SUMMARY BULLETS:

- #ItsNot2013: Growth estimates globally continue to get marked down. Slowing topline (GDP) and compressing margins (rising inflation) is not the stuff of market multiple expansion or macro P&L dynamics to remain lazy long of.

- RISING INEQUALITY: Corporate Profits - measured as the % of National Income or GDP - made another new high in 4Q13. The other side of that, of course, is a lower low in labor’s share of income. Latent risks can remain latent.

- CAPEX RESURGENCE? General acknowledgement that assets are aging and businesses have under-invested isn’t a catalyst.

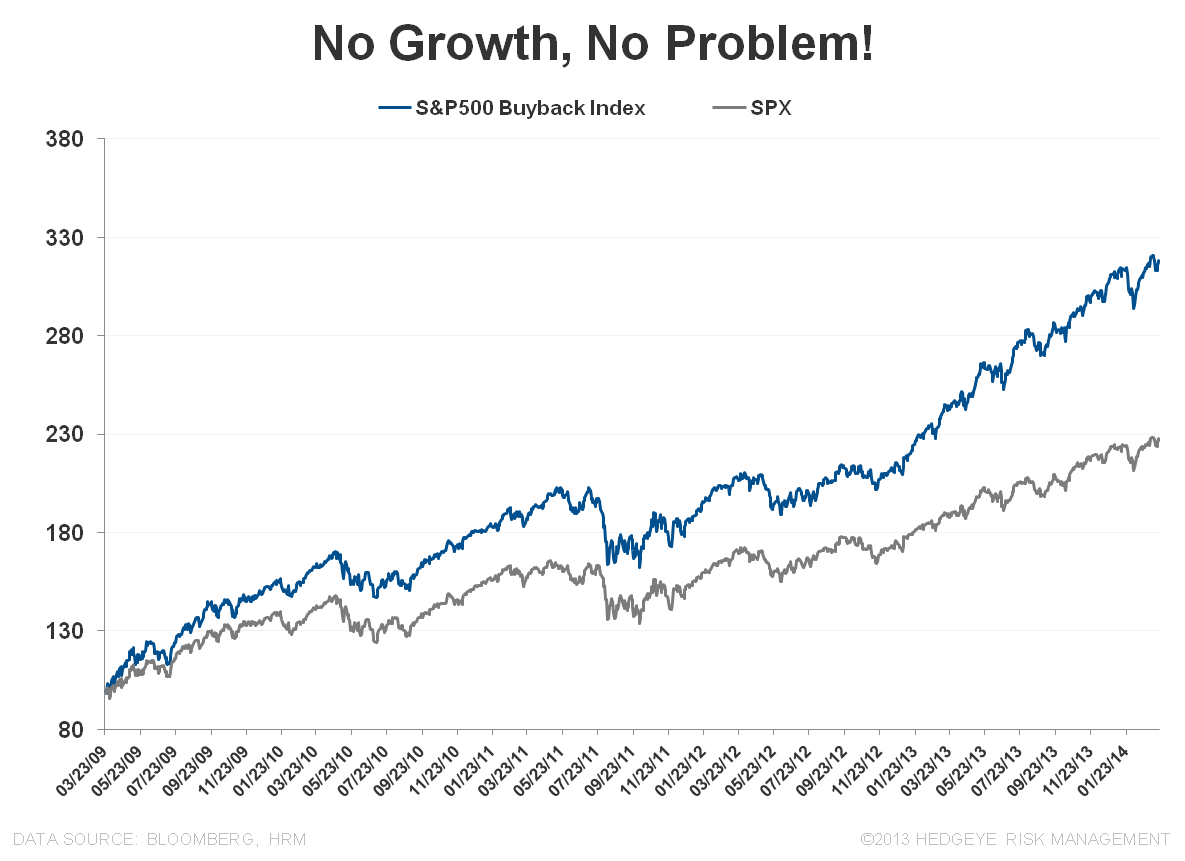

- PAY-ME-NOW: Productively continues to grow at a positive spread to unit costs and investors continue to reward the ‘pay-me-now’ corporate capital strategy.

