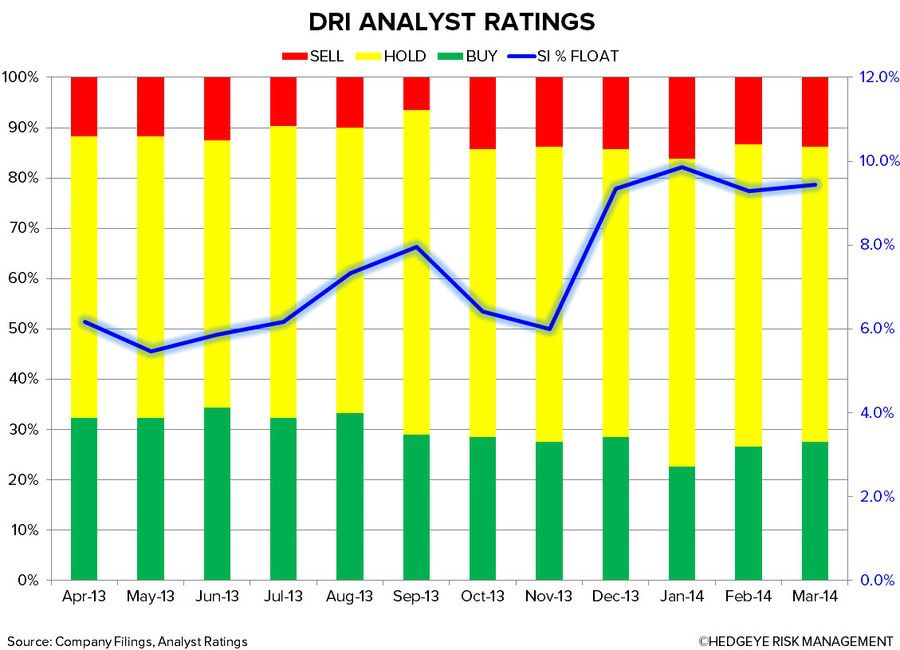

Darden Restaurants Inc. (DRI)

Despite ugly trends at its flagship brands, shaky fundamentals and management’s calculated, concerted effort to rid shareholders of their rights, we continue to believe DRI presents a strong investment opportunity due to its compelling inherent value.

That said, our long thesis is dependent on the success of activist investors Starboard Value and Barington Capital. If the activists are successful in preventing the Red Lobster spinoff and facilitating major changes at Darden, we believe there is significant upside potential. We look to Brinker International as the most recent example of a flailing company with an over-concentrated, complex portfolio to dwindle down its portfolio, refocus and create significant shareholder value. We believe this is possible with Darden, but the current management team appears unwilling to enact such change.

As we’ve said before, we believe Darden’s greatest opportunity for value creation lies within its crown jewel, Olive Garden, and to a lesser extent, Red Lobster. These two brands accounted for approximately 69% of Darden’s 3QF14 revenues despite tumultuous same-restaurant sales and traffic trends. While Darden has publicly addressed these two issues, we believe their plans (Olive Garden Brand Renaissance and Red Lobster Spinoff) are not only inadequate, but in the case of Red Lobster, value destructive.

ISS and Glass Lewis released reports last Friday recommending shareholders submit consents to Starboard in its ongoing effort to call a Special Meeting to put the Red Lobster spinoff to vote. We believe Starboard will get the majority vote and will put the right plan in place to turnaround the aforementioned chains and drive value creation.

DRI is trading at 18.18x P/E and 9.07x EV/EBITDA on a NTM basis.

