TODAY’S S&P 500 SET-UP – April 8, 2014

As we look at today's setup for the S&P 500, the range is 37 points or 0.82% downside to 1830 and 1.19% upside to 1867.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.30 from 2.31

- VIX closed at 15.57 1 day percent change of 11.53%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Business, March, est. 92.5 (prior 91.4)

- 7:45am ICSC weekly sales

- 8:55am: Redbook weekly sales

- 9am: IMF releases biannual world economic outlook

- 10am: JOLTs Job Openings, Feb., est. 4.020m (prior 3.974m)

- 1:30pm: Fed’s Kocherlakota speaks in Rochester, Minn.

- 2:45pm: Fed’s Plosser speaks in Philadelphia

- 4pm: Fed holds open board mtg in Washington on leverage ratios

- 4pm: Fed’s Evans speaks in Washington

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- 10am: House Ways & Means hearing on supporting economic growth through “a Fairer Tax Code”

- 10am: House Armed Services Cmte hearing on Russia’s military developments, implications

- 10am: Atty Gen. Holder testifies on Justice Dept. at House Judiciary Cmte

- 10am: PPP hearing at House Transp. and Infrastructure Cmte

- Senate leaders hold news conferences after party luncheons

- FY15 budget panels/hearings:

- 9:30am: NASA Admin. Charles Bolden, House Appropriations

- 9:30am: Gen. Raymond Odierno, National Guard Bureau Chief Gen. Frank Grass, Army Reserve Chief Gen. Jeffrey Talley, Senate Armed Services Cmte

- 10am: Secretary of State John Kerry, Senate Foreign Relations

- 10:30am:Education Sec. Arne Duncan, House Appropriations

- 2pm: GSA Admin Dan Tangherlini, House Appropriations

- 2:30pm: Senate Judiciary marks up patent troll bill S. 1720

WHAT TO WATCH:

- Takeda, Lilly jury awards $9b over hiding Actos risks

- Citigroup agrees to $1.13b settlement over mortgage bonds

- Koch said to near deal for CVC’s Flint Group with Goldman Sachs

- Fed holds open board meeting in Washington on leverage ratios

- GM SUVs get top marks in insurance-industry front crash test

- U.S. Court of Appeals hears Apple/Google patent arguments

- Long-term jobless benefits stalled even with Senate passage

- China approves Microsoft, Nokia deal with conditions

- Express Scripts threatens to blackball Gilead’s Sovaldi

- Barclays settles U.K. Libor case weeks before trial to start

- BOJ refrains from boosting stimulus as recovery seen

- U.K. industrial output rises more than forecast on factories

- Weekly release of FDA warning letters

- IMAX to sell 20% stake in China business for $80m: WSJ

EARNINGS:

- Alcoa (AA) 4:03pm, $0.05 - Preview

- International Speedway (ISCA) 7:30am, $0.34

- Science Applications Intl (SAIC) 4:01pm, $0.65

- WD-40 Co (WDFC) 4pm, $0.68

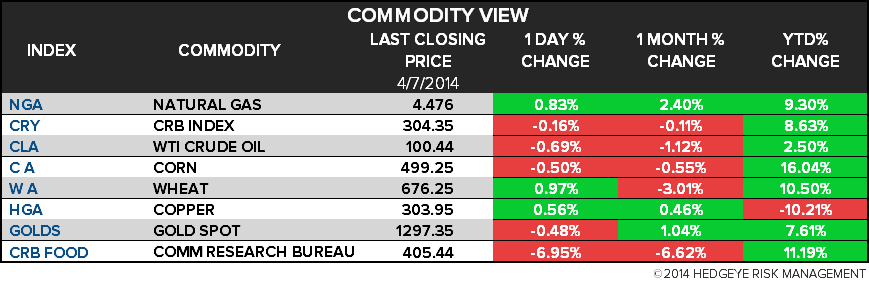

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Climbs to Two-Week High as Dollar to Ukraine Spur Demand

- EU Pig Farmers Miss Out on Boom as Russian Ban Spurs WTO Case

- WTI Rebounds as Gasoline Stockpiles Seen Shrinking; Brent Gains

- China Corn Glut No Barrier to Farmers as State Buys: Commodities

- Copper Falls 0.4% to $6,648 a Ton in London; Nickel, Tin Drop

- Coffee Extends Gains in London as Arabica Climbs for 4th Day

- Soybeans Snap Two-Day Drop as USDA May Report Reduced Stockpiles

- Rebar in Shanghai Climbs to One-Month High as Stockpiles Decline

- U.S. Beef to Japan May Decline on Australia Deal, Ministry Says

- Age of Gas Seen as Sideshow to U.S. Producers Preoccupied by Oil

- Copper Producers Keep Faith in China as Rout Belies Demand

- Gold’s Open-Interest Drop Signals Rally Ending: Chart of the Day

- Ending Iran Oil Ban May Cut Refiners’ Supply Cost: Bull Case

- Turkey’s Fracking Push Won’t Be Stalled by Bribery Probe: Energy

CURRENCIES

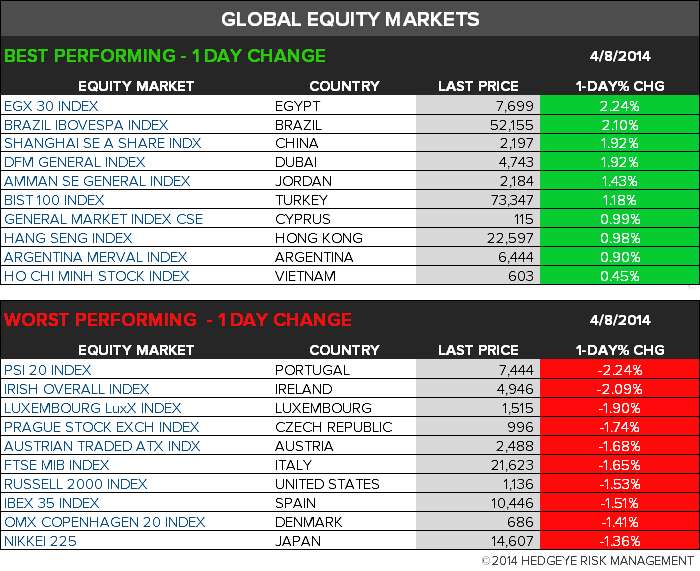

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team