- DURABLE DISAPPOINTMENT: New Orders for Capital Goods non-Defense Ex-Air have been negative on a month-over-month basis for four of the last six months.

- INITIAL JOBLESS CLAIMS: A positive week of data…finally. The next few weeks of data should be important

We summarily re-hashed our 1Q14 macro view along with our current thinking from a strategy perspective in a note late last week - #PROCESS: SUMMARIZING OUR CURRENT VIEW.

Below we highlight the notable trends across this morning’s GDP & Initial Claims data

GDP: GROWTH ESTIMATES FALLING

In short, with inflation estimates unchanged, the +0.2 positive revision to 4Q13 GDP resulted as the net of a +0.49 revision to consumption (driven by services) and -0.31 revision to investment (driven by downward revision to nonresidential investment).

The table below provides the detail on the final estimate and the complexion of the final revision.

Domestic growth expectations, meanwhile, continue to come in with the 1-month and 3-month change in 1Q14 GDP estimates down -30bps and -80bps, respectively.

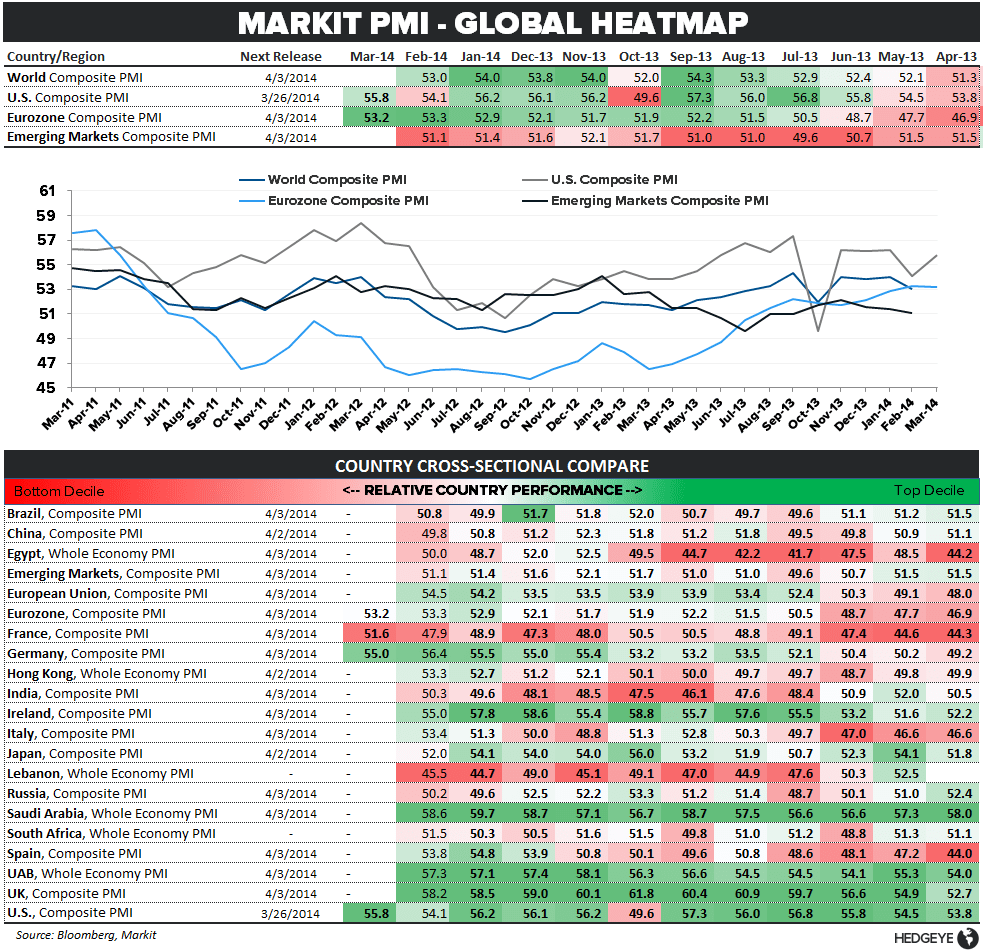

Looking globally, the story is similar with growth estimates for 1Q14 and full year 2014 getting marked lower across both developed and emerging economies while inflation expectation, particularly across emerging markets, are beginning to flash some upside

