Overall, we expect this earnings season will be lackluster for the banking sector. Outside of some modest acceleration in loan growth and ongoing credit tailwinds from an improving labor market and inflating collateral values, there will be little good news for management to discuss. Margins are likely to be flat sequentially, while credit tailwinds, vis-a-vis provision expense/reserve release, will show more pronounced signs of fading. Offsets will be expense reduction initiatives, though these have now been ongoing for some time, and falling sharecount from active repurchase programs. Another offset may be relatively upbeat guidance with respect to a reduction in future costs, both legal and operational, relating to legacy mortgage troubles. We think 1Q results are likely to set expectations fairly low for the duration of 2014.

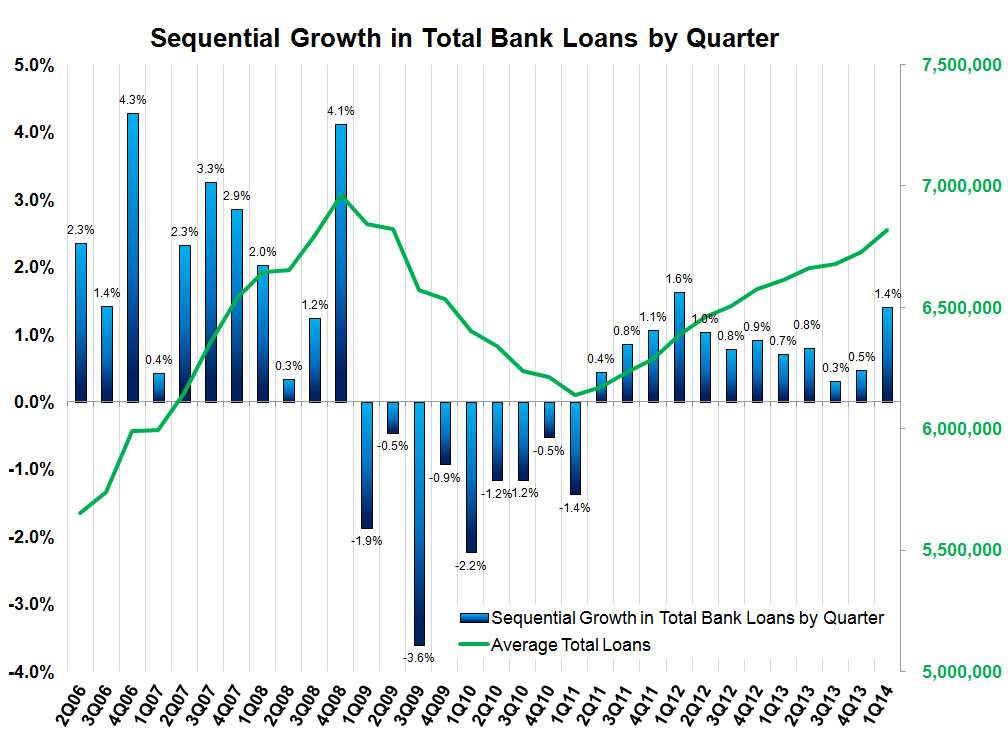

- Loan Growth - Status Quo - Overall, loans grew by 1.4% QoQ in 1Q14, which was up vs 0.5% QoQ growth in 4Q13.

- Margins Likely Unch'd - 1Q14 saw essentially no change in the average yield spread QoQ. Banks have pulled most of their available levers at the short end of the curve, but the pressure on earning asset yields has abated somewhat for now.

- Credit - Fading Tailwinds - Credit quality is still improving (lower DQs & NCOs), but provision expenses are actually beginning to rise as reserve release shrinks. The modest uptick in loan growth will add modestly to the pressure here to grow provision expense.

1Q14 Revenue: Better Loan Growth, Flat Margins and Non-Interest Income Pressure.