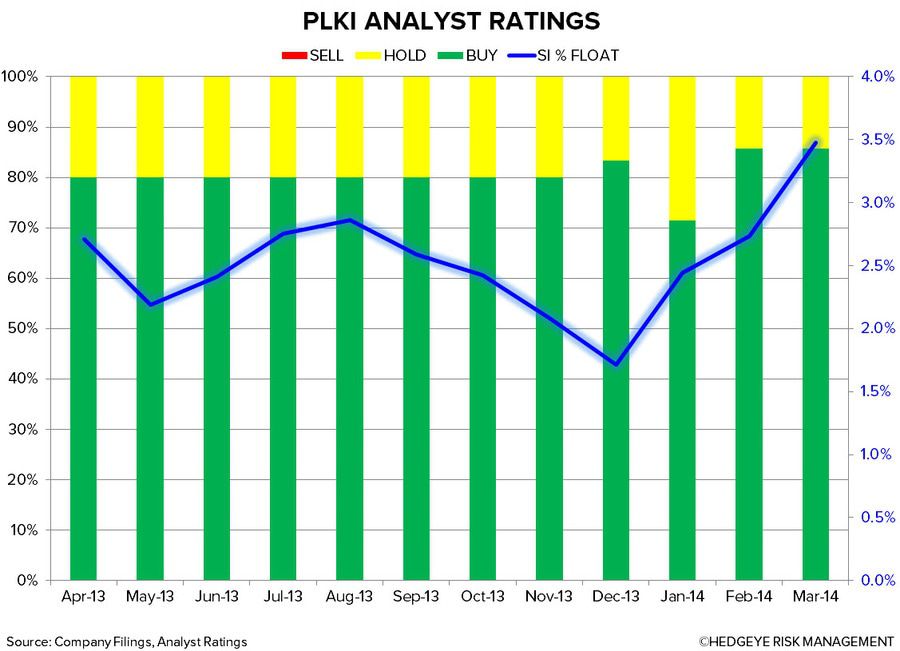

Popeye’s Louisiana Kitchen, Inc. (PLKI)

PLKI has been on our Watch List as a long for quite some time and we’re now adding it to our Investment Ideas list. PLKI is an operationally sound, strategically focused company with considerable brand momentum and modern day relevance. Given the considerable growth opportunity that lies ahead, both domestically and internationally, and a stringent, calculated plan to capitalize on this, we are bullish on the stock. Popeye’s diversified revenue stream and strong, stable cash flows mitigate the risk typically found with consumer growth stocks.

There are many things we like about PLKI, notably its strong management team led by CEO Cheryl Bachelder and a group of executives who have led the brand’s turnaround beginning in 2009. Under the current leadership, Popeyes has established a laser-focused strategy and clear path for consistent shareholder value creation. Last night, news hit that CFO H. Melville Hope III will be stepping down on May 23rd to pursue other opportunities. The company has begun a search for his successor. We don't view this as a huge deal and believe the Mr. Hope is leaving the company in a strong organizational and financial position. Any sell-off related to this news could present a strong buying opportunity.

PLKI’s efficient, asset-light model, healthy margins, current initiatives and feasible, material growth opportunities give us reason to believe they can successfully generate at least 13-15% EPS growth over the long-term. As it stands, we believe street estimates for 13% EPS growth on 14% sales growth in FY14 are conservative.

In our view, barring a sector-wide correction, PLKI’s risk/reward setup is too attractive to ignore, with limited downside and notable upside. We plan to release a full report running through our thesis next week.

PLKI is trading at 25.75x P/E and 14.04x EV/EBITDA on a NTM basis.

Jack in the Box Inc. (JACK)

JACK continues to be one of our favorite longs in the quick service space as we continue to believe its long-term potential is underappreciated, particularly with respect to the future growth of Qdoba. The company’s pivot to a defensive, asset-light model has proven wise and led to significant operating margin gains. We expect recent initiatives and same-store sales gains to continue to accelerate through FY14 as JIB continues to build upon the late night and breakfast dayparts and Qdoba identifies ways to differentiate its brand and attract new customers.

JIB has been a pleasant surprise to many investors amid its recent string of success. Reimaged restaurants and resonant advertising campaigns have helped company restaurants generate higher AUVs and margins, while improving franchise profitability. The late night and breakfast dayparts have been accretive to sales and continue to present an opportunity for future growth. Menu innovation continues to be a catalyst, while tighter operations (refranchising, lower food and packaging costs) have helped sales flow through to the bottom line. Improving speed of service continues to be a major opportunity moving forward.

Qdoba continues to be an underappreciated piece of the JACK story and one that we believe should be awarded a growth multiple. The Qdoba brand is working closely with Boston Consulting Group as it continues to develop its brand positioning strategy and effectively differentiate itself in order to retain current guests and attract new guests. An important part of this repositioning effort has been closing unprofitable stores in markets with poor brand awareness. According to management, they have identified clear opportunities to reposition the Qdoba brand and set the stage for strong performance moving forward. A big part of this strategy will include product innovation and the introduction of more LTO’s to drive traffic and trial. Catering growth continues to be a bright spot at Qdoba. We expect management to open approximately 42 Qdoba restaurants system-wide in FY14.

