Below are Hedgeye analysts' latest updates on our TEN current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We also feature three research notes from earlier this week which offer valuable insight into the market and economy.

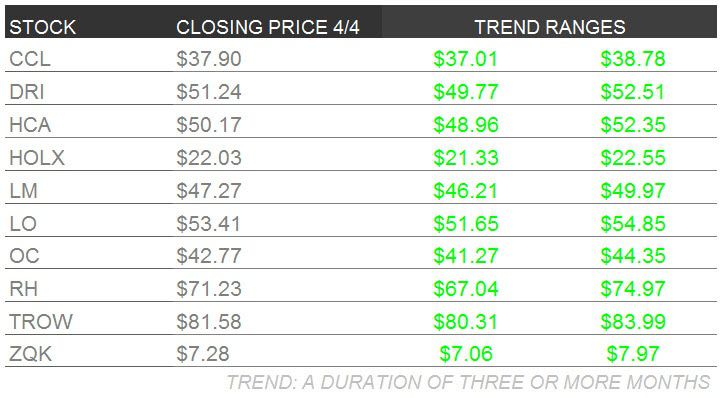

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

CCL – Carnival traded up almost 2% this week while the S&P 500 Index was up 0.4%. Last week’s headlines focused on the health of the U.S. consumer and whether or not the U.S. economy is expanding sufficiently to create new jobs – which leads to improved consumer sentiment and increased consumer spending, two trends which favor the cruise industry.

European news was again positive, the European Central Bank indicated it would be open to further policy easing, supporting optimism regarding improving European economies and stronger European consumer spending. As we indicated last week following Carnival’s earnings call, our full-year fiscal earnings estimates remain above management’s guidance because we believe Carnival recent pricing power continues and will ultimately translate into better than expected revenues and earnings. We affirm out positive outlook on Carnival Cruise Lines.

DRI – Starboard Value released an investor presentation, detailing its analysis of Darden management and the proposed Red Lobster spin-off. Starboard believes Darden’s real estate portfolio is worth approximately $4 billion and that separating Red Lobster and its real estate from Darden’s portfolio would destroy approximately $850 million in value. The presentation was deservedly critical of Darden’s current management team and is a must-read for interested parties. We highlighted what we believe are the key takeaways from the 100+ page deck in a note to subscribers and an exclusive HedgeyeTV video.

Darden responded to the public scrutiny by releasing a statement reiterating their confidence in the initiatives they have in place. Hedgeye Managing Director Howard Penney continues to believe Darden represents a generational opportunity, but he needs to see the activists succeed in order for this thesis to materialize.

