Editor's note: This research note was originally published March 20, 2014 at 11:24 in Macro. For more information on how you can subscribe to Hedgeye click here.

"If I see an ending, I can work backwards."

- Arthur Miller

Hedgeye CEO Keith McCullough outlined the thought process behind our view of yesterday’s Fed announcement and the how/why of our subsequent positioning in this morning’s strategy note (Early Look: Fade The Fed's Forecast).

Below we summarily recapitulate that thought process in the context of both our research and risk management views.

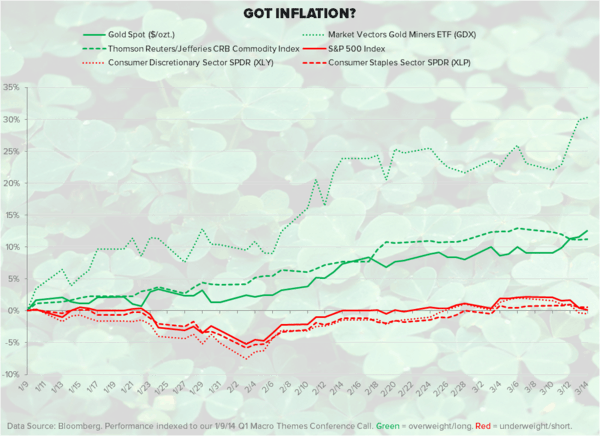

1Q14 Macro View Redux: We became incrementally more bearish on growth at the beginning of 1Q alongside the breakdown in the $USD and 10Y Yields and the breakout in the VIX.

From a positioning perspective, we increased our cash allocation and shifted away from pro-growth consumer leverage towards slower-growth (bonds, gold, slower growth equities, inflation hedge commodities) exposure.

The subsequent and significant deceleration in the preponderance of fundamental macro data served to confirm the price signals.

Recall, we love the pro-growth, factor constellation of #StrongDollar + #RatesRising that characterized most of 2013,

A return to the Dollar Up/Rates Up/Stocks Up regime, confirmed by both the price and research signals, would certainly shift our intermediate term growth outlook upward but the data doesn't support that shift in view here (yet).