JACK currently trades at a discount to its QSR peers despite the potential to grow operating margins by 340 bps and EPS by +25% in FY14. In addition to considerable momentum, a strong balance sheet and notable free cash flow generation, management appears ready and willing to continue buying back shares through an aggressive repurchase program which was recently raised to $260mm. Indications are this program will be completed by FY15 and should contribute meaningfully to EPS growth.

JACK is trading at 23.34x P/E and 10.20x EV/EBITDA on a NTM basis.

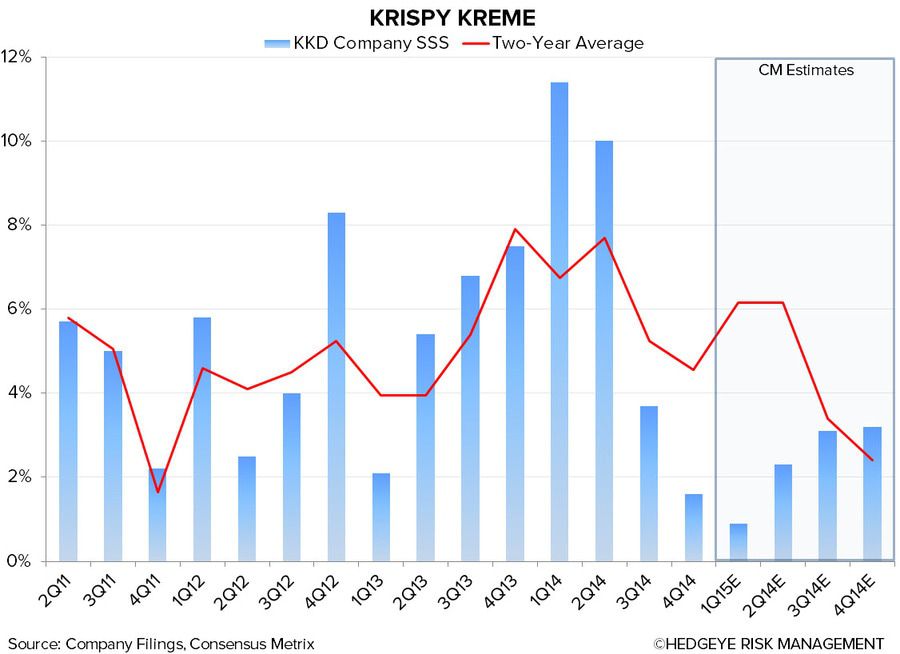

Krispy Kreme (KKD)

Despite selling off hard towards the end of 2013, KKD remains one of our favorite small cap growth companies. Over the past three years, the company has transformed itself into a strong regional brand and positioned itself as an asset-light business with unique global growth potential. KKD is a rapidly growing company with a strong financial profile.

KKD has plans to increase its system-wide unit count from 828 at the end of FY14 to 1,300 (400 domestic, 900 international) by the beginning of 2017. KKD international franchisees pioneered the initial development of smaller, satellite shop formats that generated stronger returns for owners. This model has translated to the U.S. and is an integral part of the company’s domestic growth model. We believe these formats will continue to resonate with the franchisee community and give them the confidence to incorporate these smaller models into their expansion plans.

Given the difficult comps, we expect KKD’s same-store sales to decline on a two-year basis in FY15. We believe the stock has already sold off on these expectations. On the other hand, we expect franchise international same-store sales to continue its upward trend and ultimately approach positive territory. Despite potentially slowing same-store sales trends, we believe KKD has leverage left in its operating model. Specifically, we believe selling higher margin beverages continues to be one of KKD’s largest opportunities. Management is taking steps, including a partnership with GMCR to sell Krispy Kreme K-Cup packs, to drive top of mind awareness and, ultimately, in-store coffee purchases.

We are also intrigued with the strong financial profile of the company. KKD has compelling unit economics, free cash flow generation and is generating strong ROIIC. Despite its ambitious growth agenda, management has been willing to return capital to shareholders through its share buyback program. KKD has approximately $50mm remaining on the current $80mm authorization. Given the brand’s recent success, we believe the company is a strong takeout candidate.

