Below are Hedgeye analysts' latest updates on our TEN current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We added two new names this week: Hologic and Legg Mason.

We also feature three research notes from earlier this week which offer valuable insight into the market and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

CCL – Carnival traded down 6.8% this week while the S&P 500 Index was down 0.5%. Last week’s optimism regarding improving European economies and stronger European consumer spending was quickly tempered when Carnival announced fiscal first quarter 2014 earnings on Tuesday prior to the market open. Recall, our proprietary March 2014 cruise line pricing survey indicated the Carnival brand showed the greatest positive pricing momentum in sequential pricing among the big 3 cruise line operators in March 2014.

During the company’s earning conference call, Carnival confirmed the uptick in pricing we saw in our survey – which is a positive fundamental trend. However, investors reacted negatively to Carnival’s forward earning guidance.

Our full-year fiscal earnings estimates remain above management’s guidance as we remain convinced the recent pricing power is both sustainable and enduring – and will ultimately translate into better than expected revenues and earnings. We view the recent price weakness as temporary, as well as a great entry point for accumulating CCL shares.

DRI – Earlier this week, Barington Capital wrote a letter to Darden’sindependent directors suggesting they begin their search for a new CEO. Barington CEO James Mitarotonda blasted current Darden CEO Clarence Otis, noting his concern with the “rapidly deteriorating financial performance” of the company.

It’s becoming an increasingly fragile situation over at Darden.

Shareholders and activists are beginning lose all faith in the current management team. Mitarotonda, who previously called for the Chairman and CEO role to be split, is leading an increasingly public campaign against the company.

In response to Mitarotonda’s letter, Darden once again urged shareholders to reject the special meeting and, once again, failed to provide a legitimate reason to do so. If the company is so confident in their plans, they should welcome the meeting and leave the floor open to debate. Instead, they are doing everything in their power to push forward with the plan to spin-off Red Lobster – without the approval of shareholders! This tells us they are hiding something and puts a huge question mark on the company’s already questionable credibility.

HCA – Since being added to Investing Ideas on 6/14/13, shares of HCA Holdings have risen 27% doubling the 13.5% return on the S&P 500. Healthcare Sector Head Tom Tobin will have a new update next week.

HOLX – Hedgeye Healthcare Sector Head Tom Tobin added Hologic to Investing Ideas earlier this week. Click here to read the full report.

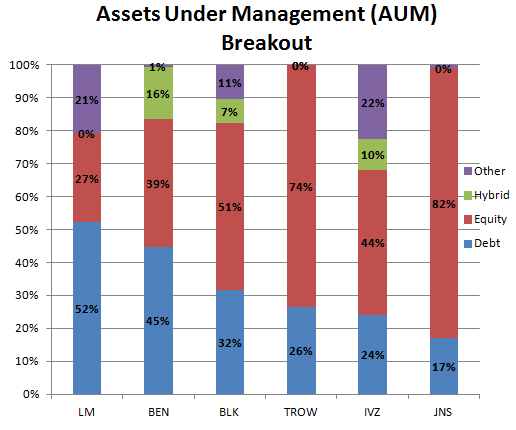

LM – We added Legg Mason (click here to read the full report) an asset management company based in Baltimore to Investing Ideas this past week.

In a nutshell, we think shares have over 20% up over an intermediate term duration.

Our investment thesis on the stock is predicated that “at funded” U.S. corporate pensions are now de-risking from equities after over 5 years of outperformance in the asset class and are shifting asset allocation into fixed income and alternatives. This will benefit leading bond managers most specifically Legg Mason which has the largest exposure of the publicly traded asset managers to institutional fixed income assets.

Separately, we estimate that as the Fed starts to taper and come off of the bond curve, that interest rates will actually decline and not increase because a reduction in quantitative easing will slow growth. This will also benefit leading bond fund managers as fixed income performance can improve after last year’s dismal returns. We think the company can earn $3.50 next year, 10% above Street estimates, which at an industry multiple would translate into a fair value of $60 for the stock.

