RETAIL FIRST LOOK: I LIKE NEW STUFF

21 JULY 2009

TODAY’S CALL OUT

I like new stuff – sometimes to a fault. I’m the guy that can’t run the same trail twice. It’s gotta be new every time. That’s why it kills me to repeat myself on Under Armour. Yet ANOTHER analyst came out this morning with a cautious view in advance of the quarter. Why? ‘Checks suggest that footwear sales are weak.’ Yes, this comes on the heels of comments last week from another analyst that downgraded because "Current Macro Trends and Retail Inventory Levels Are of Concern." Can ANYONE come out more negative on this name? Only 2 out of 23 analysts are positive, the short interest is sitting at 28% of the float, and no one I’ve spoken with has a unique short case.

Are these trends concerning? You bet. That's why it's never been easier to craft a short case. Core apparel sales are flattish, footwear is performing 'fine' (i.e. not stellar), management has been selling stock, key internal positions have turned over, prior guidance is vague, 2Q just closed after it rained for 80% of the most important month of the quarter, and at 26x earnings it is one of the most expensive stocks in retail. The stock is resting right on top of $21 TREND support. I can't say that I blame the bears...

But whenever it is so easy to craft a short case, one needs to ask what the long case is. NO ONE who owns UA does so because they think that the company will smoke the upcoming quarter or year. They largely own it because they think that this company can, and will double in size over 3 years.

Bulls are unlikely to throw in the towel unless the company does. UA will definitely not back off its growth strategy, and in fact is likely to highlight organizational changes to take the footwear organization to the next level.

Also, what about the call option of better footwear pricing out of Asia in the coming 12 months (which I think is underappreciated)? How about ANY success in moving the needle with women's biz? How about the new CEO at Foot Locker that wants nothing more than smaller brands to succeed as he looks to make something out of the disaster that is Foot Locker?

I'm still in the camp that a nugget of positive news will have a disproportionate impact on the stock than negative news. Check out our 7/8 note - UA: The Duration Bifurcation.

We’re working on some analysis to show the addressable market for UA. Stay tuned for that one…

LEVINE’S LOW DOWN

Some Notable Call Outs: A quiet morning in advance of a barrage of earnings reports. Two notable call outs come from across the pond…

- Next (UK’s second largest clothing retailer) warned that a rebound in sales caused by warmer summer weather is unlikely to last.

- While the likes of JJB, JD, and Sports Direct continue to suffer in a rather self-destructive way, U.K. department store chain Debenhams PLC is playing offense while competitors suffer. The company is launching a new Sport & Leisure concept on July 26. The retailer is expanding into the High Street sports market following research showing that customers are turning away from traditional, male-orientated sports retailers and are instead looking for a fashion-led offer. Sport & Leisure will be introduced into 41 stores nationwide and online. The department will cover men’s, women’s and children's clothing, footwear, accessories and equipment for sports, leisure, surf, yoga and outdoor activities, and will include many big brand names (Nike, Adidas, and the like).

- Dick’s Sporting Goods is attempting to clean up its athletic shoe inventories before Back to School season with a Buy One Get One 50% Off sale. This event synchs with the reported weekly scan data we have seen out of the sporting goods channel. Sales of athletic footwear fell 9% in May, 11% in June, and are currently down approximately 13% for the month of July.

- Cache highlighted renewed weakness in its California markets. While hardly a proxy for all of retailing, the commentary is noteworthy because it also suggested that the current budget crisis coupled with the real estate fallout are leading to an acceleration in the already negative trend. Over the past few months, commentary on the state has been mixed, with some companies like ROST highlighting it as above average while others including HD suggested were weakening.