We expect KKD to generate +20% EPS growth in FY15 and FY16 and believe the current share price represents an attractive entry point.

KKD is trading at 25.14x P/E and 15.30x EV/EBITDA on a NTM basis.

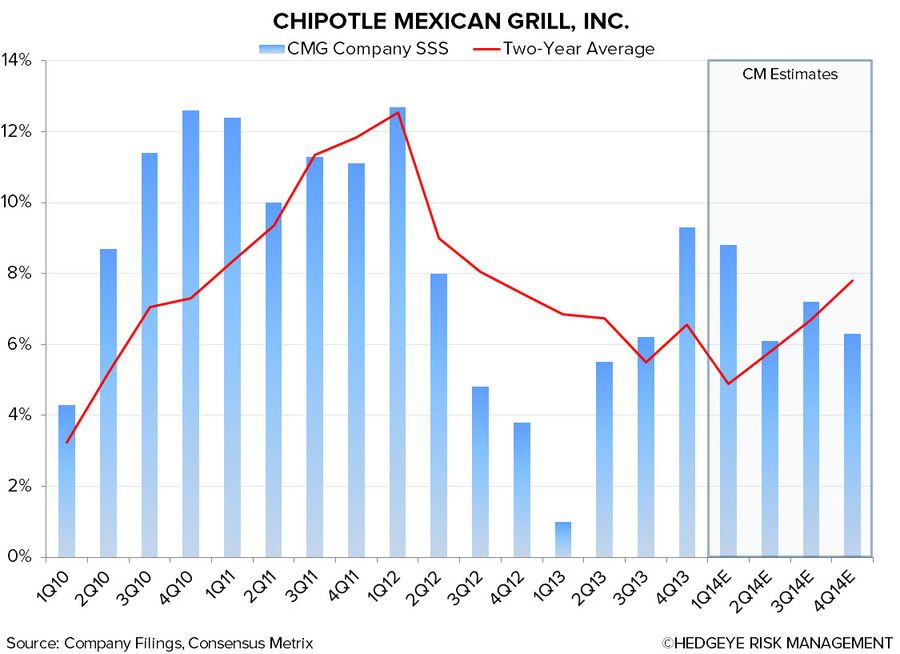

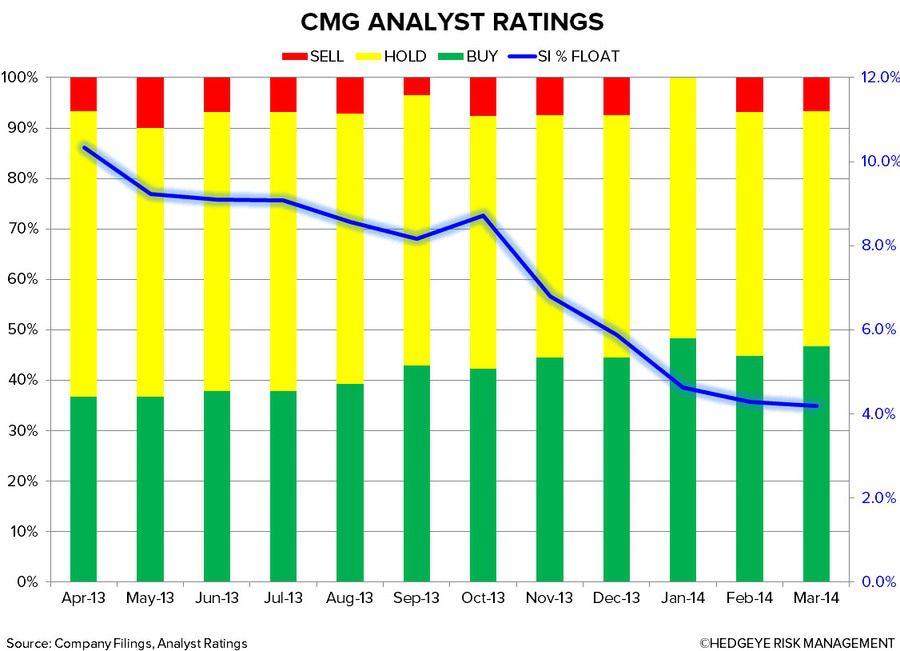

Chipotle Mexican Grill, Inc. (CMG)

Chipotle Mexican Grill, with its best in class operating model, has delivered strong returns for shareholders over the majority of the last five years. Despite more than doubling in 2013, we continue to favor the stock as strong same-store sales momentum (+9.3% in 4Q13) should continue through 1H14. Chipotle continues to differentiate itself and drive consumer loyalty with its unique food and people culture.