With 11% short interest (the second highest in the group) and the lowest ranked stock of the big 6 public asset managers (with only 3 buys in coverage by 18 analysts) even just marginally improved trends should send this stock to a much improved valuation range.

LO – Shares of Lorillard were up 2.3% on the week – in-line with a stock we think will grind higher on advantaged menthol fundamentals, limited regulatory risk, and a growth engine in blu e-cigarettes.

This week we held conference call with the President of LOGIC, a private e-cig manufacturer since 2010 with the #2 national brand in unit and dollar share for C-Stores in the United States (according to Nielsen).The substance of the call substantiated our bullish outlook on the e-cig industry.

We continue to believe that the e-cig industry will consolidate, led by Big Tobacco, and in particular by Lorillard. We expect blu to continue to maintain its category leadership, despite increased e-cig competition from RAI (Vuse) and MO (MarkTen).

OC – This past Monday CEO Keith McCullough, appeared on “Opening Bell” with Maria Bartiromo and pointed out companies like Owens Corning which are able to absorb inflation in its pricing. While #InflationAccelerating is not the dominant point of our thesis, we believe it will not be a headwind compared to other companies, who are dependent on lower energy and food costs.

We are more interested in supply and demand imbalances. With residential and non-residential construction needing to double to return to post-WWII averages, the company with the largest market share (among other factors) in building products subsections can benefit tremendously from these imbalances. Owens Corning holds approximately 40% of a reasonably consolidated market for fiberglass insulation. OC shares ended the week up 2.3%.

RH – Shares of Restoration Hardware rocketed over 12% on Friday after the company reported better-than-expected results and guidance.

For the record, RH remains our highest conviction long idea in the Retail space, with ultimate earnings power of $11 per share and a stock price in excess of $200.

The company’s 4Q print supported our thesis in many ways. But despite all the positives around revenue outlook, store growth, and margin upside, the biggest growth in the quarter from our perspective was not found in a line item…it was in the CEO.

When we talk to investors about RH, almost every single critic lists Gary Friedman as a chief concern now that (former Co-CEO) Carlos Alberini has left the picture. In investors’ minds, Gary was the product guy, and Carlos did everything else. That’s an incorrect view, but like it or not, that’s the perception. Well, this quarter Gary literally sounded like a different person. He spent more time talking about ROI, capital deployment and managing risk in the business as he did talking about product and merchandising. The only question to be answered is whether this is just a temporary Gary we’re seeing in the immediate wake of Carlos’ departure, or if this marks a structural change to how he approaches his role. Critics will claim the former. We think it’s the latter. Time will tell, but there’s no disputing the change as it appears today.

We’re not making any material changes to our estimates. We still think that the company will have a far better year than it’s guiding. As much as that should make the stock continue to grind higher, the real upside comes from earnings expansion as this growth story plays out – which literally begins in April/May with the redesign of its product line, launch of its Sourcebook (all 3,200 pages of it), and the opening of the new store in Greenwich (which kicks off a mini-burst of square footage growth).

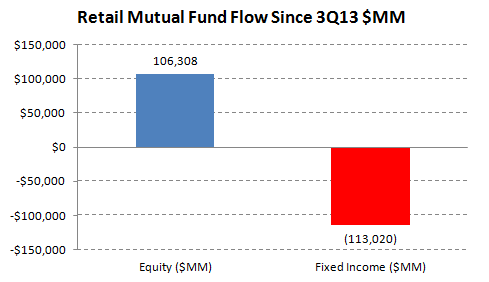

TROW – Shares of T Rowe Price are bouncing around with the market as of late, but we encourage investors to stay the course. In our initial asset management sector launch in the middle of last summer, we highlighted a forthcoming investable shift in mutual fund flows from outsized fixed income asset allocation by retail investors since 2008 and the Financial Crisis into equity mutual funds which hadn’t seen any annual inflow since 2007. This would benefit T Rowe Price as the leading equity mutual fund provider with the industry’s best performance in hoovering returning equity inflow.

