PNRA remains on the Hedgeye Best Ideas list as a SHORT.

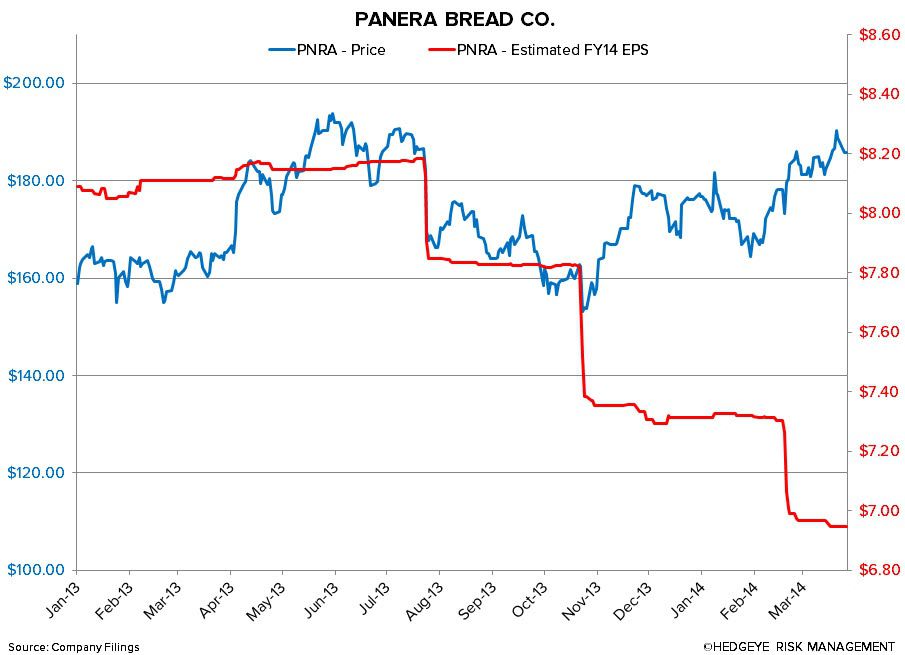

Following Panera’s Investor Day, we have upped our conviction in PNRA as a high quality short. Since the end of January, the stock has largely traded off of overly optimistic expectations, rallying more than 12% in anticipation of the event. However, after revealing a more sober financial outlook than most anticipated, the stock should sell off on reset expectations.

Panera announced a number of initiatives yesterday, many of which we liked. These, ultimately, will lead to the culmination of a new to-go experience, a new eat-in experience, and a new catering business:

- The new to-go experience will allow customers to order in the store or in advance on their mobile phones, leverage the MyPanera app (saved favorites, customization, rewards), and establish a specific time for pickup.

- The new eat-in experience will incorporate fast line kiosks from which the customer can order and pay, before sitting down at a table and having their food served to them.

- The new catering experience will run out of delivery hubs, which will enhance café capacity and focus and allow for both small and large order delivery.

It is Panera’s goal to thrive in a digital future and we believe they have an innovative, feasible plan in place to deliver on this. With that being said, these initiatives require significant investment which likely means that 2014 and 2015 will be nothing more than investment years. As management reiterated time and time again, they are positioning themselves to drive long-term success which means that there will be some near-term pain.

We remain bearish on Panera for the following reasons:

- No guidance – Management reiterated 2014 guidance but would not provide any guidance for 2015. This lack of visibility is concerning, but understandable. Management simply doesn’t know what to expect. The majority of Panera 2.0 will not be rolled out until the end of 2015, meaning it will likely be another significant, margin compressing investment year.

- Conscious cannibalization – This is a phrase we never like to hear management teams use. This, to us, is an indication of market maturity and while we understand the concept of growing units and overall sales, we never like to see this done at the expense of another store. Growing at lower returns is always a red flag.

- Low returns – Among the P&L implications for Panera 2.0 are increased labor and training, higher credit card usage, fees related to IT, and depreciation, all of which will have a dampening effect on margins. Management would not commit to higher margins post the rollout.

Considering the bulk of the investment will come in 2015, we believe it is unlikely Panera will be able to deliver the 18% earnings growth the street is expecting. After a prolonged disconnect, we expect the stock to begin reflecting the fundamentals as the street comes back to reality.

Recent Notes

12/19/13 Best Idea Update: Short PNRA

10/23/13 PNRA: The Pace Of Change?

10/21/13 PNRA: Stage 1 Denial

09/26/13 PNRA: No Quick-Fix Recipe

07/23/13 PNRA: Short Thesis Playing Out As Expected, Part II

04/24/13 PNRA: Short Thesis Playing Out As Expected

04/05/13 PNRA Hype Makes It Shortable

03/26/13 PNRA Happy Camper Facing QSR Wounded Bears

02/15/13 PNRA Mix Tapped Out?

01/30/13 PNRA Bread Not Quite Baked

Howard Penney

Managing Director

Fred Masotta

Analyst