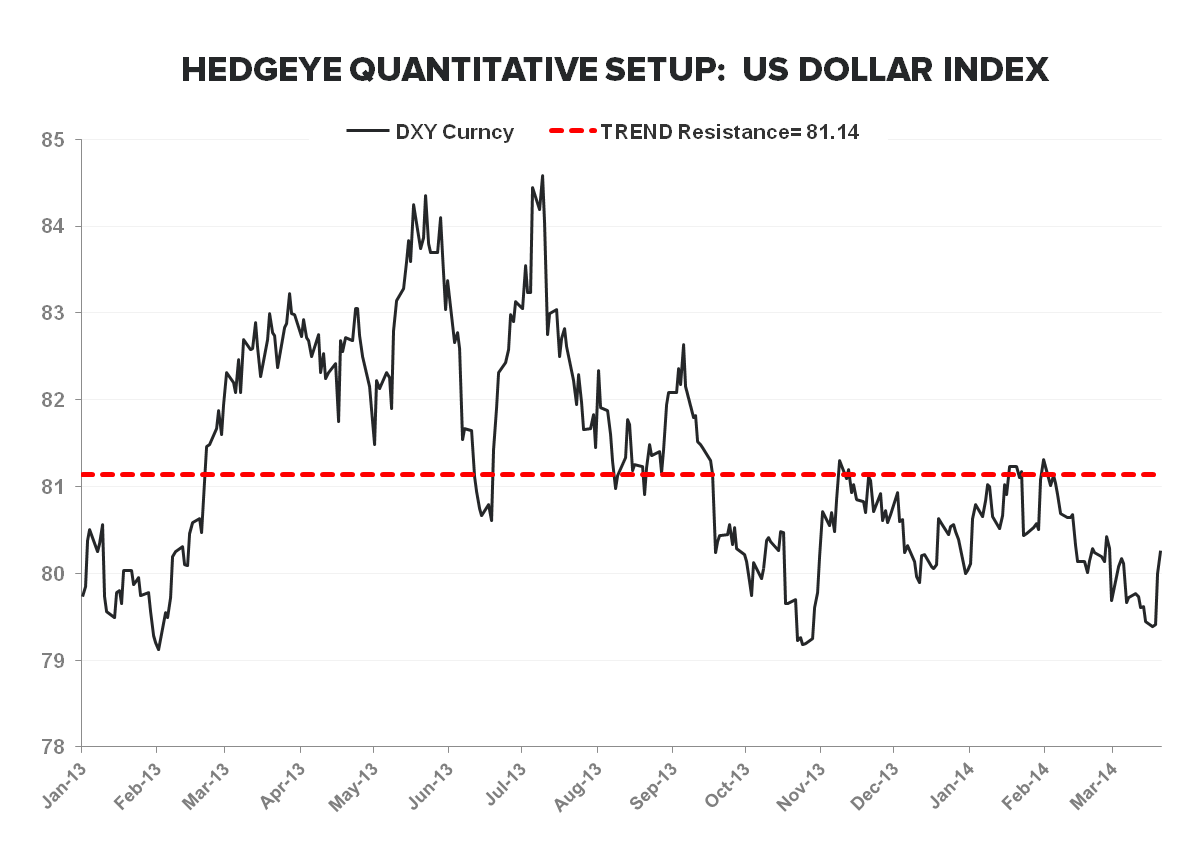

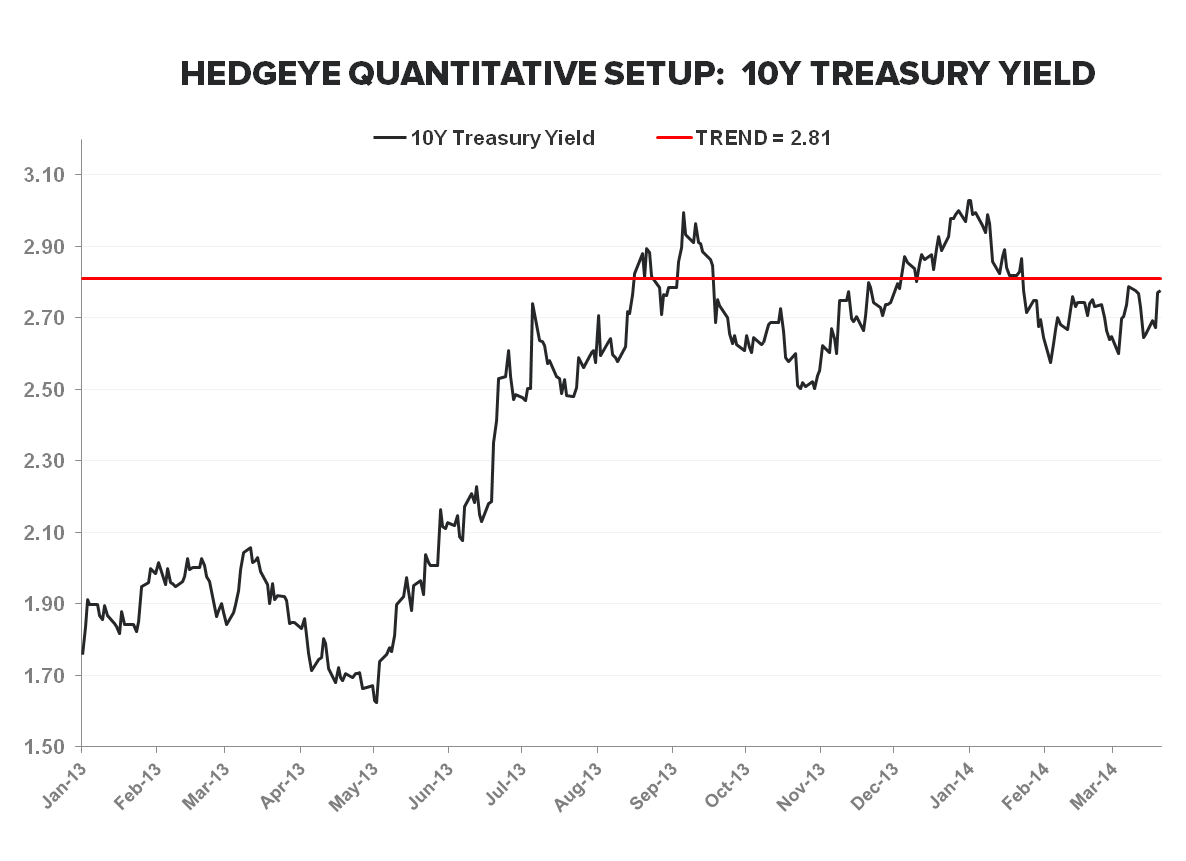

THE RISK MANAGEMENT: Inclusive of yesterday’s price action, the $USD and 10Y Yields remain broken Trend while the VIX and Gold remain bullish on a Trend basis.

In the context of our view of the Risk Management Signal as a leading indicator of fundamentals, from a quantitative perspective, we’d need to see the following occur for us to get back behind the growth trade