The shift into equity funds from bond fund has been significant over the past 9 months and we estimate this will be well reflected in the upcoming 1Q 2014 earnings report from TROW, which will have the best numbers in the group. We then think shares will have appreciated to a level for investors to take a breather on TROW stock and focus on Legg Mason, which has better intermediate term prospects on institutional asset management trends as outlined above.

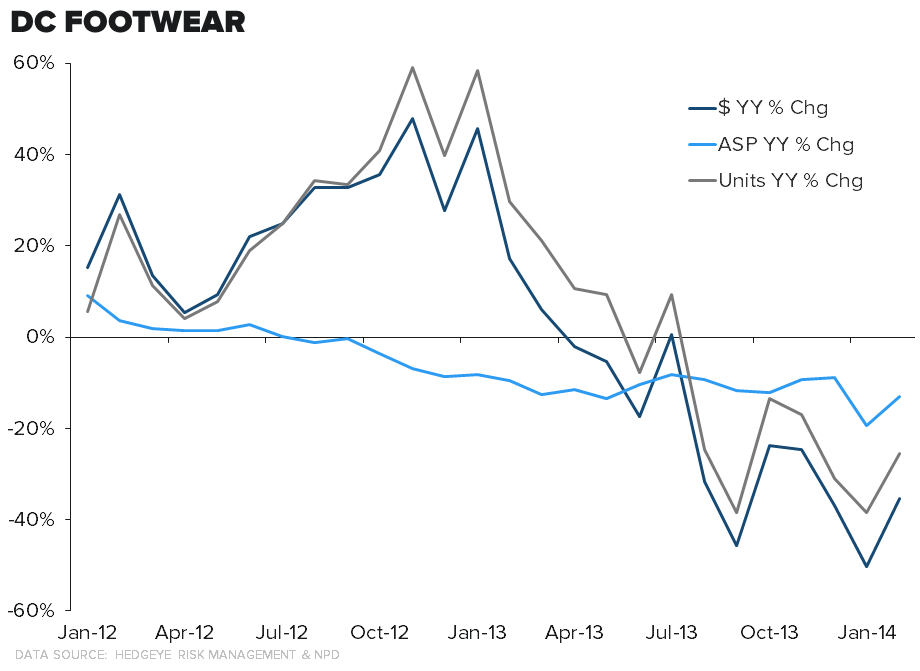

ZQK – One of the points of emphasis for Quiksilver is footwear. The company’s CEO, Andy Mooney, has a strong pedigree in the space having grown up at NKE, and it’s a category that is significantly underpenetrated accounting for just 25% of sales in 2013. There is opportunity for all three brands, but the main focus of that push will be concentrated on the obvious candidate, DC.

DC was in the worst shape post management shakeup in early 2013. Take a look at the brands recent US Wholesale sales trends below. What happened is DC rode a fashion trend from Spring ’12 through the end of that year and purchased inventory based on the assumption that those trends would continue. Except the trend didn’t continue into ’13 and the company was left with a pile of inventory on its balance sheet. In order to liquidate the excess, DC was forced to up its promotional cadence and ASP (average sale price) has fallen for 16 straight quarters.

Coming out of 1Q14 the company is in a much better inventory position and able to buy appropriately for the company’s push in 2H. This coincides with the brand repositioning itself in the vulcanized footwear segment. 120mm pairs of vulcanized shoes are sold per year at the $45-$55 price point – DC, who focused on higher priced technical product, has virtually no presence in this lifestyle segment which is dominated by Vans. Starting in the fall, DC will finally go to market with an assortment focused on the lifestyle consumer and we expect ZQK to leverage DC’s extremely relevant brand identity to kick start footwear.

* * * * * * *

Click on each title below to unlock the institutional content.

Panera Bread: Expect Some Near-Term Pain

Restaurants Sector Head Howard Penney has upped his conviction in PNRA as a high-quality short.

Does the Emerging Market Relief Rally Have Legs?

We are inclined to believe the current relief rally across EM capital and currency markets has legs w/ respect to the intermediate term.

Bubble Up: SP500 Levels Refreshed

"I’ve seen a lot in trying to trade markets for the last 16 years," writes CEO Keith McCullough. "But I haven’t yet seen something like this."