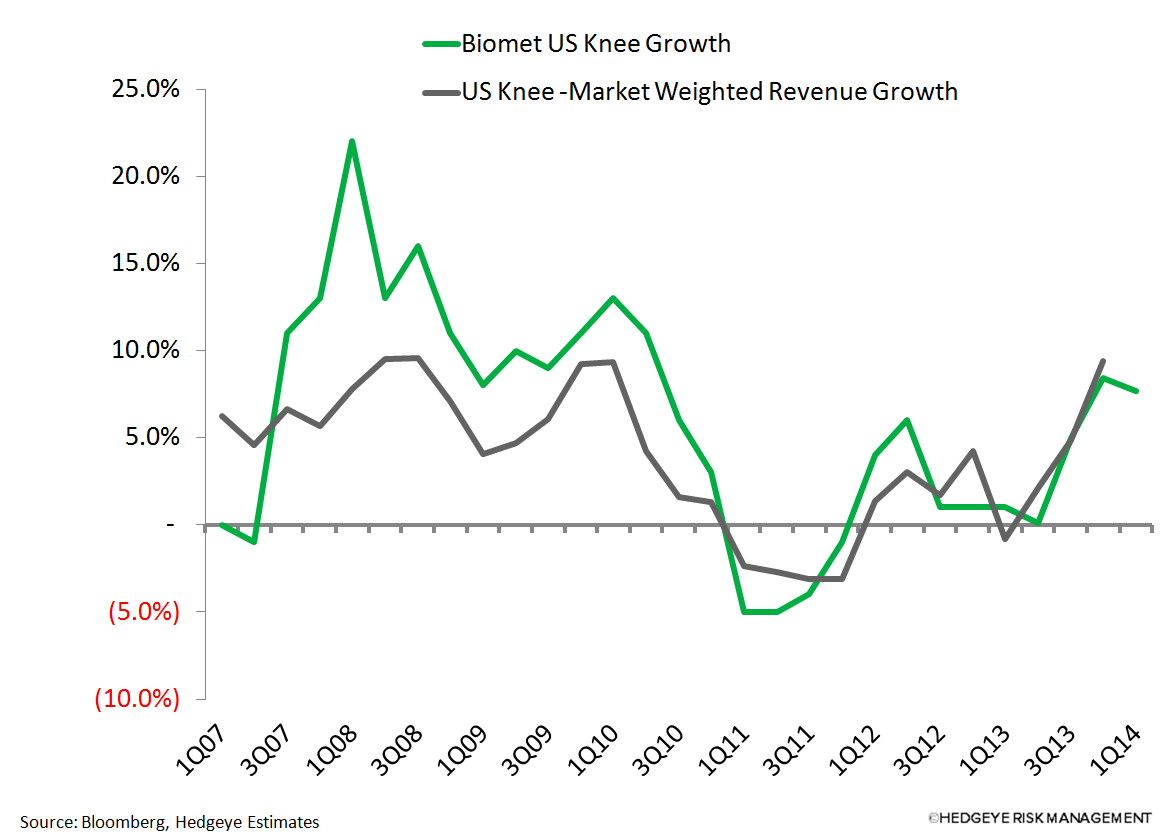

HCA – Sector Head Tom Tobin remains bullish on shares of HCA which have risen almost 25% since he added it to Investing Ideas back in June. Tobin wrote a research note on Biomet on Friday morning which is instructive as it relates to HCA. Bottom line? Biomet putting up numbers like it did is good news for HCA. Most people don't expect it.

HOLX – We received the March/April data for our physician survey. There were no big surprises, which is good. Patient volume at OB/GYN offices (Hologic focus) appears positive across several groupings, including region, payer class, and income. On the Thinprep side, a key growth headwind, the update was as expected as well.

On the positive side, we are noticing a common thread among the unsolicited comments from our surveyed physicians. Thinprep is slowing because the most recent guidelines (Cervical Cancer Screening Guidelines 2012) suggest increasing the time between testing patients who have a normal result by as much as 3 to 5 years. But as with all guidelines, and medical data in general, what looks good for the population as a whole, may not be good for the individual. Physicians are expressing a significant amount of concern about the possibility of missing cancers and women getting gravely ill. You can read some of the comments below.

LM – Our thesis on Legg Mason is an intermediate to longer term one with numerous positive catalysts into the back half of this year and into 2015. We think patient shareholders can be rewarded in numerous different ways including a management team that is now back on the deal making path with the recent placement of long term debt; that the company has a tailwind in pensions de-risking away from equities and into fixed income and alternatives; and that on a cash flow basis Legg has the highest free cash flow generation in the group which will enable shareholders to benefit from incremental dividends and buybacks.

Legg stock is off to a fast start this year up 9% versus BlackRock down 2%, Franklin Resources which is down 7%, and Janus which is down 12%. In the current range bound equity market, we would continue to add to LM shares on sharp market sell offs and position for positive catalysts over the next 6-12 months.

LO – Tobacco stocks took a slight hit this week on news that the British government may be moving toward instituting a tobacco plain packaging law by 2015. The UK would join Australia, the only other country that mandates plain packaging.

Lorillard does not have exposure in the UK, so we think the pullback in the stock creates a buying opportunity. Broadly, we believe that despite best efforts of a government to reduce smoking rates through plain packaging, studies have shown that such measures can have harmful consequences by boosting illicit trade.

We continue to believe LO will grind higher on advantaged menthol fundamentals, limited regulatory risk, and a growth engine in blu e-cigarettes.

OC – Owens Corning Q1 2014 earnings call is set for Wednesday April 23 at 11 a.m. EST. Beating or missing estimates for Q1 will not change our bullish stance on Owens Corning. This is a cyclical name in a cyclical industry. The cycle is just beginning to show signs of a construction rebound.

Incidentally, on Friday morning Reuters noted a pickup in housing activity, a positive sign for Owens Corning, who has products in both the commercial and residential space. Non-residential construction lags ~6 to 9 months behind residential construction (graphed below) shows a sharp inflection point, impressive considering the weather impact. Do not be surprised if construction activity this season picks up quickly to make up for a terrible winter, adding a further tailwind to our bullish case.

RH – Below are a few key takeaways from Restoration Hardware’s 4Q print and conference call from last week.

- We need to address the hiring of Doug Diemoz as the Chief Development Officer. While we’ve never quite heard of that title before, that doesn’t mean that it can’t be effective for Restoration Hardware. As focused as CEO Gary Friedman is in steering the ship, the reality is that there are a lot of areas for growth where Gary simply does not have the bandwidth to pursue. Now he’ll have someone who reports directly to him that can explore these opportunities. And of course, Diemoz is part of the Williams-Sonoma alum club – along with Gary, Richard Harvey (Kitchens), and COO Ken Dunaj (we’d put CFO Karen Boone in there too from her Deloitte audit days).

- ‘Always Innovating’ One thing we particularly liked was when Gary noted that people who are going to nitpick over timing of costs and revenue by quarter will perennially be disappointed with Restoration Hardware because “we will always be innovating.” There are other companies that have that same mindset – such as Nike and Ralph Lauren. Both have a dominant founder/leader who sets the tone inside the organization, and both have never been afraid to invest in the business even when it was not popular at the time by Wall Street. Both companies have emerged as superb stewards of capital over time. Restoration Hardware has the exact same feel to us as those other companies.