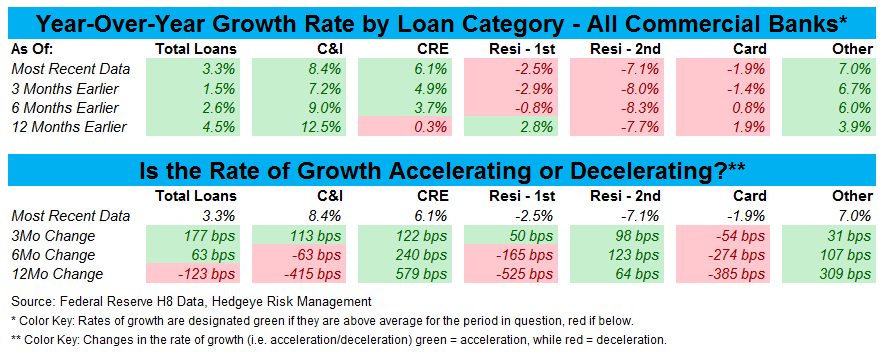

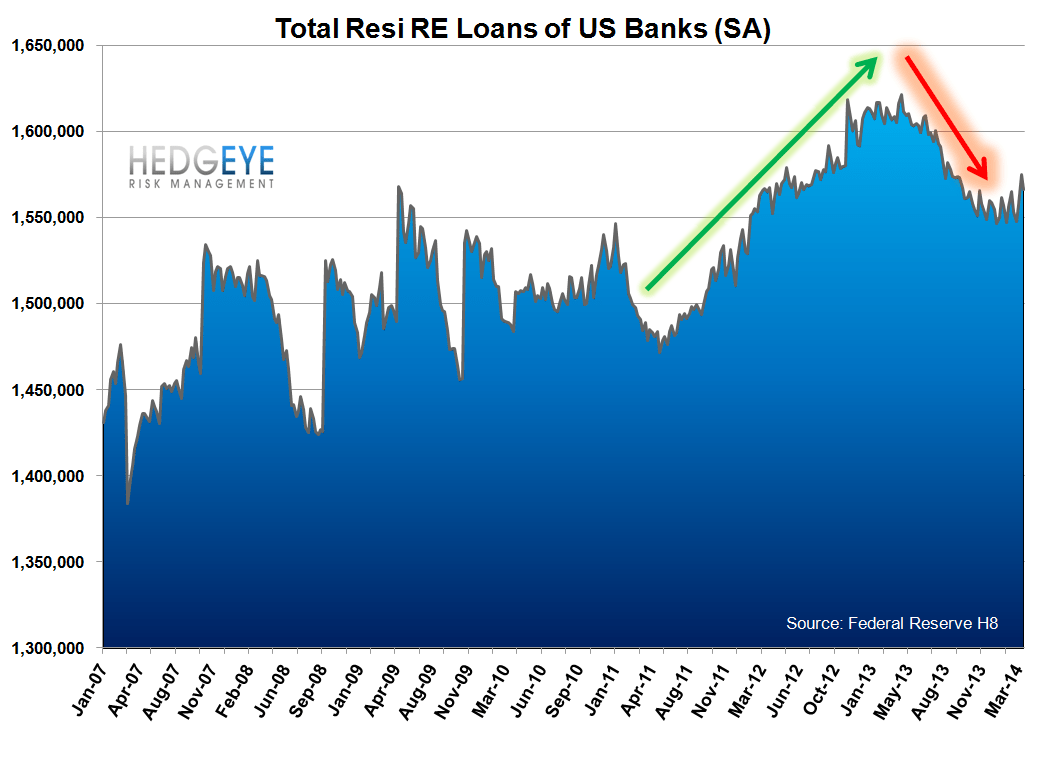

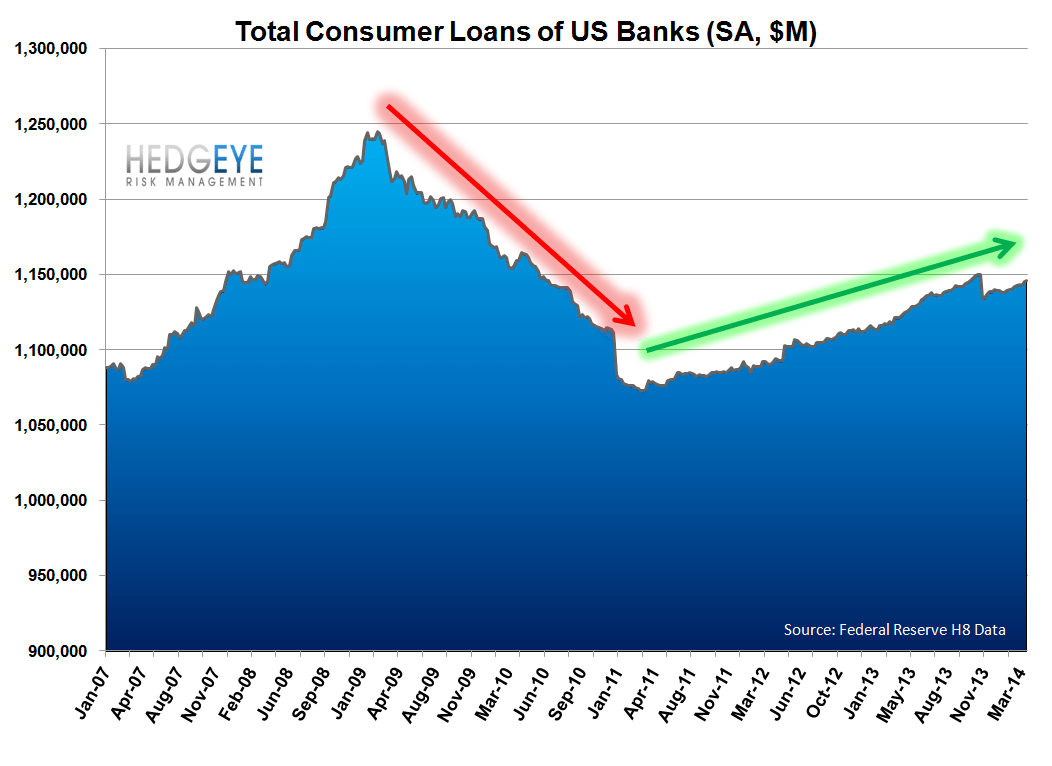

* Loan Growth - Total domestically-chartered commercial bank loan growth grew 1.4% QoQ, which was roughly triple the QoQ growth in 4Q13 (+0.5%), based on the Fed's H8 data through March 26, 2014 (the most recent available). This is an important inflection as the preceding 7 quarters were showing pretty consistent sequential deceleration in loan growth. It remains to be seen whether 1Q14 is the start of an upturn or a false dawn, but it's deviation vs recent trend is definitely noteworthy. Loan growth is now running at +3.3% year-over-year, which is up from +1.5% y/y just three months ago.

