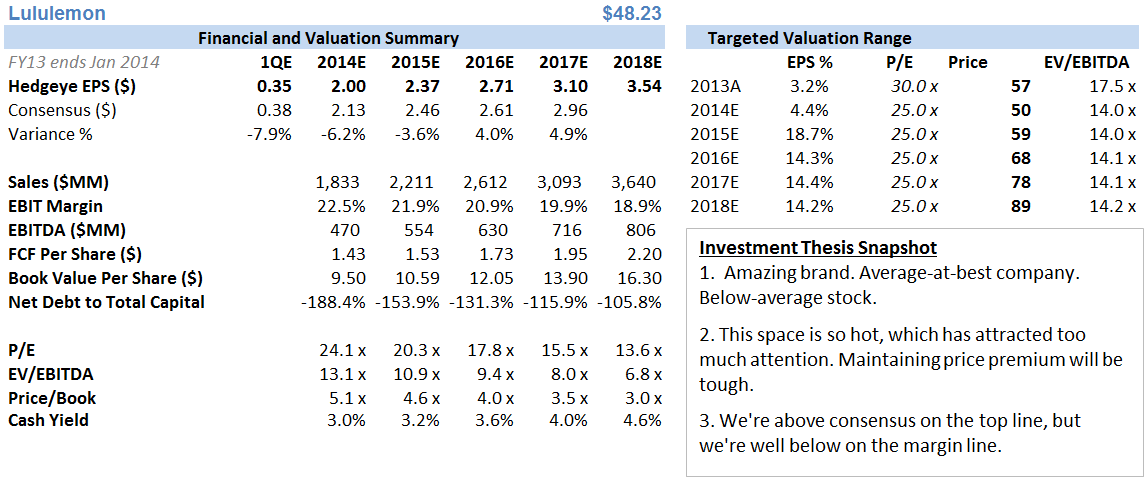

Conclusion: No surprises for us with the LULU 4Q print after what we laid out in our Black Book on Monday (see our excerpt note below LULU: Why We’re Pulling the Plug on the Bear) where we reversed our bearish stance and turned cautiously bullish. The quarter in itself was hardly anything to celebrate – flat EPS on 7% top line and 20% inventory growth – that’s not exactly an algorithm of excellence . Yes, the company beat, but it beat horrible expectations. The good news for us is that the upside came from the top line, which is something that our research suggests has found a bottom. We think that over time, top line expectations are meaningfully too low – the catch is that margin expectations are about 600bp too high. That might seem like a push (good sales vs bad margins), but with the stock (and sentiment) where it is today, we view the better top line equation as bullish.

