Editor's Note: This research note was originally published March 20, 2014 by Hedgeye’s Restaurant Team. For more information on Hedgeye please click here.

The Bureau of Labor Statistics released its Consumer Price Index data for the month of February last week. Despite a marginal improvement in the Restaurant Value Spread during the month, food away from home continues to be notably more expensive than food at home. This suggests that cost sensitive consumers are more likely to frequent the grocery store and prepare their own food than they are to visit a restaurant and dine out.

The value spread did, however, narrow sequentially by 30 bps in February to -1.3% as food at home inflation accelerated at a faster rate than food away from home inflation. Therefore, we’d surmise that eating out did become marginally more attractive over the course of the month. Overall, we view the release as less bearish, on the margin, for the restaurant industry.

Full-service and limited-service prices grew +2.3% and +2.2% YoY, suggesting that fast casual and QSR restaurants are becoming more attractive, on the margin, than casual dining restaurants to cash-strapped consumers.

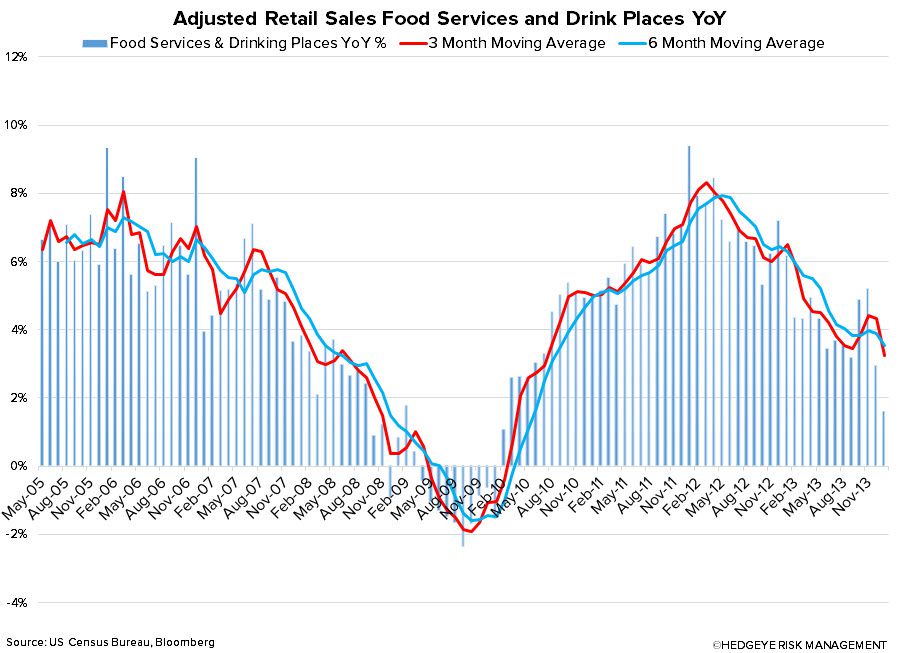

Overall, retail grocery sales and food services sales data continue to support our thesis regarding the negative Restaurant Value Spread, as grocery sales continue to increase on a YoY basis at the expense of food services sales.