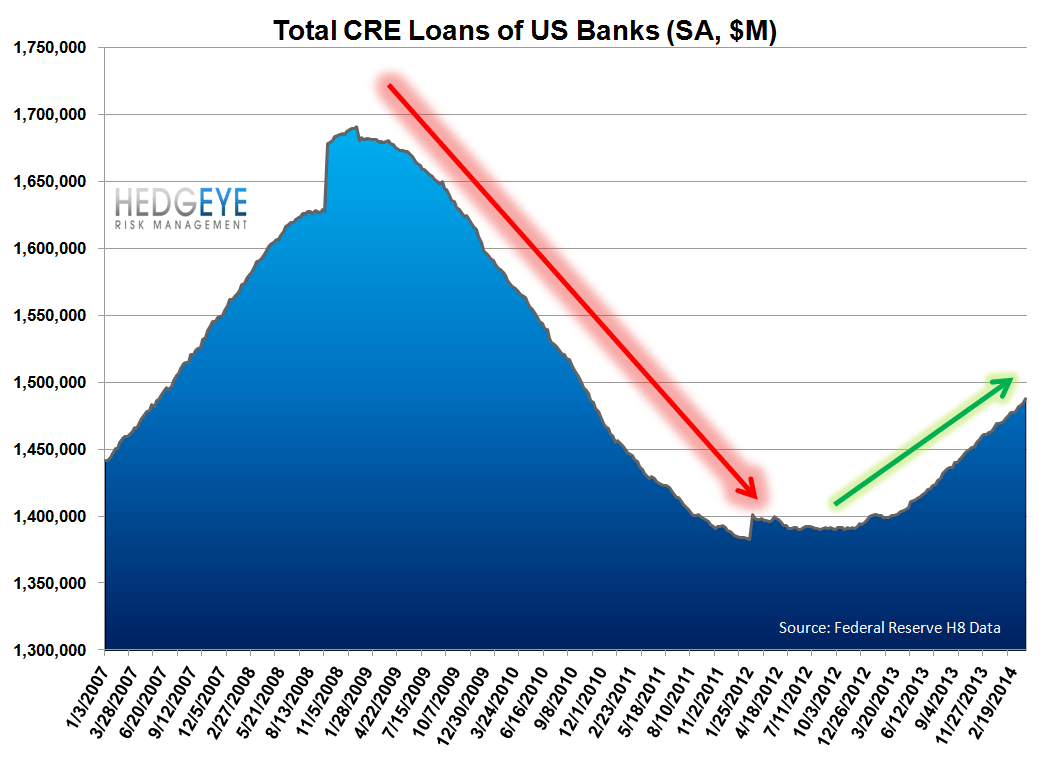

The strongest categories of loan growth remain C&I (+8.4% y/y) and "Other" (+7.0%), which is powered primarily by auto loans. CRE lending is where we're seeing the fastest acceleration in growth. CRE loan balances are up 6.4% y/y, but have accelerated +579 bps over the past 12 months and +122 bps over the past three months.

The chart below shows the year-over-year growth rate of loans by category at a slightly more granular level.

Taking a step back, the recent positive inflection in loan growth has helped the trend get almost back to trendline. The chart below shows loan growth back to 2002 and breaks it into three distinct periods. The CAGR since Feb 2011 - the most recent inflection - has been +4.4%.

