RECAP: YELP'S US TAM

During our Best Ideas Short Call, we broke down YELP's US Total Addressable Market TAM). The analysis was fairly simple. YELP's addressable market needs to fit two criteria:

- Retail (vs. B2B)

- Affordability

YELP has suggested that its US TAM is 27M. Our analysis of the US market, using the above criteria, suggested it is only 3.4M. We also explained why we don't believe YELP can ever penetrate more than 170K of that. For more detail, see link at end of note.

DISSECTING YELP'S EU TAM

We didn't touch upon YELP's international market during our Best Ideas Call because the headwinds in the US are too severe for international to compensate. However, we decided to extend our TAM analysis to the EU to prove this point.

CRITERIA 1: RETAIL

There are 21M non-financial establishments in the EU, however the majority (65%) cater to the B2B market (vs. Retail, which is YELP's core user). YELP's EU TAM (according to Criteria 1) is 7.4M, but that doesn't consider affordability

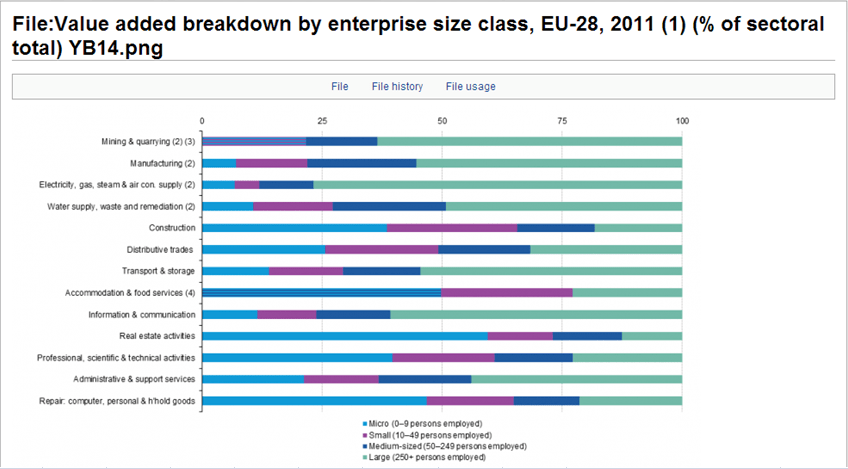

CRITERIA 2: AFFORDABILITY

This one is tougher to back into since we can't pull business segmentation by revenue/income bracket as we did with the US market. But we do have "Value Added" (essentially EU version of NOPAT) by firm size, which gives us a proxy for affordability.

Micro firms (less than 10 employees) represent over 94% of YELP's EU TAM, but represent a disproportionately smaller portion of Value Added. While we can't segment YELP's EU TAM with the same granularity as we did with the US market, we broke it down by average Value Added (think NOPAT) across the Micro firms in the Yelp's applicable markets.

The data suggests that average firm in YELP's EU TAM produces Value Added of $77K. In turn, the cost of Yelp Advertising would be prohibitive at YELP's average ARPU (YELP suggests its typical local ad spend is $4.2K year). It's important to note that these are averages, so YELP should be able to gain some penetration among the above-average Micro firms. The question is how much?

CONCLUSION

In summary, the data suggests YELP's Total Addressable EU market (7.3M) is much smaller than many expect, and given that 94% of this market is composed of micro firms producing less than $77K of Value Added on average, we suspect the road to penetrating this market will be challenging.

We provide more detail on our short thesis in the note below, and far more detail in our YELP Short Best Ideas Slide Deck. For a copy, or to discuss our thesis in more detail, let us know.

YELP: Death of a Business Model

04/04/14 10:05 AM EDT

http://app.hedgeye.com/feed_items/34518

Hesham Shaaban, CFA

@HedgeyeInternet