“Selling is hard to teach because it is about what exists in your head and what goes on in your whole life.”

- Mrs. Shibata, the top salesperson at Dai-ichi Life in Japan

The quote above come from Philip Delves Broughton’s 2012 book “The Art of the Sale.” In his book, Broughton studies the most successful habits of some of the best sales people across various industries worldwide – from a Moroccan man who sells carpets and tiles in a bazaar, to some of the world’s most famous actors and musicians, to the top saleswoman at Japanese life insurance Dai-ichi Life, to Steve Jobs making the complex simple with Apple’s revolutionary products.

Selling is an art and there is no singular way to be successful at the art of persuasion. Often times the same tactics fail to work consistently; hard work, persistence, patience, charisma, knowledge, perceptiveness and having extremely good product are all qualities that allow for the subjects in the text to find success selling.

The biggest take-away is learning by observing. Incorporating the best practices of others, while simultaneously discarding the negatives, helps us all optimize our daily processes in the never-ending, impossible, pursuit of perfection.

Whether we realize it or not, we are all selling something on a daily basis – pitching an idea to your PM, convincing your current or potential investors why your investment strategy is going to be most effective, or getting your kids to eat their daily serving of fruits and vegetables. Many of our actions are “non-sales selling” practices – i.e. motivating & moving others.

So get out there and make a sale today.

Back to the Global Macro Grind...

In the interest of saving myself the embarrassment of providing my macro thoughts, I’ll leave you with three of our current, non-consensus investment ideas:

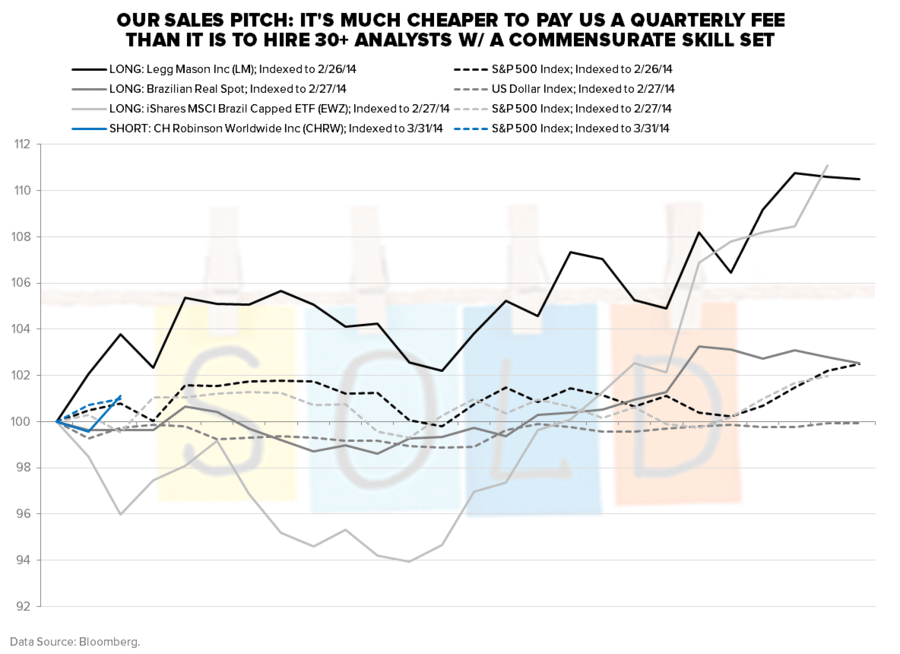

Long Brazil (BRL; EWZ) - Stealth call by the (self-proclaimed) best dressed member of the Hedgeye team, macro analyst Darius Dale; The Brazilian real is up +3.1% Mom and the EQZ ETF is up +12.8% MoM. Our macro team makes calls on the slope of line, and in Brazil’s case, we believe the Growth/Inflation/Policy fundamentals are going from really bad to less – similar to Indonesia last year. Depressed valuations and bombed-out prices make this an interesting market to get involved in if you think US monetary policy is getting easier, at the margins, like we do.

After being the bears in 2013 and heading into 2014, we think EM capital and currency markets are poised to continue outperforming their developed market counterparts over the intermediate-term. In Brazil specifically, the World Cup and upcoming elections are two significant and underappreciated catalysts that could be very positive from both a macroeconomic and investor sentiment perspective.

Short C.H. Robinson Worldwide (CHRW) - This is a rare structural short with low barriers to entry with the advent of lower cost technology solutions creating an increase in the competitive landscape in 3rd Party Logistics. We expect both margin and multiple compression to cut CHRW in half. Sector Head Jay Van Sciver is presenting our black book tomorrow at 11am EST.

Long Legg Mason (LM) – Legg is positioned as a prime beneficiary of pension fund flows out of equities and into fixed income with assets over-indexed to both institutional and fixed income exposure at 71% and 55% respectively relative to peers. We estimate half of the $1T in equity exposure outflows to be reallocated towards fixed income as institutional pension funds look to capture higher re-investment rates. With favorable style factors (i.e. high short interest and bearish sentiment), the highest free cash flow yield in the sector, and discounted multiple, LM continues to be one of our top longs.

Upcoming Events at Hedgeye:

Short CHRW – Tomorrow 11am est.

Long HOLX – Monday 4/7 11am est.

Q2 Macro Themes – Tuesday 4/8 1pm est.

Covering some of the top investors on the West Coast, I have the privilege of learning from some of the top non-consensus thinkers in our industry. It’s fun to learn from all of you on a daily basis, while hopefully helping you make some money in the process!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.67-2.82%

SPX 1

VIX 12.77-14.72

USD 79.41-80.32

Gold 1

The best defense is a good offense,

Ryan Fodor

Associate, Sales