This note was originally published at 8am on April 02, 2014 for Hedgeye subscribers.

“We shall not cease from exploration, and the end of our exploring will be to arrive where we started and know it for the first time.”

-T.S. Eliot

Yesterday we held our quarterly firm meeting in Stamford, CT. It was by all accounts a very successful day. We introduced new employees, celebrated recent wins and also contemplated strategic shifts to keep Hedgeye moving forward.

As an aside, it also coincided with my personal favorite day of the year, April Fool’s Day. Unlike those April Fool’s days of prior years, like when I fired Keith one year, this year’s joke was more benign, though we did manage to “suck” a few people in again. For those that didn’t see the faux press release about Wall Street 2.0: Hedgeye the Movie, it can be found here.

So at the company meeting, a key topic of discussion was how to generate contagious content / ideas. For those that didn’t know, the term, “content is king”, was first used in 1994 and then popularized by Bill Gates in an essay about two years later. So, as ideas go, the idea of content is king is not new, but it is certainly contagious.

Back to the Global Macro Grind...

In my mind, activist investment ideas are examples of ideas that need to become contagious before they become successful. Yesterday activist Starboard filed a presentation outlining the potential for Darden Restaurants ($DRI). A key take away from the presentation is that the Company’s EBITDA margins are at 7.4% versus the industry median of 10.3%.

As many of you know, Darden is also currently a favorite of Restaurant Sector head Howard Penney and is on our Best Ideas list. As a result, Starboard was kind enough to reference our work on Darden in their presentation. Specifically, they referenced a recent poll that we did:

“According to a recent poll conducted by sell-side research firm Hedgeye Risk Management, 84% of respondents said that they did not believe that management’s plan to spin-off Red Lobster would create value.”

We actually have created a polling product to specifically gauge sentiment and opinion in a more quantified fashion, which has, obviously, also had the derivative impact of creating contagious content.

Included in the Starboard presentation as well was this tweet from Penney:

“$DRI management shuts me out of another earnings call. Running out of time is not an excuse. @jannarone article on #CNBC was $$”

This point goes to the crux of Penney’s thesis on Darden, which is that management operates in a vacuum and is totally unwilling to listen to new ideas, especially from analysts that may disagree with them. Ignoring great ideas is the death knoll for any company. If you’d like to learn more about our thesis on Darden before it goes too viral, please email sales@hedgeye.com.

While we are on the topic of contagious content, I thought it would be worth highlighting an essay that Warren Buffett wrote for Fortune in 1977 (back when periodicals like Fortune still published essays):

“There is no mystery at all about the problems of bondholders in an era of inflation. When the value of the dollar deteriorates month after month, a security with income and principal payments denominated in those dollars isn't going to be a big winner. You hardly need a Ph.D. in economics to figure that one out.

It was long assumed that stocks were something else. For many years, the conventional wisdom insisted that stocks were a hedge against inflation. The proposition was rooted in the fact that stocks are not claims against dollars, as bonds are, but represent ownership of companies with productive facilities. These, investors believed, would retain their Value in real terms, let the politicians print money as they might.

And why didn't it turn but that way? The main reason, I believe, is that stocks, in economic substance, are really very similar to bonds.”

As you can see this basic concept that we have been pounding on, which is that when a currency is devalued that devaluation naturally creates inflation in dollar denominated asset classes, is not new. Neither is the idea that at a point, this inflation begins to negatively impact economic growth, which has the potential to have a negative impact on the returns of those assets classes levered to economic growth.

Certainly, of course, we aren’t suggesting we are in the midst of 1970s style inflation. Or, frankly, on the path to that any day soon, but commodity inflation is here, is persistent and is likely to be sticky. Most notably on the inflation front is what is happening to food (you know that stuff we eat).

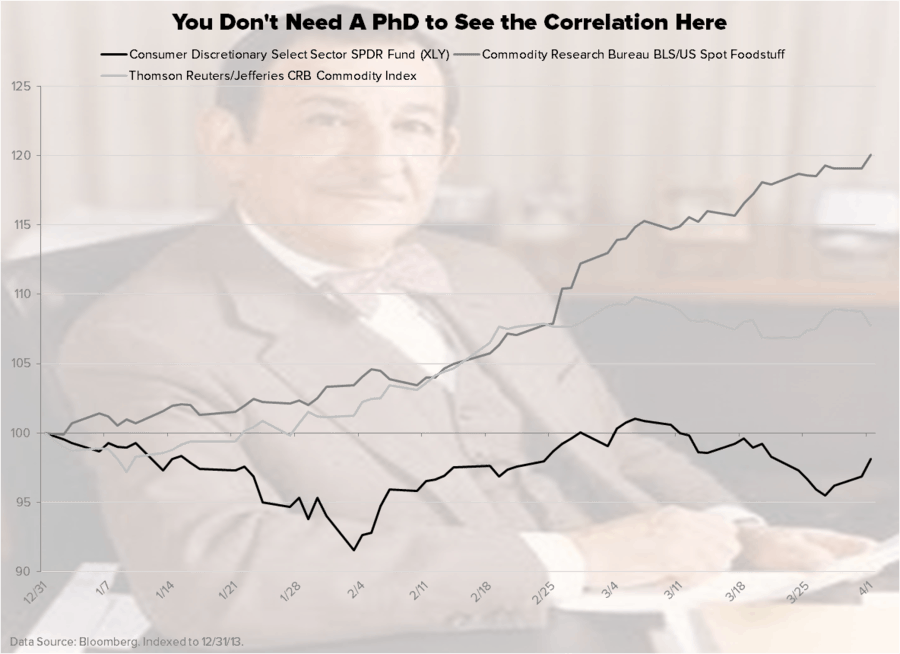

In the chart of the day below, we’ve compared the performance of consumer discretionary stocks in the year-to-date versus the CRB Index versus the BLS Foodstuff Index. For those that can’t read the fine print, I’ll give you the punch line. The CRB commodity index is up more than 7% in the year-to-date, the BLS Foodstuff Index is up more than 20%, and consumer discretionary stocks are down on the year.

As Warren Buffett might say, you don’t need an economics PH.D. to see that correlation!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.66%-2.80%

SPX 1856-1888

VIX 13.01-14.72

USD 79.91-80.40

Gold 1270-1321

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research