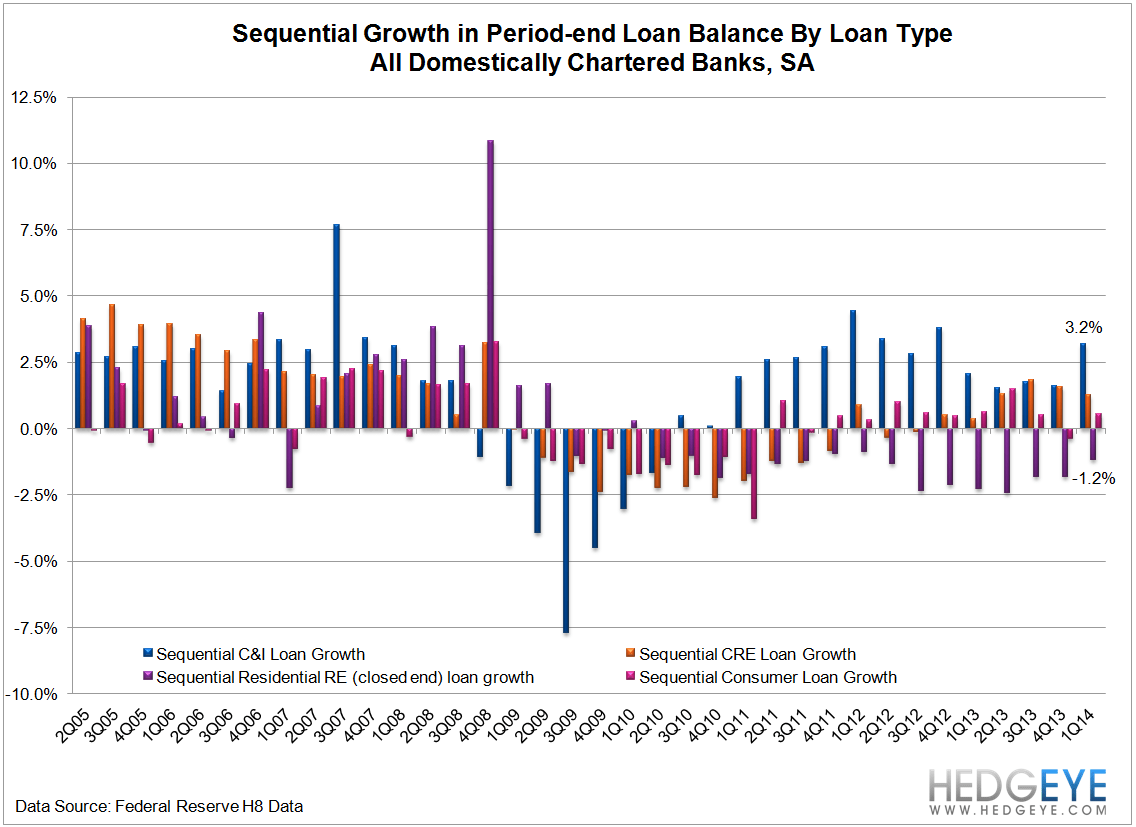

Here's a more detailed look at each loan category vis-a-vis growth.

* NIM - Net interest margin trends should be uneventful this quarter as the average 2-10 yield spread in 1Q14 was 239 bps vs 241 bps in 4Q13. The same is true for the long end of the curve, where the average yield on the 10-year treasury was similarly lower by a few basis points quarter-over-quarter.

* Non-Interest Income - Mortgage banking is one of the primary drivers of Q/Q change in non-interest income, and the news here isn't great. Total application volume in 1Q14 was down 12% QoQ, though primary/secondary spreads were relatively unchanged at 93 bps in 1Q14 (avg) vs 91 bps in 4Q13. Taken together, this implies sequential declines of roughly 10% in production revenue. There is unlikely to be any offset to this from the servicing side as rates ended the quarter flat to down with where they started (4.42% on 30YR FRM at 3/31/14 vs 4.54% at 12/31/13). Meanwhile, spreads have not widened since the end of the quarter.

1Q14 Credit Tailwinds: Slack Sails

* Credit quality continues to improve, but at a decelerating rate. Take a look at the chart below showing the sequential change in NCOs for the money center banks and large card operators. The point is that losses have been steadily converging towards a steady state for the last four years and appear to have reached their nadir as evidenced by the last two data points, which average roughly zero.

Meanwhile, on the other side of this, provision expense is beginning to rise. Expectations are that 1Q14 provision expense for the 7 firms shown in the chart above will rise to $4.2 billion from $3.3 billion in 4Q13. That would be the first rise since the beginning of the credit cycle recovery. NCOs are still outpacing provisions by $2.0-2.5 billion for these firms, but that's down sharply from almost $5 billion in reserve release just a few quarters ago.

In the chart below we show the sequential change in allowance in the H8 data for Large Banks (blue) and the actual total for the large caps above (in red). The current quarter reflects the atual H8 data and the consensus estimates for reserve release in 1Q14.

The chart below shows the sequential change in total allowance across all domestically chartered commercial banks.

* The only good news on the credit front is that the labor market continues to improve, as evident from the recent claims data, JOLTS data and ongoing, steady-as-she-goes ADP numbers. Moreover, collateral values have continued to inflate at a rapid clip, namely residential and commercial properties, in the first quarter of this year. While the tailwind of reserve release will definitely slow, it's at least some comfort that the fundamental measures of credit quality are still improving.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA