The large capacity increase in Q2 for the Caribbean is clearly impacting pricing

OVERALL SURVEY SENTIMENT

- RCL: Neutral

- NCLH: Negative

- CCL: Not applicable

CALL TO ACTION

RCL continues to be a mixed bag with strong pricing power in Europe but weakness in the Caribbean. NCLH’s high exposure to the Caribbean will pressure company yields particularly in 1H 2014.

SUMMARY

Our most recent pricing survey focused on RCL and NCLH, since CCL just reported earnings last week. While overly conservative in our opinion, CCL’s guidance was certainly disappointing. RCL's pricing power resides in Europe and pricing in the region strengthened even further in March. However, RCL is not immune to the weakness in Caribbean pricing, particularly for FQ2. For NCLH, its FQ2 Caribbean pricing continued to slip in March. We estimate NCLH has approximately 83% and 46% exposure to the Caribbean in FQ1 and FQ2, respectively.

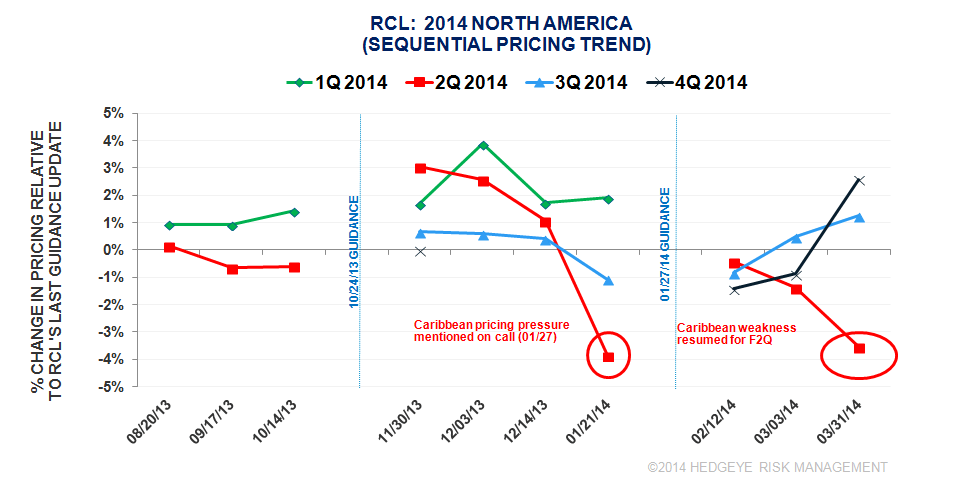

RCL

- Caribbean

- Glaring tumble in FQ2 pricing as seen in Chart 1

- Celebrity pricing fell off a cliff for FQ2. Thankfully, it only accounts for 9% of RCL’s Caribbean itineraries.

- For the RC brand, pricing for late April/early May itineraries was hit hard across the fleet.

- Starting with June, pricing in the Caribbean looks pretty healthy

- Quantum pricing for Nov/Dec remain unchanged

- Anthem pricing for 2015 remain unchanged

- Pullmantur pricing steady

Chart 1

- Europe

- Chart 2 shows strong YoY pricing for all quarters. In Chart 3, on a sequential basis, there was a price drop in FQ2 but that is more than offset by gains in FQ3 and FQ4.

- RC brand – pricing up high double-digits for F2Q and high single/low double digits YoY for F3Q-F4Q

- Celebrity pricing making strides. Sequential positive momentum continued at the end of March.

- Azamara pricing was mixed

- Pullmantur pricing showed good growth considering very easy comps

- Alaska

- Both RC brand and Celebrity improved slightly on sequential pricing. YoY, pricing remains down modestly.