- Amazon’s Kindle and e-book business are about to face some competition from Barnes & Noble, the largest bricks and mortar bookseller in the US. Last night, BKS announced its own digital bookstore, with downloads that can be read on a variety smartphones and mobile devices. Additionally, a competing device to the Kindle will be unveiled in early 2010 in a partnership with Plastic Logic. Historically, BKS has been a follower of AMZN when it comes digital distribution. However, it’s interesting to note that BKS actually experimented with e-books back in 2000 and ultimately scrapped the test in 2003 due to lack of demand and market acceptance. Whether BKS can kill the Kindle is up in the air, however there are two main takeaways from this announcement. First, the consumer probably wins here. Competition leads to better pricing for the consumer and ultimately I would expect pricing on e-books to come down. Secondly, with the two biggest forces in bookselling focused on digital distribution, publishers will have to begin to rethink their business models. If anything has been learned from the music industry vs. iTunes battle, publishers should embrace this move wholeheartedly and begin to envision a world with fewer printed books.

- The Chicago-area retail real estate vacancy rate accelerated to 11.6% in Q2, reaching the highest level in the last 15 years. Retailers closing doors and a continued wave of construction fueled the 8th consecutive quarter of vacancy increases. Discount retailers Target and Wal-Mart have recently opened up stores in the Chicago area, taking advantage of the favorable environment that affords companies with solid balance sheets. Retailers with the highest exposure to Chicago as a percentage of their total store base are: Ralph Lauren 8.2%, Sports Authority 7.1%, H&M 6.5%, Urban Outfitters 5.2%, DSW 5.0%, Calvin Klein 5.0%, and Saks 4.9%. Trends in Manhattan aren’t much better, with vacancy rates on Madison Avenue rising to 15.5% and rents decreasing by one-third year over year.

MORNING NEWS

- Kellwood still trying negotiate loan agreements to avoid bankruptcy - Kellwood Co.’s noteholders continue to provide it with additional time to work out its financial arrangements. The St. Louis-based sportswear firm has been granted two additional extensions on the maturity date of $140 million in notes. The first expired at midnight Monday and the second is set to expire at midnight Wednesday. Two deadlines passed last week without a resolution of the notes issue. A spokesman for Kellwood said negotiations with noteholders, in particular with Deutsche Bank, are ongoing. As long as negotiations continue, there is the possibility of additional extensions beyond Wednesday, he added. Meanwhile, Kellwood also has been granted forbearance from its lender for a few weeks, the spokesman said. The agreement allows the apparel firm to hold off making payments on the principal and interest on its loan on a temporary basis. It still bears the responsibility for making those payments at some point. <wwd.com/business-news>

- Wal-Mart working the press today….

- Launched a TV ad campaign reflecting business leadership by supporting health care bill - Wal-Mart Stores Inc., continuing to burnish its image as a leader in the business community on health care reform, has launched a TV advertising campaign running in the nation’s capital. The retail giant recently caused a rift in the industry, specifically the National Retail Federation, when it endorsed a controversial employer mandate provision in health reform legislation being drafted on Capitol Hill. But Wal-Mart has scored points with President Obama, longtime critics, neutral observers and even some labor groups for endorsing employer mandates in conjunction with the Service Employees International Union and the Center for American Progress, a liberal think tank. Wal-Mart covers 51.8 percent of its 1.4 million U.S. employees with health care benefits, according to a spokesman. He said 5.5 percent of the company’s workforce is uninsured, while 94.5 percent of its U.S. employee base has some type of health care insurance either from the retailer or elsewhere. <wwd.com/business-news>

- Settles a class-action discrimination lawsuit - A federal judge in Little Rock, Ark., has approved a $17.5 million settlement of a class-action discrimination lawsuit against Wal-Mart Stores Inc. The retailer in February said it had reached a settlement in the case, which charged that Wal-Mart turned away black applicants for truck-driving positions. Wal-Mart denied any unlawful discrimination. The settlement includes job placement for 23 drivers who sued the company and an agreement by the retailer to put a greater effort toward minority job recruitment. <capitaliq.com>

- Hires BNP, Mizuho, Mitsubishi UFJ to Arrange Samurai Bond Sale - Wal-Mart Stores Inc., the world’s biggest retailer, hired BNP Paribas Securities Japan, Mitsubishi UFJ Securities Co. and Mizuho Securities Co. for a sale of samurai bonds, according to a filing. <bloomberg.com/news>