- Holiday: One thing that we underappreciated in the quarter was the company’s reliance on Holiday. It’s markedly less than Williams-Sonoma, but some of the weakness on the top line was driven by the company’s gifting categories. Those weaknesses were attributed to a medley of weather and self-inflicted wounds the latter of which was focused on the company’s decision to send Holiday Source Books to only 20%-30% of its mailing list. The source book strategy in total is still a work in progress (more on that below), but what strikes us is how data dependent the company is. There are still some wrinkles to iron out in the system, but the company is working through different strategies in order to maximize return on ad dollar spend.

- Source Book Strategy: This spring’s 3,200 page Source Book is exactly 2 times what it shipped last spring. The raw page count seems excessive, but it makes sense when you consider the breadth of the company’s product assortment in 2014. Add to the existing categories RH Rugs, RH Leather, and one unknown and you have the real core of RH’s product offerings – the one exception being Kitchens which isn’t scheduled for rollout until 2015. We estimated that the company saved about $40 million by eliminating the Fall Source Book. Some of those costs will be transferred to the spring book, but when you consider cost savings from production and shipping, net-net the company is coming out ahead on this one. The reality is that the company won’t be mailing out the full assortment to all of its customers. When you look at the numbers from 2013, customers received about 40% of the assortment. That number will probably be even less as the company tries to leverage the shopper data it has collected over the past few years to target specific consumers with specific assortments. On top of all that you have UPS delivering the mailers this year which may increase shipping costs, but will ensure a targeted and on-time roll out of the books in 2014, with better data for the company to analyze.

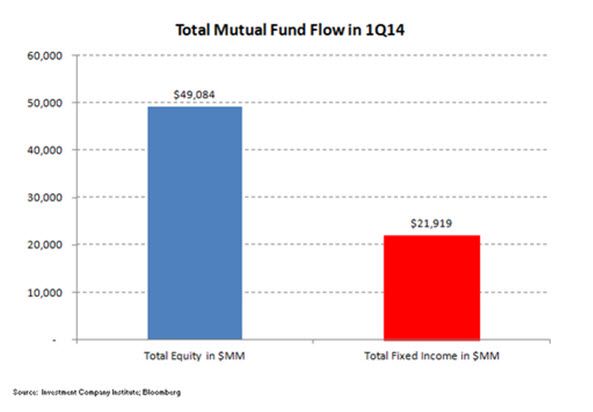

TROW – With the first quarter of the 2014 in the books, the running total of equity and fixed income funds continues to favor the stock side of the ledger. Total equity mutual fund flow (domestic and international) amounted to $49 billion quarter-to-date, over double the $21 billion that has come into all bond funds (taxable and tax free products), so despite the short term momentum in bond funds, the equity category is still better for now. These quarterly totals continue to support our long recommendation in shares of T Rowe Price (TROW), which we estimate will have the best results in the upcoming earnings season over the next few weeks.

ZQK – On Tuesday 23-year Quiksilver endorsee, Kelly Slater, announced that he was leaving ZQK to join the French conglomerate Kering, who owns action sports brands Volcom and Electric as well as the luxury Gucci label. Usually these types of announcements don’t cross our radar, but Kelly Slater is to Quiksilver what Michael Jordan is to NKE. The key difference is that Jordan has transcended his sport and become a $1 billion-plus commercial brand that is bigger than the entire Quiksilver brand.

ZQK tried to directly commercialize Slater through a new product line called VSTR in 2012. The brand was discontinued in 2013 along with a number of other brand extensions soon after CEO Andy Mooney took the helm in 2013. Due to the company’s brand rationalization strategy and cost cutting initiatives. The ironic twist in the story is that the company had to pay $3.6 million in damages for copyright infringement to a company called Visitor – much more than the brand would have likely ever added to the bottom line. We see this as a mutual split between the two parties allowing Slater to try to build his own lifestyle brand with a company with deeper pockets.

The punchline is that we applaud ZQK's restraint – which so few brands have when it comes to these ego-driven deals. Historically, ZQK has spent nearly 85% of its marketing budget on athlete/event sponsorship and T&E, leaving a small pittance for demand creation. Our work shows that this was a gross misallocation of funds. When we surveyed 1,000 Action Sports consumers about endorsements, only 41% thought they were important. Of that 40%, while most people likely knew Kelly Slater, only 17% actually knew that he was affiliated with Quiksilver. While athletes/events are critical to the brand’s identity, these funds are much more effective when used to generate demand leveraging ZQK’s strong brand portfolio.

* * * * * * *

Click on each title below to unlock the institutional content.

Equity Flows: Not Looking Good

“I’ve been trying to reconcile why US stock market volume has been so astonishingly bad (at the all-time highs this week),” CEO Keith McCullough wrote in a note on Friday. “This has to be part of the answer. 2 straight weeks of domestic equity OUTFLOW, and the 7th straight wk of taxable bond fund INFLOW.”

Rate of change is negative for the first time in many months. Positive flows into stocks and out of bonds was a big part of our bullish call on US growth equities in 2013. This recent rally looked like capitulation short covering to McCullough. Data is in the attached note.

Bubble, Overbought: SP500 Levels, Refreshed

Hedgeye CEO Keith McCullough writes, "Risk happens fast."

Gaming, Lodging & Leisure Sector Head Todd Jordan believes a disappointing March could put Q1 regional casino estimates at risk following a nice bounce in the stocks.