CMG has several drivers in place (faster throughput, Sofritas, catering, GMO removal, non-traditional marketing) to help capitalize on recent momentum and enable them to deliver +15% revenue growth and +20% EPS growth in FY14 and FY15. Chipotle, at 1,500 domestic units, has ample room left for domestic expansion and an international market that is virtually untapped. Longer-term, the Shop House and Pizzeria Locale concepts remain two potentially significant growth drivers.

On the 4Q13 earnings call, management discussed a potential 3-5% price increase beginning in 3Q14 in order to help offset rising food costs, including the transition to non-GMO ingredients by the end of FY14. Management guided to food costs as a percentage of sales to be around 34.5% for FY14 before the impact of any price increase. Assuming a modest price increase, the street is currently modeling food costs at 33.6% of sales for the full year.

Despite significant same-store sales and traffic momentum, we believe margin pressure is beginning to build on CMG’s cost lines. However, a price increase could help offset this and given the loyal customer base and premium placed on high quality food, we don’t expect this to be much of an issue.

CMG is trading at 41.77x P/E and 20.97x EV/EBITDA on a NTM basis.

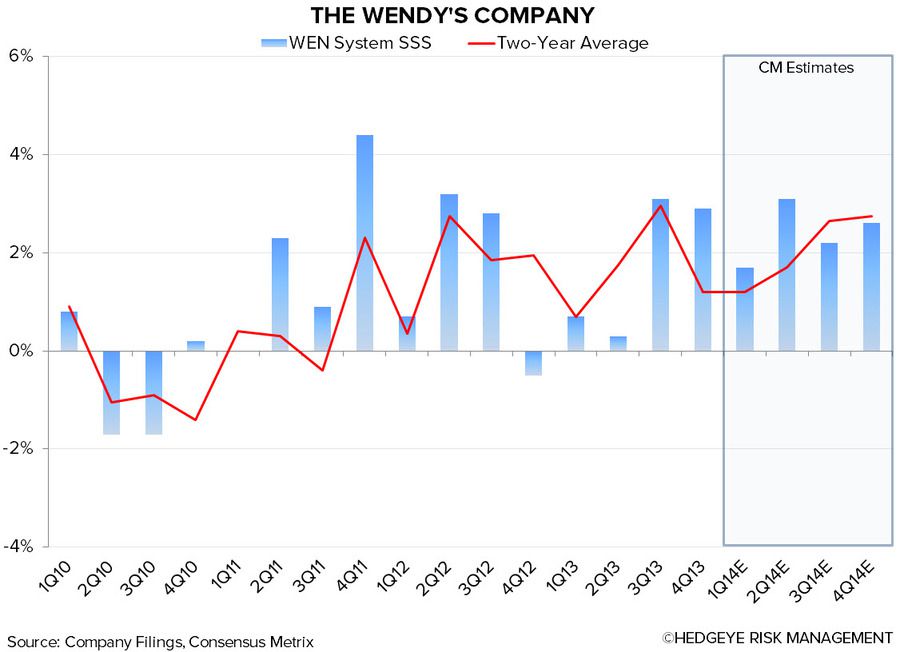

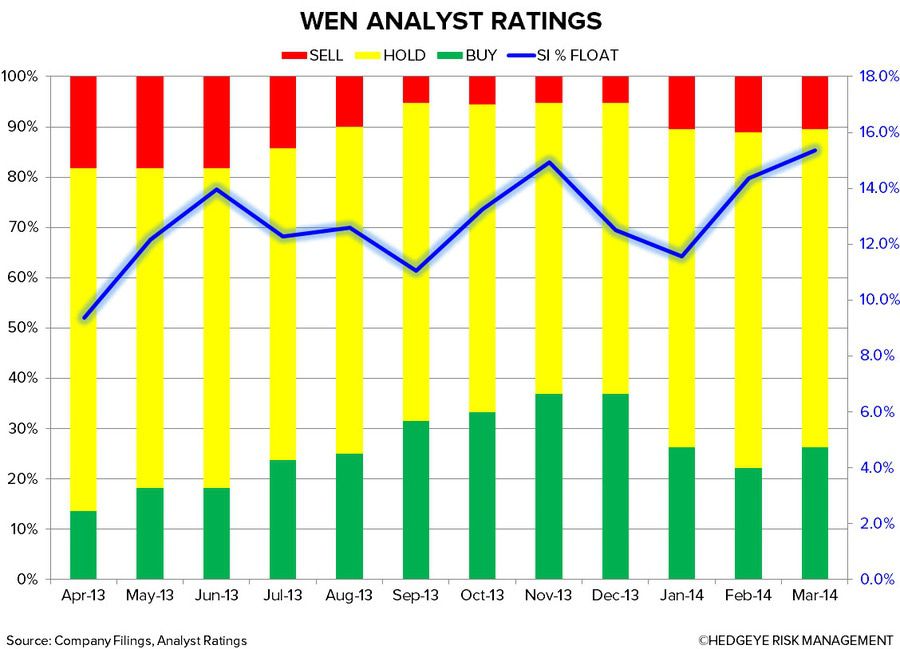

The Wendy’s Company (WEN)

WEN continues to take market share in the QSR space in large part due to its successful Brand Transformation, successful new products and ongoing store reimages. By repositioning the brand as “A Cut Above,” management has driven strong same-store sales momentum that should continue through FY14. Menu innovation has led to the creation of popular LTOs such as the Pretzel Pub Chicken Sandwich, the Pretzel Bacon Cheeseburger, and Bacon Portbella Melt on Brioche. Through this repositioning, WEN has established itself as a producer of high quality food at a reasonable price. In other words, they’ve found the middle ground between traditional QSRs and fast casual concepts.

In late March, Wendy’s rolled out a new mobile payment smartphone app to its entire domestic restaurant base. Not only is this a smart strategic move that fits with the brand’s repositioning, but it is a potential guest experience enhancer and transaction driver.

Same-store sales momentum and recent debt refinancing initiatives have aided cash flow generation, while WEN’s corporate optimization has helped management manage its effective tax rate. WEN already pays a respectable dividend, but management has been open to growing this and repurchasing shares when they have the cash.