(Note: we can email the tables below for a cleaner visual if you're interested)

As we’ve highlighted repeatedly QTD, slowing topline (GDP) and compressing margins (rising inflation) is not the stuff of market multiple expansion or macro P&L dynamics to remain lazy long of. #ItsNot2013

CORPORATE PROFITABILITY: RISING INEQUALITY

Corporate Profits - measured as the % of National Income or GDP - made another new high in 4Q13. The other side of higher highs in corporate profitability, of course, is that labor’s share of national income made another lower low.

The un-sustainability of that trend and the associated mean revision risk to peak margins remains perhaps the broadest, and most obvious, latent risk to investors.

The bureaucratic prescription for a (largely) policy driven rise in inequality, as we’ve seen with the recent statutory wage increases, is more policy aimed at legislating spread compression in the division of income via a de-facto income transfer from owners of capital to labor.

Please see our note LOSE-LOSE? WAGE INFLATION & LABOR'S BAD BANK for a fuller discussion of the impact of wage controls on labor economics.

With the income spread expanding and the goal of monetary policy effectively amounting to a hope for the ultimate trickle down/trickle around wealth effect, expect more populist rhetoric out of the beltway to help further churn existing populace angst.

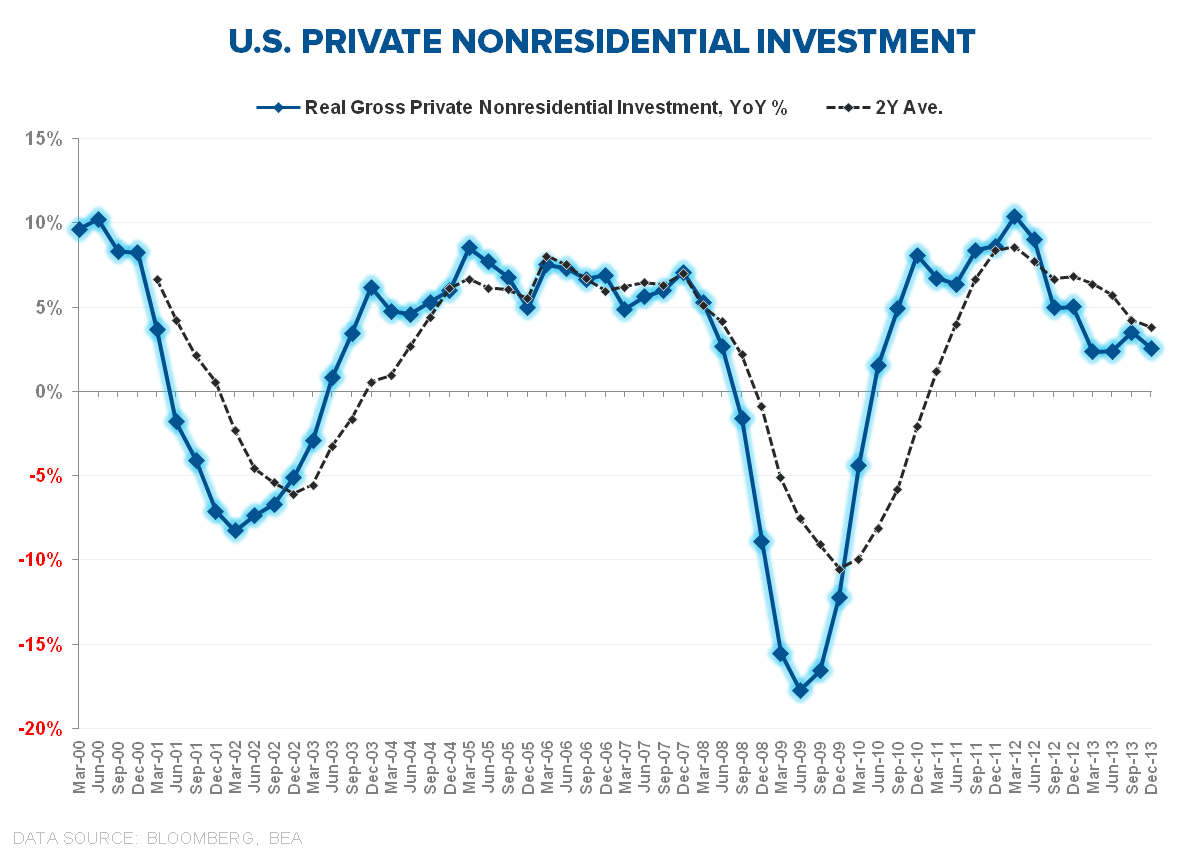

CORPORATE CAPEX: THE GREAT PHANTOM RESURGENCE

Expectations for resurgent corporate capex have been fairly pervasive of late. Indeed, varying iterations of that same narrative/expectation have ebbed and flowed for the better part of 4 years now.

From a growth perspective, real gross private nonresidential investment growth extended the broader deceleration trend in 4Q13, slowing 90bps sequentially to +2.6% YoY.

Fairly, net private investment as a % of GDP continues to recover and the average age of the aggregate capital stock may be above historical triggers for accelerated capex spending, but that’s been true for a while now and general acknowledgement of that reality doesn’t make it a catalyst.

As it stands currently, productively continues to grow at a positive spread to unit costs and investors continue to reward the ‘pay-me-now’ corporate strategy.

There are some inflationary wage pressures percolating but they are far from acute and, with a little leverage & planned repo in the model, peak margins can stay peaked and EPS can continue to grow at a premium to topline over the intermediate term.