- US Dollar Index breaks out > $81.14 TREND resistance

- US 10yr Yield breaks out > 2.81% TREND resistance

- Gold snaps $1278 TREND support

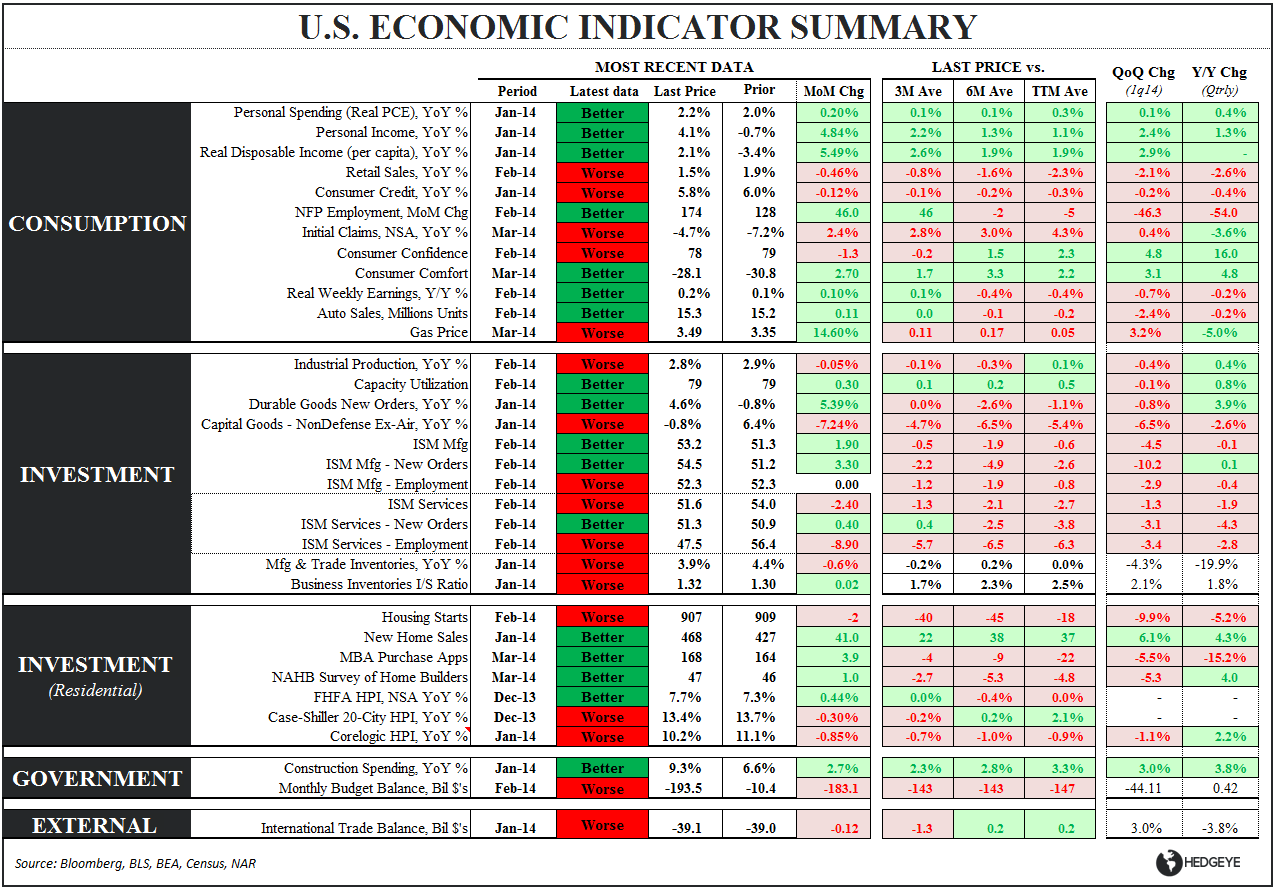

THE FUNDAMENTAL: The fundamental data decelerated materially in 1Q14. We saw some multi-decade/record sequential drops in various ISM sub-indices (for example) and while the weather did have some impact, we’d argue the slope of growth was negative vs 2H13 levels even if you discount for the weather distortion.

Indeed, it’s likely we get a post-weather distortion bounce in the reported data over the next couple months – the question, however, will be whether we can recover to a positive slope of growth from a trend perspective.

Growth math, after all, is geometric – you have to go up more than you went down on a percentage basis to get back to breakeven.

In the context of the summary table below, we expect the “latest data” column to improve from the homogenous sea of “Worse” that existed in February to a more heterogenous mix of “Better”/”Worse” as we comp exaggerated Jan/Feb declines.

From a fundamental perspective, we’ll be looking for the TREND data (3M/6M/TTM Ave) to reflect a re-acceleration.

THE COMPS: In short, the comp setup gets progressively tougher for two more quarters as Growth Comps get increasingly difficult while inflation comps ease into 3Q14.

At the least, progressively harder top line comparisons alongside increasingly harder margin comparisons is a comp dynamic to be wary of on the long side – particularly when both the quant and fundamental data aren’t yet confirming the pro-growth call.

THE PLAN IS THE PLAN WILL CHANGE: The above highlights the summary output of our integrated research-risk management process post the hawkish lean out of Yellen et al.

The process isn’t perfect, but it’s dynamic, quantified and repeatable and its happened to work a good deal more than not over the last 6 years.

Of course, the process also dictates we change our view/positioning alongside the collective change in the price signals and fundamental data. The above outlines the primary metrics and levels we’ll be using to manage our exposure from here.

Fascinating and frustrating, but definitely not boring.

Current Positioning: 15 Longs, 5 Shorts

Christian B. Drake

cdrake@hedgeye.com

@HedgeyeUSA