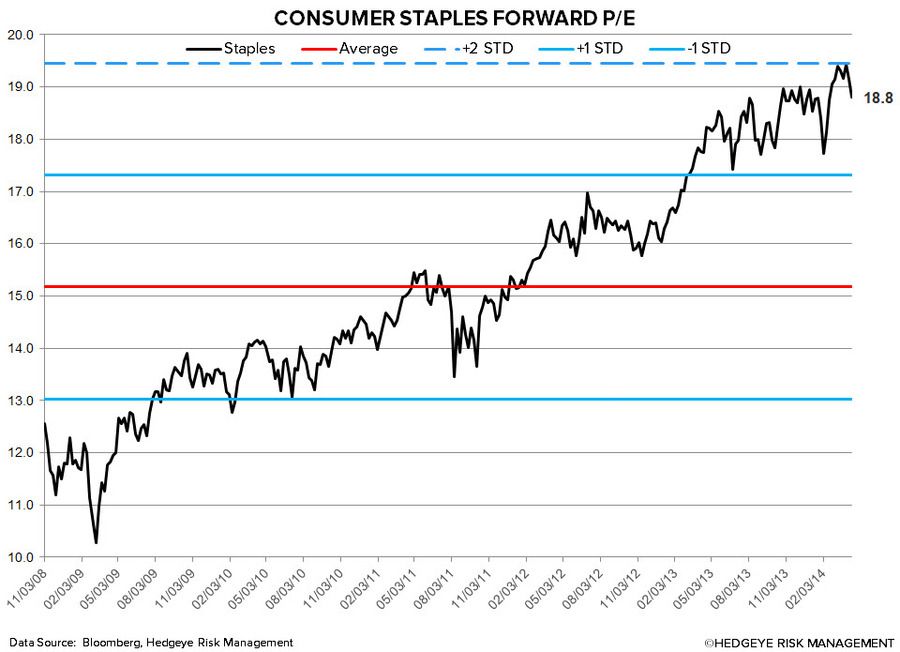

Despite the bullish quantitative set-up for the sector, we continue to believe that the group is facing numerous headwinds, including:

- U.S. consumption growth is slowing as inflation rises, in-line with the Macro team’s 2014 Q1 theme of #InflationAccelerating, and Q2 theme of #ConsumerSlowing.

- The economies and currencies of the emerging market – once the sector’s greatest growth engine – remain weak with the prospect of higher inflation in 2014 eroding real growth.

- The sector is loaded with a premium valuation (P/E of 18.8x).

- Less sector Yield Chasing as Fed continues its tapering program.

- The high frequency Bloomberg weekly U.S. Consumer Comfort Index has not seen any real improvement over the past 6 months, and declined to -31.9 versus -30.0 in the prior week.

* * * * * * *

Editor's Note: This is an excerpt of a research note that was originally provided to subscribers on April 14, 2014 by Hedgeye Consumer Staples Analyst Matt Hedrick. Follow Hedgeye's Consumer Staples sector @HedgeyeStaples.

subscribe to Hedgeye.