- Urban Outfitters hires database marketing agency - Urban Outfitters has selected database marketing agency Merkle Inc. to manage data, analytics, strategy and build a comprehensive custom-built database infrastructure called a Knowledge Center for executing multi-channel marketing programs in the US. The deal encompasses all of the company's retail brands, which include Urban Outfitters, Anthropologie and Free People. From Urban Outfitters' perspective, the move will enable it to promote its brands more consistently to customers. <dmnews.com>

- Jarden Corp preannounces positively - Jarden Corp., the parent of Coleman, K2 Sports and Rawlings, said it expects to meet or exceed analysts' consensus estimates for eps and to be in line with or slightly better than analysts' estimates. <sportsonesource.com>

- Hermes Q2 sales up 12% on handbag, scarves, and perfume business - Hermès International reported a 12% rise in second-quarter sales, helped by demand for its iconic handbags and scarves. The Paris-based company cited “persistently strong” demand for its leather goods, pushing sales in the category up 33.4%. Despite a small improvement in its perfume business, sales for other sectors declined, with watches and tableware hardest hit. As for the remainder of 2009, Hermès said the trend seen in the first half is in line with its target of steady sales for the full year at constant exchange rates, with a slight contraction in current operating income. <wwd.com/business-news>

- Montreal based jewelry retailer Birks & Mayors Inc. suffered 26% sales decline and a weak outlook - Comparable-store sales declined 20%, as a 13% decline in Canada partially offset a 26% dip in the U.S. Currency translation. The firm has been “encouraged” by an improvement in the rate of same-store sales declines since April, but concluded that “the competitive landscape, including the liquidation sales of jewelry and timepieces, will continue to create a challenging sales environment for the company and the jewelry industry.” <wwd.com/business-news>

- Online fashion store Shopbob.com launches new look and functionality - Shopbop.com, the Madison, Wis.-based contemporary online fashion store, has launched a new look and upgraded functionality. The new site, which officially made its debut on Monday, introduced elements such as the “Shop Your Style” section, where customers can browse looks within five mini boutiques — classic, edgy, bohemian, girly and casual chic. There’s a “Shop by Occasion” area of the site, where shoppers can search for items specific to the event for which they are looking to dress — the office, summer wedding, black-tie affair, weekend essentials, night out or beach vacation. <wwd.com/retail-news>

- NexCen Brands, Inc. announced on Monday the opening of the first Shoebox New York franchised store in the Middle East - The store is in 360° Mall in South Surra, Kuwait. The store came out of an agreement NexCen signed with developer Khalid Al-Mutawa in February. The agreement stipulates the opening of three Shoebox franchises over a 10-year period. Al-Mutawa also owns the development rights to another NexCen store, TAF, in Kuwait, Jordan and Egypt. TAF, formerly known as The Athlete’s Foot, has opened up 11 stores in Kuwait since 1997 under Al-Mutawa’s guidance. The Shoebox opening marks NexCen’s continuing push to develop more stores in the Middle East in Africa. Last month, the company opened a TAF store in Botswana, with plans for more stores in that region over the next decade. <wwd.com/footwear-news>

- Exports of Swiss watches fell 31.9% in June - Swiss watch exports experience the steepest fall since the beginning of 2009, reflecting wilting demand for expensive timepieces amid the economic crisis. In the first half of 2009, total watch exports showed a 26.4 percent decline, totaling 6.1 billion francs, or $5.7 billion at average exchange rates. The Swiss watch industry has been in decline since the end of 2008, after five years of strong growth, with exports currently below 2006 levels. In general, wristwatches selling for more than 500 francs, or $466, experienced the most severe declines. Products worth between 200 francs, or $186, and 500 francs were the least affected, with a fall restricted to around 10 percent. Pasted from <wwd.com/business-news>