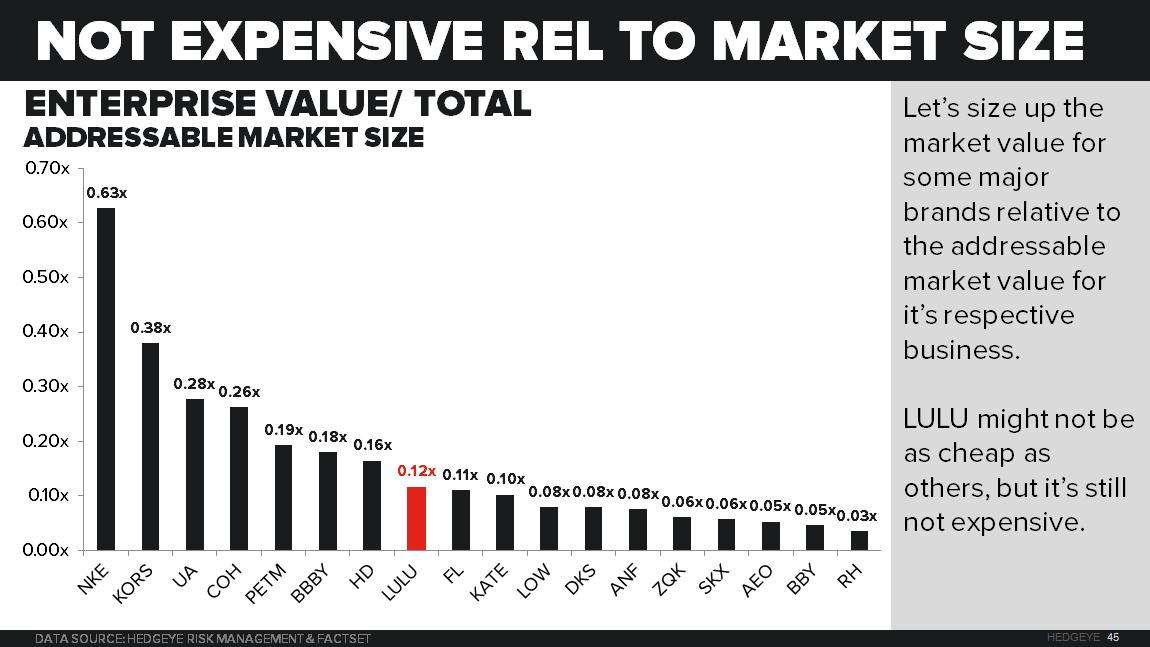

Our only real disappointment is that we were looking for an opportunity to take our recent reversal a step further and get outright bullish. The fundamentals didn’t present the ammo for us, and the stock price certainly is not giving us a ‘buy on the freak out’ opportunity. For now, we’re still ‘cautiously bullish’. The stock is trading at about 22x 2015 earnings, and 11x EBITDA, and is on the cheaper side of retail peers when sized against its total addressable market size (EV/TAM). How we’re doing the math, we don’t get more concerned about margins until either a) we’re proved wrong on top line or b) the stock is well into the $60s.

Here are just a few thoughts on some of the themes that came from the call.

Seasonal product – Easily the most talked about topic on today’s call. LULU has used the scarcity model when making seasonal buying decisions to keep demand high and limit discounting. New management emphasized the investments in processes that would allow for deeper buying in these categories and noted that the current 50% core/ 50% seasonal mix would start to favor seasonal. There are puts and takes for both strategies, but it’s inevitable for the brand if it wants to grow up.

- It’s interesting how they stress ‘seasonal’ and don’t acknowledge the word ‘fashion’. Call it what you want, but seasonal product carries more fashion risk. That means higher discounts. We think LULU needs to go there. But let’s call it what it is.

- Deeper seasonal collections will help drive the top-line. This is especially true in mature markets where the comp is driven by seasonal merchandise. A long replacement cycle means that core can’t carry the comp.

Mens – Thankfully it appears that the previously announced standalone Men’s doors won’t be happening. We think there is opportunity in men’s. Now it accounts for about 15% of revenues and that penetration should grow higher in the coming years. New doors with a greater male footprint is great, but we were never fans of the standalone men’s concept. Capital should be channeled towards proven concepts, international, and product/infrastructure improvements.

55/25 Margin Targets – Management didn’t say much when asked directly about the company’s long term 55% gross margin/ 25% EBIT margin targets other than to note that in the near term margins would be under pressure due to investments. We’re thinking we’ll get more detail at the coming analyst meeting. We don’t think that LULU will take down the targets materially at the meeting. It will more likely be a slow bleed as LULU pumps more sales dollars through the system.

03/25/14

LULU: Why We're Pulling the Plug on the Bear

Takeaway: We pulled the plug on our LULU Bear call. Our work clearly shows that things are improving. If the qtr is weak, we may get outright bullish.

Conclusion: After being extremely bearish on LULU since the fall, we're changing our position on the name. While we are not outright bulls at this point -- and while we believe there are extreme challenges for LULU from here -- we do not think that the bear case carries meaningful merit. If the quarter is sloppy and the stock trades down, we may get outright bullish.

DETAILS

As background, we had been long-term bulls of LULU, but last fall turned bearish as LULU's well-publicized gaffes started to come about. Then we conducted a detailed consumer survey of 500 female Yoga shoppers (80% of whom were LULU customers) across appropriate demographic groups. That survey -- conducted three months ago -- told us to press our short, and it was right to suggest we do so.

But yesterday we released an update to our survey, which asks the same detailed questions (and then some) to the same demographic group. The punchline is that things are unquestionably getting better on the margin. We outline all of the reasons why, and then some, in our 52-page slide deck, the link to which is below. Also, if you care to listen to the accompanying presentation, that audio link is below as well.

One slide we'll highlight is #12, which shows the 'Brand recommendation factor' now versus when we first ran the survey at the beginning of the year. The question asks the extent to which consumers would recommend each of 18 brands to their friends. At the start of the year, LULU ranked embarrassingly low. But today, it is right in line with peers. There's definitely room for improvement. But things have gotten better on the margin, and that's what matters most to us.

By no means is the change in our opinion based on one simple question. But many of the questions that we asked -- especially those where we could compare today's results versus those from the start of the year, simply suggest that anyone playing on the short side for things to materially worsen from here has a pretty tough risk/reward on their hands.

Are their challenges? Sure. Athleta (GPS) is emerging as a major threat to LULU's business, and Nike is strengthening on the margin. Also, based on our results we think that there is a problem with perception of value for LULU's product, which suggests to us that the company will have to start a more meaningful discounting strategy.

In the end, we come out much higher on the top line over our 3-5 year modeling period, but we have margins going from 24.5% to just under 19% (see Exhibit below). While multiples rarely expand when margins are coming down, we think that with the stock having a 4-handle, better top line will probably win over margin degradation.

If the company gives weak guidance on the quarter, based on what we see we'd likely look to get more aggressive on the name.

HERE'S A LINK TO OUR FULL SURVEY AS WELL AS THE AUDIO PORTION OF THE PRESENTATION

MATERIALS: CLICK HERE

AUDIO REPLAY: CLICK HERE