Overview

The Hedgeye Macro team have presented their 2Q Macro themes and, as usual, it was data rich, timely, and insightful. The Macro Themes calls have too enviable forecasting track record to ignore. Below, we touch on how this quarter’s themes relate to parts of the Industrials sector. The themes of a slowing consumer, structural inflation, and a housing slowdown have implications for the sector and its performance relative to broader indices. We also highlight key transport data that shows broader resilience into 2Q 2014.

Commodity Price Divergence

Consumer oriented commodities, such as food/agricultural commodities, have increased much more than many industrial inputs, like copper or oil. Large supply increases in several metal categories and weaker emerging market demand may be pressuring industrial metals. Rising prices for consumer necessities may be negative for spending on other more discretionary categories.

Capacity Utilization

While some slack remains, corporations have tended to repurchase shares and pay dividends rather than invest in capacity in recent years. Long-term, that may conceptually result in too little of the right capacity in the appropriate places. One person’s inflation may prove to be another person’s pricing power, potentially benefiting well-positioned manufacturers. North American heavy truck fleets appear to be a compelling example of this theme, discussed below.

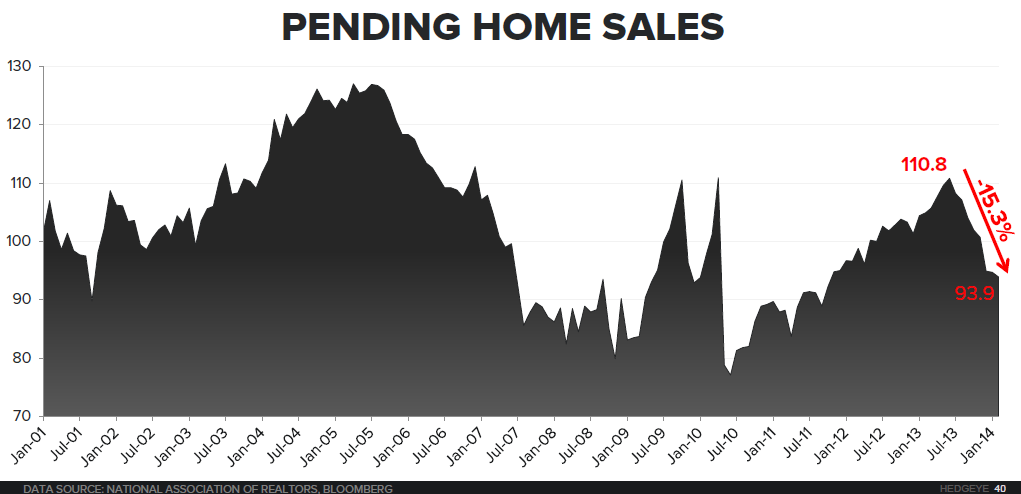

Housing Slowdown

A variety of factors, from new mortgage rules (QM) to higher interest rates, appear to be pressuring housing activity.

Residential Construction

While still posting strong year-on-year growth, there appears to be a deceleration in new residential construction spending. Weather is a likely contributor, but the broader trends are also potential drivers.

Truckload Rates

Truckload rates have been rising as fleet utilization is at decade-plus highs. Truckers have been hesitant to invest in capacity growth in recent years. It is a potential positive for PCAR and other Truck OEMs, while likely negative for truckload 3PLs that are structurally short capacity.

Heavy Truck Backlog to Build (North America)

The environment for Heavy Truck OEMs appears better, in part due to higher equipment rates. However, we would generally see a high reading on this index as an exit signal should it continue to improve.

China Exports

Recent increases in the CRB index are particularly noteworthy given signs of weaker Chinese activity. China is often viewed as the key swing consumer of commodities.

Cass Freight Index

The 1.144 March read of the Cass shipment index is at the high-end of its range in recent years.

IATA FTK Growth

International air cargo growth continues to improve, a positive sign for carriers.

Intermodal Rail Traffic

Intermodal traffic has rebounded smartly, partly reflecting better weather through March.

* * * * * * *

Editor's Note: This is an excerpt of a research note that was originally provided to Industrials Pro subscribers on April 11, 2014 by Hedgeye’s Industrials Sector Head Jay Van Sciver. Follow Jay on Twitter @HedgeyeIndstrls.