TICKERS: PENN, DRH

EVENTS TO WATCH: UPCOMING EARNINGS / CONFERENCES / RELEASES

Wednesday, April 16

- HTZ at BAML Auto Summit

Thursday, April 17

- Iowa Racing & Gaming Commission Meeting - scheduled to decide whether it will grant Cedar Crossing Casino a state gaming license, which would make the facility the 19th casino in Iowa.

- GE 1Q14 Earnings – 8:30 am Conf Call – real estate comments?

- BX 1Q14 Earnings – 11 am Conf Call PIN 149 943 55 – lodging comments & color?

- TZOO Earnings – 11 am Con Call

- DIS – Investor Day – cruise & parks commentary?

Monday, April 21

- Genting Singapore – Annual General Meeting

Tuesday, April 22

- IGT FQ2 earnings: 5 p.m. Conf Call , Passcode: IGT

Thursday, April 24

- WYN Q1 earnings - 8:30 a.m. , Passcode: Wyndham

- LHO Q1 earnings - 9:30 a.m.

- PENN Q1 earnings - 10 a.m.

- HOT Q1 earnings - 10:30 a.m. , Passcode: 12049644

- LVS Q1 earnings - 4:30 p.m. ; PW: 18236529

COMPANY

PENN - Continental Real Estate Cos, based in Columbus Ohio, is negotiating with PENN to buy and redevelop the Beulah Park property, which will cease to be a racetrack in May. Beulah Park will hold its final thoroughbred horse races on Derby Day, May 3, and then will close. PENN will transfer the site's gaming license to Hollywood Gaming at Mahoning Valley (Youngstown).

TAKEAWAY: The monetization of a hidden asset on PENN's balance sheet.

DRH - sold the 386-room Oak Brook Hills Resort for $30.1 million, including $4.0 million of seller financing or approximately $78k/key.

TAKEAWAY: Seems to be a very low price per key, but deferred capex likely a hurdle to getting a better price.

INDUSTRY

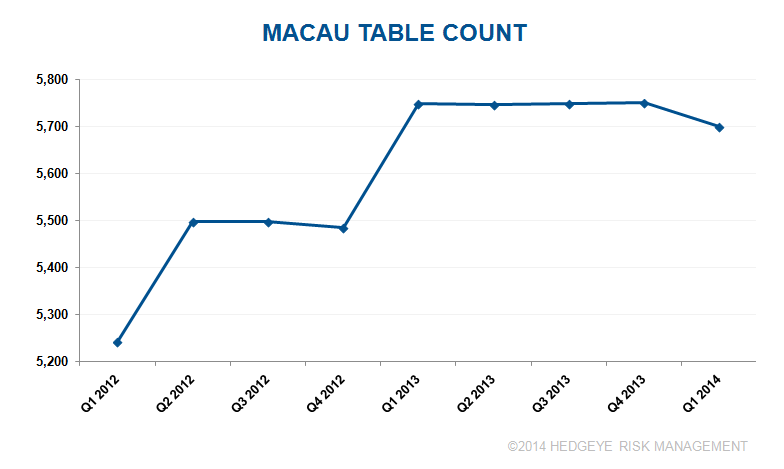

Macau table/slot count Q1 2014 DICJ Gaming tables sequentially declined from 5,750 in Q4 2013 to 5,700 in Q1 2014. Slot machines sequentially rose from 13,106 in Q4 2013 to 13,232 in Q1 2014.

TAKEAWAY: The slight table decline in Q4 is a little surprising given all the fuss over lack of tables.

VIP Player Scrutiny - The Treasury Department is seeking to enforce Article 31 of the Bank Secrecy Act, which was enacted over 10 years ago. The Treasury Department claims Las Vegas Strip casinos are years behind other financial institutions in handing over their data and customer lists. Fred Curry, a partner with Deloitte Financial Advisory Services, says it is only “a matter of time” before such information is going to be handed over.

TAKEAWAY: Clearly not a positive for the casino industry, this could also lead to increased audits by the Internal Revenue Service based on suspicious activity.

Japan Gaming Congress -http://www.japangamingcongress.com/

TAKEAWAY: The Yumeshima annoucement yesterday shows Japan interest is heating up. This conference is held before the May debate on a possible casino bill.

Macau Infrastructure - the China high speed train between Beijing and Guangzhou will be delayed from 2015 to 2016 and expected to open for passenger services in 2017.

TAKEAWAY: A near term negative for the mass segment growth.

Vietnam Gaming - Casino operator Donaco International cleared the final regulatory hurdle in its bid to open a new hotel and casino in Northern Vietnam with a focus of attracting Chinese gamblers in the bordering Yunnan province. The company is run by Joey and Ben Lim who are nephews of casino magnate K.T. Lim, the founder of Malaysian conglomerate Genting Berhad. Genting Hong Kong, which is part of Mr Lim's empire, has a strategic stake in casino operator Echo Entertainment Group. The five star 428-room hotel and casino is now slated to open in a "soft launch" on May 18th.

TAKEAWAY: This is a foreigners only casino. Vietnam's upcoming pilot project ($7BN Van Don Casino), which would be open to locals, is the real prize.

Atlantic City Property Comp – based on company filings by Bally’s Atlantic City casino, TJM Properties, the buyer for the former Claridge Casino/Hotel in Atlantic City paid $12.5 million for the property.

TAKEAWAY: Another low transaction price in a fading market.

MACRO

China - Q1 GDP growth: +7.4% YoY vs +7.3% consensus and +7.7% YoY in prior quarter

TAKEAWAY: A beat off of a lowered number

China 1Q14 Home Sales Decline - (Bloomberg) home sales fell and new property construction declined 25% in Q1, as credit remained tight, adding to signs of a slowdown. The value of homes sold fell 7.7% year/year to 1.1 trillion yuan (US$177 billion) and the last time home value sales dropped in 1Q2012.

TAKEAWAY: A key metric that bodes poorly for China

China Shadow Banking (Business Times) - Chinese companies that have lent money to other companies are facing a potential wave of defaults, with several firms reporting missed loan repayments, including Sainty Marine and Qiaqia Food Co. According to Chinese Central Bank data, the shadow banking industry granted a net 2.55 trillion yuan ($411 billion) in so-called entrusted loans last year, nearly double the total for 2012, making them the second-biggest source of domestic credit behind bank loans.

TAKEAWAY: No doubt Chinese government is keeping a close watch on shadow loan defaults. Could impact Macau VIP

Hedgeye remains negative on consumer spending and believes in more inflation. Following a great call on rising housing prices, the Hedgeye Macro/Financials team is turning decidedly less positive.

TAKEAWAY: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.