Chart 2

Chart 3

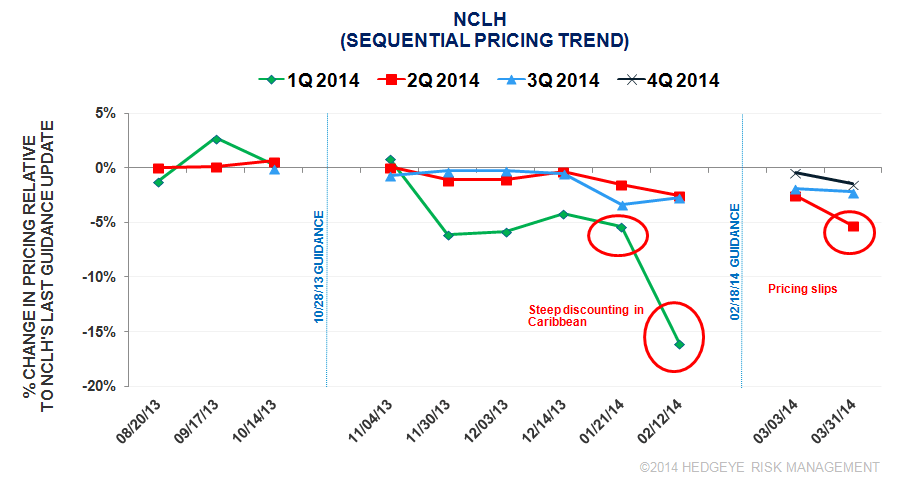

NCLH

Chart 4 shows overall, NCL pricing fell slightly at the end of March.

- Caribbean

- Discounting didn’t stop as March progressed. We’re particularly worried about FQ2.

- Getaway’s 2Q pricing maintains a healthy premium over its existing fleet but it’s misleading because its comp brands (Sun, Pearl, Sky, Epic) pricing fell again, -8% on average since early March and -27% since February guidance while Getaway pricing declined 18% since February. Getaway premiums for 4Q was steady around 28%. Compared with Epic, its 6% higher.

- Breakaway 3Q premium remain in the low single digits for F3Q and +26% for 4Q.

- Alaska

- Pricing was relatively stable. YoY, pricing remains modestly lower.

- NCLH has 10% and 19% exposure to Alaska in FQ2 and FQ3.

- Europe pricing looks outstanding for the summer

- Hawaii summer pricing took a hit in FQ2

Chart 4

STOCK VS SURVEY

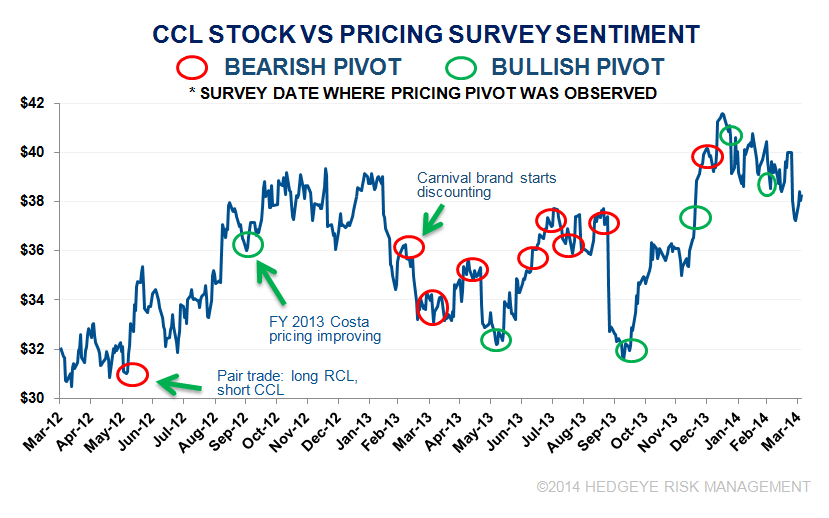

CCL

Survey has been mostly bullish for Carnival since the major pivot from the 10/14/13 survey.

RCL

Survey has suggested mixed signals for RCL in the past 6 months

NCLH

Survey has been bearish on NCLH since the 02/12/14 survey