CEO Andrew F. Puzder, says this morning “the decline in our same-store sales remains our management team’s primary focus” – it better be!

CKR reported that blended same-store sales declined by 5.0% during period six; an improvement from period five when comparable sales declined 5.2%! There are not many QSR concepts with same-store sales trends as bad as these.

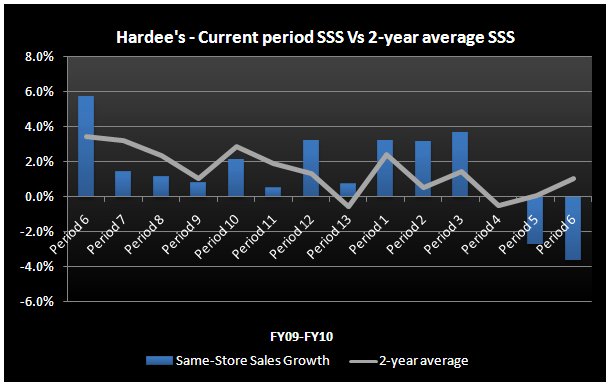

For period six, Hardee’s same-store sales declined 3.6%, compared to an increase of 5.7% last year; on a two-year basis, Hardee’s same-store sales increased 2.1%. Same-store sales for Carl’s Jr. declined 6.1% for period six as compared to an increase of 4.9% last year; on a two-year basis, same-store sales decreased 1.2% for period six.

It appears that a little bit of discounting is creeping into the game plan, but it is not moving the needle on traffic counts. In period six, Carl’s Jr. began running a limited time 2 for $4 Western Bacon Cheeseburger promotion supported with TV advertising. If I’m not mistaken, this is using TV to discount one of the concept’s core products – something management said it would never do. Management is clearly passing some of the benefit of lower commodity costs to the consumer. Without incremental traffic coming into the door, this is a net negative to margins.

Industry leading margins and a mid-single decline in traffic are not a sustainable combination. The only way to get traffic back is to give up some margin in order to improve the company’s affordable perception. Relative to what we are seeing from other restaurant companies over the past two days, there is little upside to EPS for CKE but rather the downside risk is looking better.