We expect WEN to deliver +13% EPS growth over the next two years and continue to grow restaurant level and operating margins. WEN has high short interest (+15% of the float) and is generally disliked by the street, making it our favorite contrarian play on the long side in the restaurant space.

WEN is trading at 24.84 P/E and 10.22x EV/EBITDA on a NTM basis.

Yum! Brands, Inc. (YUM)

YUM continues to be one of our favorite longs in the big cap QSR landscape as we believe the company is well positioned to capitalize on a substantial long-term growth opportunity in China and other emerging markets. We expect easy comps, notable margin expansion and positive earnings momentum to drive performance throughout 2014. As we’ve stated before, the magnitude of this performance will depend heavily upon the trajectory of the recovery in China. While management’s guidance of 40% operating profit growth in China may be aggressive, we believe they have multiple levers at their disposal to reach at least +20% EPS growth in 2014.

We believe China concerns are overdone and the region is well on its way to recovery, despite somewhat limited visibility. YUM’s ongoing efforts through its I Commit campaign should help restore trust in the KFC brand, while a 2Q restaging and menu revamp should help establish considerable brand momentum. Furthermore, Pizza Hut casual dining and home business continue to be two strong growth opportunities. Despite near-term volatility in trends, China continues to be a significant opportunity for YUM to capitalize on a growing consumer class that is expected to double from 300mm+ in 2012 to 600mm+ by 2020.

Domestically, Taco Bell continues to take share from competitors and drive incremental sales through innovation. The chain recently launched its national breakfast rollout, supported by a strong advertising campaign. Early signs indicate that breakfast has been selling well and franchisees are supportive of the move. We believe breakfast represents a material opportunity for Taco Bell, even if they are only able to capture a small piece of the market. Taco Bell has significant brand momentum and continues to carry the domestic business. We expect to see a renewed focus at both the KFC and Pizza Hut brands as they continue to lose share to competitors.

YRI continues to be a material long-term growth opportunity as the company positions itself to capitalize on a rapidly expanding consumer class.

YUM is trading at 20.86x P/E and 11.68x EV/EBITDA on a NTM basis.

Howard Penney

Managing Director

Fred Masotta

Analyst