- More confirmation of apparel manufacturing returning to normal in Bangladesh after labor unrest - Bangladesh's apparel manufacturing industry has seen recovery from the labor unrest, arson attacks and vandalism last month that left two workers dead and hundreds of people injured. The unrest has destroyed the factory of the country's leading apparel manufacturer Ha-Meem, whose customers include American Eagle Outfitters, Gap, J.C. Penney, Target and Wal-Mart. Despite the aftermath of the violence and the continued layoff and wage cut, manufacturers said most of the production and export business are returning back to normal. <fashionnetasia.com/industryupdate>

- The Indian government has allocated land to build a spun silk mill -The Andhra Pradesh government has decided to allocate 334.9 acres of land to build an industrial park in Visakhapatnam and 6 acres to develop a spun silk mill in the Anantpur district. The government ratified the earlier decision of the Commissioner of Sericulture that sanctioned 3 acres of land to give an additional 3 acres of land for a lease period of 10 years. The spun silk mill project is the first of its kind in the country and is expected to provide employment to many farmers along with helping them to increase their income. The cabinet also decided to extend by three years the Rs 50 crore government guarantees extended to the AP State Cooperative Bank towards providing the Weavers Cooperative Society (APCO) with cash credit facilities. <fashionnetasia.com/industryupdate>

- Nepal Handicrafts Association criticized government on newly announced budget - The Federation of Handicrafts Association (FHAN) in Nepal has criticized the government for not giving the sector any leverage in the newly announced budget. The President of FHAN Shakya said: "Just like the previous budgets, there is no thrust on the export front and it is not possible to only rely on remittances and grants from abroad." He continued: "Malaysia and Thailand had thrived because the country laid an emphasis on the export front rather than countries like Bangladesh and Philippines which chose to depend on remittances from their nationals". <fashionnetasia.com/industryupdate>

RESEARCH EDGE PORTFOLIO: (Comments by Keith McCullough): WMT

07/20/2009 03:14 PM

BUYING WMT $48.73

WalMart breaking out above its immediate term TRADE line of $48.43, finally. Downshifting your beta at the top end of a market move is the right risk management call. KM

INSIDER TRADING ACTIVITY:

NKE:

- Charles Denson, President-Nike Brand, sold 5,062shs ($XX) less than 20% of common holdings pursuant to 10b5-1 plan.

- Mark Parker, President & CEO, sold 8,579shs ($XX) less than 5% of common holdings pursuant to 10b5-1 plan.

- David Ayre, VP, sold 3,533shs ($XX) approximately 23% of common holdings pursuant to 10b5-1 plan.

JCG: David House, Director, sold 1,749shs ($48k) after exercising the right to buy 1,749shs ~30% of common holdings.

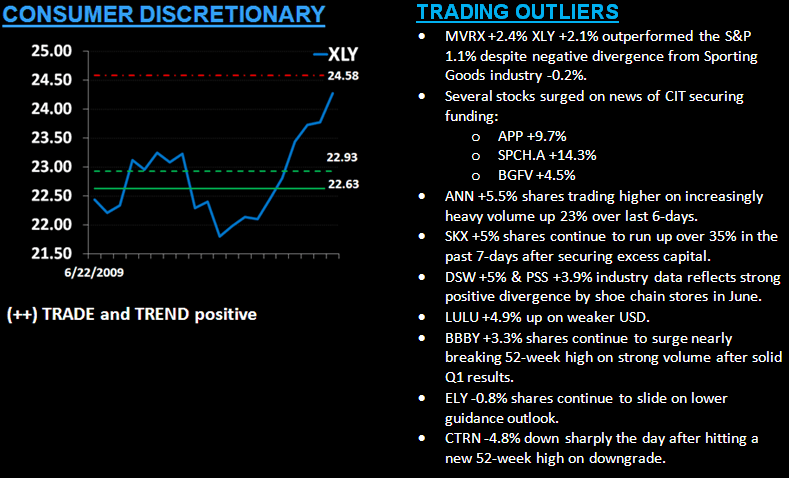

MACRO SECTOR VIEW AND TRADING CALL OUTS