This note was originally published at 8am on March 11, 2014 for Hedgeye subscribers.

“The life and light of a nation are inseparable.”

-James A. Garfield

That’s the opening quote to a fantastic US #history book I cracked open this past weekend: Destiny of The Republic – A Tale of Madness, Medicine, and the Murder of a US President, by Candice Millard of Kansas City, Missouri.

After serving only 200 days as President of the United States (MAR-SEP of 1881), Garfield was shot by a whacko loser by the name of Charles Guiteau. Not unlike many of us, Garfield never thought of himself as part of a “class.” While he was raised poor, he empowered himself with the light of self-education. He was one of the smartest Presidents America has ever had.

Being “smart” isn’t a big differentiator in this profession. On paper, I don’t really know anyone who is dumb. But thinking that an un-elected-central-planning-bureau can smooth our economic lives and provide us with a pre-18th century enlightenment is. While hope is not a risk management process, that’s all I have left that America’s currency finds her footing.

Back to the Global Macro Grind…

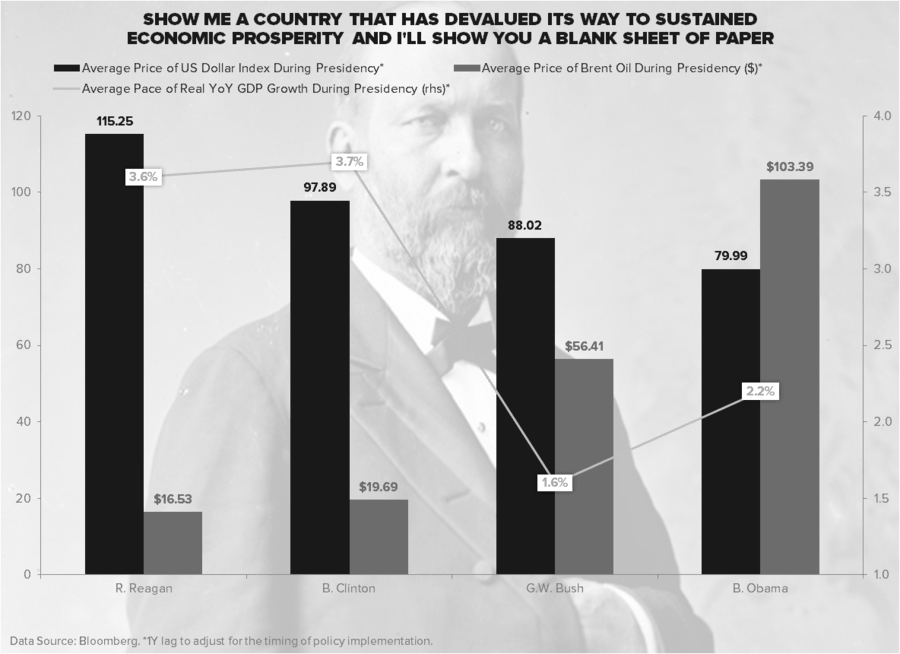

As I alluded to in yesterday’s Early Look, 1870-1913 was one of the best economic periods in American history for a reason. The US understood the value of owning what was becoming the world’s reserve currency. There was no Federal Reserve to devalue it.

Fast forward 100 years, and we have ourselves quite a scene to observe in global macro markets every day. Places like Argentina (who had the same standard of living as the US in 1920), missed having Presidential periods of sustained real (inflation adjusted) economic growth like 1983-1989 (Reagan) and 1993-1999 (Clinton) where the value of America’s currency rose with interest rates.

Our Global Macro Theme of 1H13 of #StrongDollar + #RatesRising is gone now. And, on many levels, that’s just a sad thing. It provided for what George Gilder recently coined as “information surprise” in the US economy. It was the life and light that the current @FederalReserve isn’t allowed to understand.

In case you are thinking about moving to another country, here’s what’s headline news around the world this morning:

1. New Zealand’s Prime Minister, John Key, is calling for a new country flag to represent the “end of the colonial era”

2. Swedish Consumers are enjoying #StrongCurrency Tax Cuts (Consumer Prices, CPI, -0.2% y/y for FEB)

3. UK Industrial Production #GrowthAccelerating to +2.9% y/y as the British Pound tests fresh 3yr highs

In other words, there is plenty of life and light in this world. You just have to stop navel-gazing politically in the US and realize that countries are racing against America as she always has against them.

But why do these headlines matter? What do these countries currently have in common?

1. NEW ZEALAND’s #StrongCurrency Policy (the Kiwi) has generated some of the strongest real GDP growth rates in the non-EM world. Consumer Confidence (which tracks the strength of a country’s currency) is testing all-time highs.

2. SWEDEN, while still recovering from its loss to the Canadian hockey team in the Gold medal game @Sochi, continues to reap the rewards of having a currency that can’t be devalued by some Japanese bureaucrat

3. UNITED KINGDOM continues to remind all those who followed in the footsteps of a raging Keynesian policy to devalue the Pound that real-inflation-adjusted economic-growth in the UK has accelerated alongside the purchasing power of its people

Don’t worry, all is not yet lost. But the US stock market’s volume could be. At the all-time highs in the SP500, volume has been as dead as a doornail. In both monetary policy and in market interest (CNBC ratings at all-time lows), the US is starting to emulate Japan. The land of the rising sun and “forward rate guidance” (Japan) saw its stock market volume hit 5 month lows last night too.

What if the life and the light were to just leave? And I mean literally. What if enough of us get what’s going on to simply not show up as the last lemming to buy the all-time bubble high from someone else who doesn’t call the all-time high price bubbly? What if all there is left is the last short seller covering his shorts high after shorting the January lows?

What if?

If, if, then statements aren’t new to evolution. Neither were they new (yesterday) to a part of this world (Latin America) that has tried, tried, and tried again to devalue its currencies as the best path to political power and prosperity.

Argentina, Brazil, Chile (Equities) were all down -1.2-1.6% yesterday as hedge funds continue to race to get net longer of a US stock market they got way too short of only a month ago (-80,000 net short futures/options contracts in Index +E-mini).

Latin American Equities (MSCI Index) are down almost -10% YTD as its people deal with unsustainable debt levels, deficit spending, and failed Policies To Inflate their way out of it via currency devaluation. The purchasing power and currency of The People are inseparable.

Our immediate-term Global Macro Risk Ranges are now as follows (Top 12 Daily Trading Ranges is a separate subscription product):

SPX 1864-1891

Bovespa 44566-47451

USD 79.38-80.11

Pound 1.66-1.68

Brent 106.93-110.61

Gold 1321-1355

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer