“Boom, crush. Night, losers. Winning, duh.”

-Charlie Sheen

I was in Vegas playing cards with Sheen last night and that’s what he told me about his short Facebook (FB) position. Social Media Bubble, yep. Crushing it.

I’m here to give the keynote rant today (11AM Las Vegas time) at the Government Investment Officers Association (GIOA) conference. Kidding on the Sheen part; not on the government.

USA going on the fritz (Federal Reserve Induced Trauma Zone) won’t be the subject of my speech. I’m going to give these guys the Hedgeye wood - #InflationAccelerating slows real US growth.

Back to the Global Macro Grind…

I know no one wants to call it a bubble. There’s career risk in calling something what it is. But seriously mo bros, with Facebook (FB) -17% since March 10th (coincided with the all-time-bubble-high in US stocks) and Twitter (TWTR) -30% YTD, what’s the fuss?

BREAKING: Candy Crush (KING) -15.6% on IPO day

Boom! Crush. This stuff gets real in a hurry doesn’t it? But does the whole free world care? While 2AM PST isn’t my favorite wakeup call on The Strip, I did smile to see that almost all of Asian and European Equity markets didn’t care about USA’s baggage.

Baggage?

Yes, after creating the 1st internet bubble (1999), then the US real estate bubble (2005-2006), then the commodity bubble (2011-2012)… then the bond bubble (2011-2012), then the 2nd half-baked internet bubble (2013), this is a uniquely American experience.

Maybe that’s why (in spite of the social media stock time-spanking into the close yesterday):

- South Korean Stocks (KOSPI) built on yesterday’s gains, closing +0.7%

- Indian Stocks (BSE Sensex) closed up another +0.3% to +4.7% YTD

- Italian Stocks (MIB Index) are trading up small this morning at +11.5% YTD

I know. The Italians have a lot of crony socialism issues, but one of them is not trying to talk their entire country into calling $2B for a headset (Ocular) another brilliant Zuckerberg idea. WhatsApp was a cool Bud Light commercial for a few weeks too don’t forget.

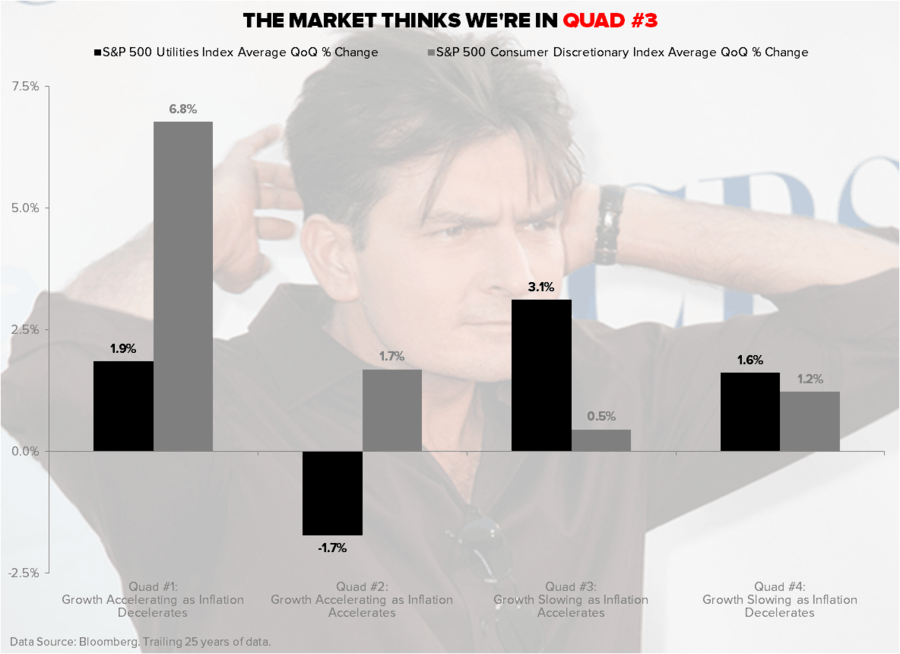

Back to the real world and our GIP model (Growth, Inflation, Policy):

- US continues to see #InflationAccelerating (CRB Commodities Index up again yesterday to +7.6% YTD)

- And the slope (rate of change) in real US Growth continues to slow (not just the weather)

But don’t take my word for it, ask the bond market:

- US 10yr Treasury Yields down again this week to 2.70%

- Yield Spread (10yr minus 2yr) continues to compress (-7bps this wk)

This is precisely what happened in 2011. As the Yield Spread compressed (leading indicator for growth slowing) the Financials (XLF) started to underperform slow-growth-yield-chasing (Utilities) and the US stock market saw multiple compression.

In other words, if you weren’t levered long YELP yesterday, but had:

- Commodities long

- Bonds long

- Anything that looks like a bond (Utilities, REITS, etc.) long

You crushed it.

Yeah, I know. We have you long Gold, and that’s not working this week. At -0.7% this morning, it’s still +7.7% YTD though. Beats Twitter. And it sure beats being long who gets crushed by inflation (US Consumers):

- US Consumer Discretionary Stocks (XLY) -4.1% YTD

- Utilities (XLU) +7.0% YTD

These performance divergences are called variance. And finally we have ourselves an Angry Bird like game here folks – where stuff actually goes down (hard), while other things stay up.

Coming off generational lows in US sector variance (i.e. you could have bought any sector and been up last yr), across longer-term investing cycles, this is as mean reverting as any portfolio risk in macro. Yep, sector and stock picking is cool again.

So, from here, do you buy the Candy Crusher or the new banking fees boy king at FB? Or do you do neither and go back to buying the Bernanke Bubbles (Commodities, Gold, Bonds) that blew up last year? We’ll do the latter. Mean reversion bubble trading works, duh.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.63-2.75%

SPX 1

VIX 13.03-17.14

USD 79.18-80.40

Pound 1.65-1.67

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer