Takeaway From McGough:

Just look at the SIGMA trajectory for both retailers: sales down, inventories up, weak margins. But how come that is in such stark contrast to what we saw out of Restoration Hardware (RH) and Williams & Sonoma (WSM)? Aside from better product, merchandising, and marketing, there's a structural factor as well. Bed Bath & Beyond generates only 4% of its sales online. Pier 1 Imports is only at 5%. That means when people don't want to leave their homes due to weather, sheer laziness, or whatever, these two companies are at a competitive disadvantage. RH and WSM, however, generate nearly half of their respective sales online. They both have the ultimate channel hedge to complement their premium product offering. This quarter it made a difference.

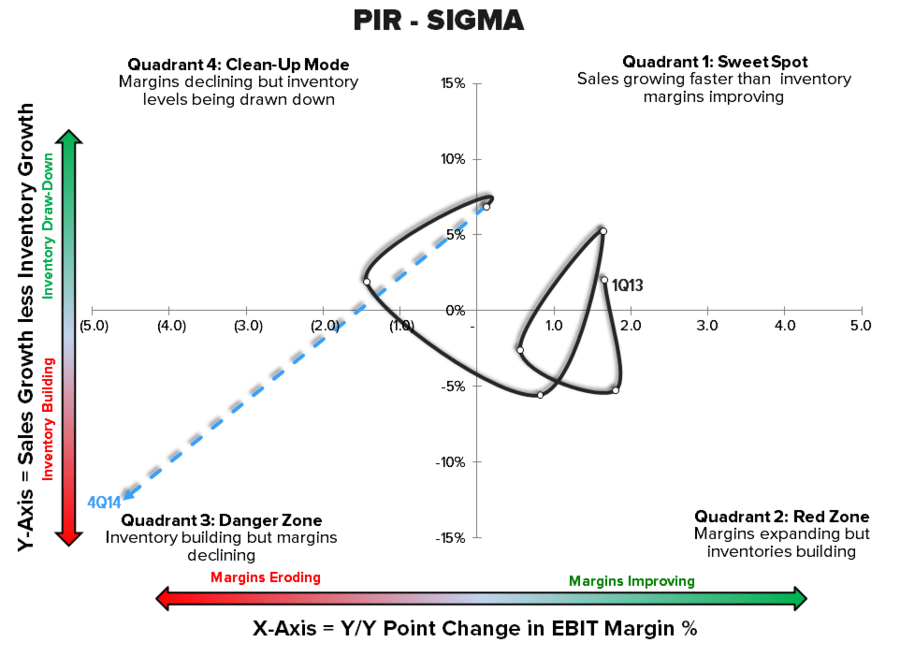

Bed Bath & Beyond may have printed earnings that are in line with prior guidance, but any way we slice it, this SIGMA trajectory looks horrendous. A 6% sales decline on a 5% inventory build is was out of character for Bed Bath & Beyond.

But, as bad as Bed Bath & Beyond looks, Pier 1 looks even worse. Not enough sales, way too much inventory, and no margin to be found. It’s ugly.

Editor's Note: This is a complimentary research excerpt from Hedgeye Retail Sector Head Brian McGough. Follow McGough on Twitter @HedgeyeRetail.