This note was originally published at 8am on March 18, 2014 for Hedgeye subscribers.

“Appreciate stories that do not come out well, for they are very much like a good deal of life.”

-James A. Garfield

According to Candice Millard in Destiny of The Republic (pg 19) , that’s what the 20th President of the United States, James A. Garfield, told his kids one night after reading them Shakespeare’s Othello.

Admittedly, I read my kids too many fairy tales. Maybe that’s my escape from the latest chapter of reality that is the US Federal Reserve un-officially Burning The Buck via its Policy To Inflate.

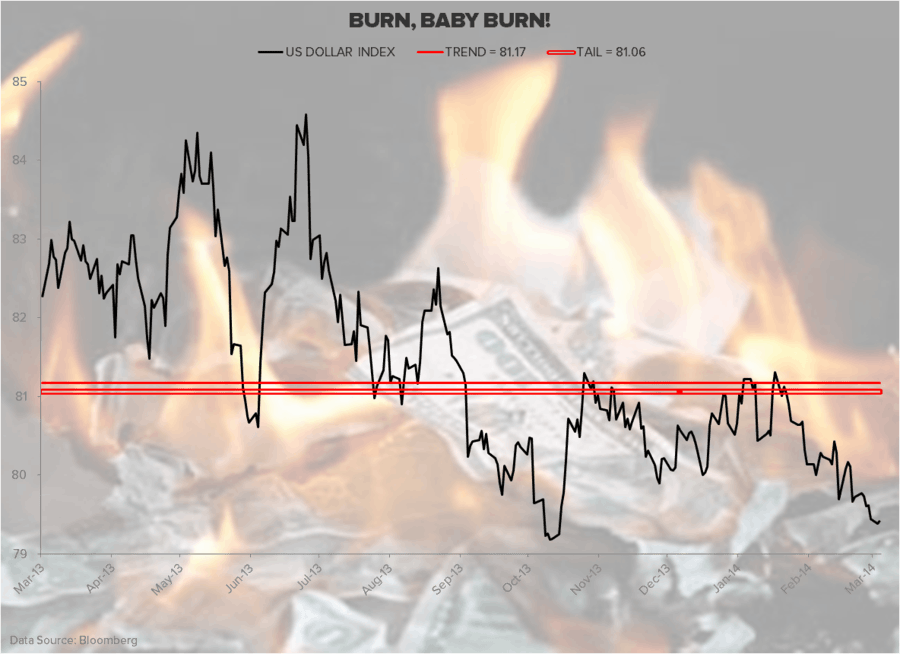

This morning you’ll see the initial outcrop of Dollar Devaluation – consumer price #InflationAccelerating again in the most recent made-up government CPI report. Tomorrow, you’ll see Janet Yellen officially abandon the Fed’s dual mandate and roll with “qualitative rate guidance” (i.e. price fixing interest rates, like Japan did).

Back to the Global Macro Grind…

No, this story doesn’t end well for the US economy and at least 80% of its people. Yes, that is a forecast. And it’s aligned with at least the last 400-2500 years of economic #history.

But don’t worry, the Fed’s main leading indicator (the US stock market) can still go up on this. Venezuela’s was up +460% (in its burning currency) last year, and has since fallen to -5.6% in 2014 YTD. Germany’s stock market went parabolic in the 1920s too.

Dollar Down yesterday perpetuated another no-volume (-20% vs. @Hedgeye TREND) rip in US stocks. While @FederalReserve’s esteemed Ph.D. economists will lie to you and suggest that price fixing the long-end of the curve isn’t “causal” to currency devaluation, it is.

Moreover, what’s left of free-market pricing believes it is – check out these 30-day US Dollar Correlations:

1. SP500 -0.86 (inversely correlated with USD)

2. Commodities (CRB Index) -0.84

3. Gold -0.93

Yep, that’s that. The entire world is front-running Janet Yellen talking down interest rates in the face of #InflationAccelerating.

Since no one who calls the shots at either the White House or the Fed has ever traded macro market risk in their life, don’t expect them to get the most important aspect of risk managing markets – expectations.

If you want to look at the market’s most obvious expectations on US monetary and fiscal policy, look at futures and options positions in the CFTC (US Commodities Futures Trading Commission) data:

1. Gold = +123,007 net long contracts (vs. its 1yr avg of +60,763 contracts)

2. Crude Oil = +432,840 net long contracts (vs. its 1yr avg of +349,652 contracts)

3. US Dollar = -197 net short contracts (vs. its 1yr avg of +17,809 contracts)

In other words, front-running an un-elected cartel of Keynesian economists who make-up new policy rules as they go (the Fed) has turned into a big business on Wall Street. If you don’t believe that, tell yourself fairy tales too.

Like it did in Q1 of both 2008 and 2011, the market is expecting both Congress and the Fed to Devalue the Dollar in the face of slowing economic data. If you go back to the 2011 playbook, you can see that Gold, Bonds, and Utilities (XLU) were beating the Dow steadily.

To review what the market is front-running:

1. FISCAL policy – moar government deficit spending

2. MONETARY policy – talking down the long-end of the curve (rates)

On both of those currency vectors (yes, decisions your elected or un-elected bureaucrats make are causal), unlike last year (when both were Dollar Bullish with sequestration + tapering), Mr. Macro Market is taking the US Dollar to its YTD lows.

In other Global Macro news, Germany appears to be finally slowing. While it’s been a good run for the German economy off its European Crisis lows, here’s the real-time market update:

1. Germany’s stock market (the DAX) broke @Hedgeye TREND support of 9273 last week

2. Germany’s bond market has ramped in the last month with 10yr Bund Yield -10bps m/m to 1.56%

3. Germany’s ZEW (confidence reading) just dropped in March to 46.6 vs 55.7 in February

I know. If China, Japan, USA, and now Germany see the slopes of their economic growth curves roll over (all at the same time) what could possibly go wrong? Oh, and Russia (stock market -23% YTD) is still crashing. This story only ends well in some sadistic dream.

Our immediate-term Global Macro Risk Ranges are now (we have 12 ranges in our Daily Trading Range product):

SPX 1846-1866

DAX 8909-9273

VIX 14.72-17.56

USD 79.21-79.79

Gold 1355-1387

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer