No inflation for four years.

That’s what this Keynesian character from the Minnesota Fed (Narayana Kocherlakota) said earlier this week. I couldn’t make this up if I tried, but here’s his explanation:

"The low inflation in the United States tells us that resources are being wasted...I’ve said that the FOMC is undershooting its price stability objective and is expected to continue to do so. But we should all keep in mind that this outcome—and especially the forecast for continued undershooting—typically means that the FOMC is also underperforming on its other objective of promoting maximum employment."

In related news, our Q2 Macro Themes released to subscribers on Tuesday has the exact opposite view. Ping sales@hedgeye.com for more info.

Someone is smoking something here, and since I don’t do drugs, I don’t think it’s me. This guy is cheering on the very thing that is slowing real growth (#InflationAccelerating).

Simple equation: Fed Minutes = Burn The Buck --> Commodity Inflation rips.

Take a look around this morning:

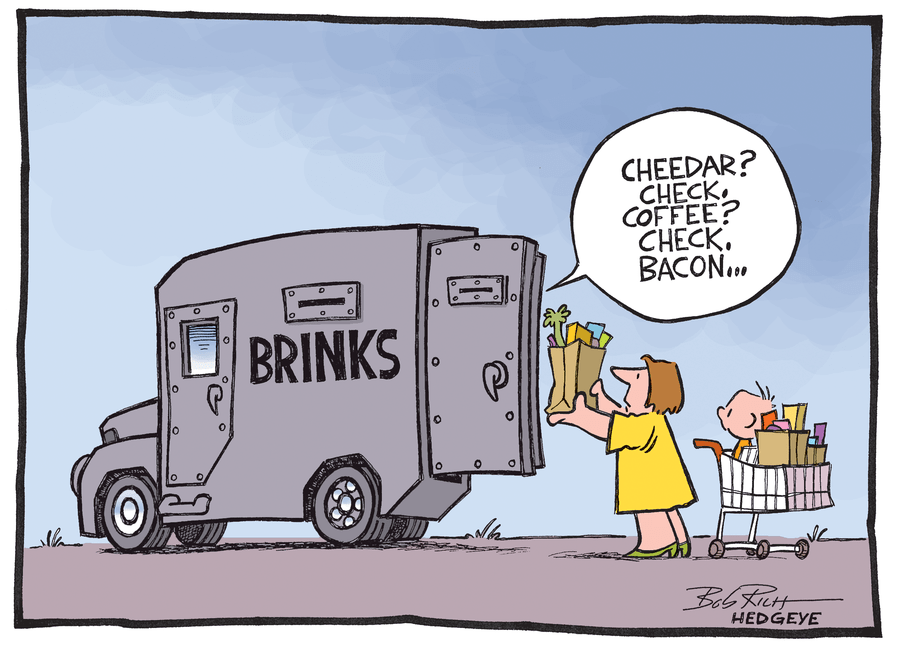

- COMMODITIES: freshly squeezed YTD highs in commodity #InflationAccelerating (CRB Index +10.7% YTD)

- COFFEE prices up 68% YTD

- BEEF prices hit all-time record high in US

- GOLD: ramps the whiners another new one (back to +10% YTD); Silver (which we're long in #RTA too) +2.5% this morning too

Your un-elected Fed says food prices are "non-core" to American life. Try telling that to average Americans in the grocery store. In other words, there is no inflation. Just ask one of these unelected and unaccountable government guys smoking Keynesian crack.