So, on balance, fundamentals aren’t signaling an immediate need to shift strategy and the prevailing corporate capital policy – which continues to reward both investors and management teams - has nearly a decade of inertial momo behind it.

Necessity may drive an ongoing, gradual shift towards rising capex but data supporting an imminent and significant inflection in business investment isn’t particularly compelling.

DURABLE GOODS DISAPPOINT (AGAIN)

Yesterday’s preliminary Markit PMI data for March was positive but the February Durable Goods figures were decidedly disappointing with the -1.3% MoM decline in core capex orders the notable, negative outlier.

Indeed, New Orders for Capital Goods non-Defense Ex-Air have been negative on a month over month basis for four of the last six months.

Weather distortion or not, measures of business investment and activity (Durable goods, Industrial Production, ISM, rising sales-to-inventory ratio’s) have to see a material, sustained acceleration from here for the resurgent corporate investment thesis to regain credibility.

INITIAL CLAIMS: PLAYING THE INFLECTION

In contrast to the accelerating improvement in jobless claims that characterized most of 2013, the 2014 trend has been one of discrete deceleration.

However, with headline rolling claims declining -9.5K WoW to 317K and the rate of improvement in the rolling average of non-seasonally adjusted claims improving 360bps sequentially, this week’s data was decidedly better.

Josh Steiner, our head of Financials research, provided the following context:

The labor market could be characterized as showing decelerating improvement since the start of January this year. This week marks an inflection from that trend. The year-over-year change in NSA initial claims came in at -13.4% this week, the strongest print since January 3, 2014 and a moonshot compared with the -5.0% print last week. This week was so strong, in fact, that it brought the rolling NSA y/y to -7.1%, up from -3.5% last week. We'll see in the weeks ahead whether the trend is beginning to reverse.

One of the arguments put forward in support of the generally weak 1QTD data has been weather. If weather is playing a role in suppressing the strength of the data then one would expect that as we move from the winter to the spring months we could reasonably expect to see improvement in the data. The next few weeks of data should be important in this regard, as they may serve to answer this fundamental question

Christian B. Drake

@HedgeyeUSA