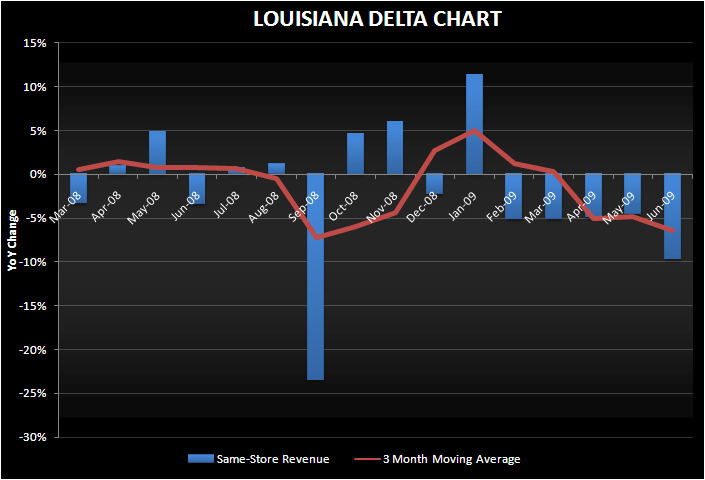

Five straight months of revenue declines without any positive delta. On a moving average basis, Louisiana now looks like one of the worst performing gaming markets.

Well, it was fun while it lasted. After a dreadful September, Louisiana was the best performing market in the country for a four month stretch. That was a critical piece of our positive outlook on PNK beginning in November. Not only did business turn “less bad”, but three out of the four months post September showed positive same store sales.

Since January, however, gas prices have been steadily increasing. The impact of government stimulus and transfer payments has dwindled. Unemployment and the savings rate continue to climb. As can be seen in the following chart, the same store revenue picture reflects the harsh economic environment. Moreover, the 3 month moving average is decidedly negative and the slope of that line is the steepest of all the gaming markets.

These results do not bode well for PNK which maintains 69% of its EBITDA exposure to Louisiana. We’ve adjusted our model to reflect the state issued revenues, including these Louisianan numbers just released. We are now expecting Q2 EPS of $0.02 on an adjusted basis versus the Street at $0.05. Our adjusted EBITDA estimate is $47 million, approximately $2.5 million below the Street. Our revenue estimate is $260 million versus the Street at $272. We do think better margins will partially offset the revenue shortfall.

PNK will release earnings this Friday before the open.