TODAY’S S&P 500 SET-UP – March 21, 2014

As we look at today's setup for the S&P 500, the range is 35 points or 1.12% downside to 1851 and 0.75% upside to 1886.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.34 from 2.35

- VIX closed at 14.52 1 day percent change of -3.97%

MACRO DATA POINTS (Bloomberg Estimates):

- 11:45am: Fed’s Bullard speaks on panel in Washington

- 1pm: Baker Hughes rig count

- 1:45pm: Fed’s Fisher speaks in London

- 4:30pm: Fed’s Kocherlakota speaks in Washington

- 7:20pm: Fed’s Stein speaks in Washington

GOVERNMENT:

- House, Senate out of session

- 8am: Moniz speaks with reporters, analysts at BGOV breakfast

- 8:30am: SEC Chairman Mary Jo White, FCC Chairman Tom Wheeler speak at Consumer Federation of America assembly

- 10am: Vice President Joe Biden speaks at National Assn of Community Health Centers’ policy forum

WHAT TO WATCH:

- Gunvor co-founder exits ownership stake as U.S. sanctions hit

- Sanctioned Bank Rossiya says MasterCard, Visa halt service

- Banks’ split with Fed on stress may risk shareholder payouts

- Volcker rule seen costing banks as much as $4.3b: OCC

- JNJ, Takeda, Roche may receive EMA decisions

- U.S. keeps AAA rating by Fitch as outlook raised on debt pact

- Malaysia jet’s steady flight has Australia scouring ocean

- No positive news yet from satellite search for jet: Malaysia

- Families seek truth after evasive responses from airline

- Netflix CEO calls for stronger rules on web traffic handling

- Nike sees weaker-than-expected sales gain after profit beat

- Macondo partner Anadarko’s e-mails seen showing role in well

- Dow, Eastman Chem. back group airing ads to protect senators

- Chrysler truck sales rise vs those of GM, Ford, WSJ says

- Obama in Europe, Stress Tests, Microsoft: Week Ahead March 22-29

EARNINGS:

- Darden Restaurants (DRI) 7am, $0.88

- Tiffany & Co. (TIF) 6:59am, $1.52 - Preview

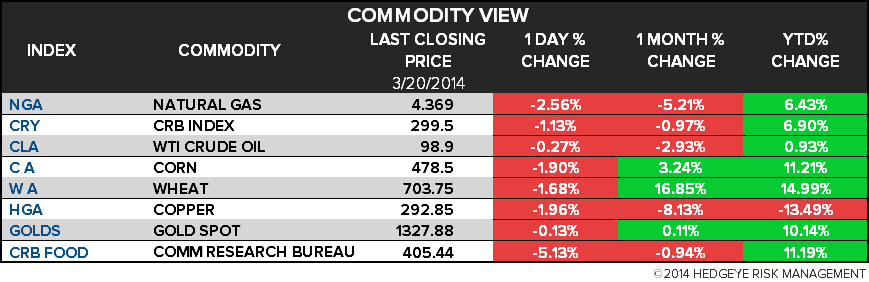

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Rises to Trim Weekly Decline as Price Drop Spurs Demand

- Palm Output in Indonesia Climbing for First Time in Six Months

- Coffee Belt in Vietnam Poised for Rains Easing Threat of Drought

- Gold Trims Weekly Decline as Ukraine Crisis Spurs Haven Demand

- Brent Set for Fourth Weekly Loss Amid Russia Clash; WTI Rises

- Canada’s Grain Backlog Seen Persisting With More Oil Shipments

- Palm Heads for Second Weekly Loss as Indonesian Output Increases

- Global Energy Thirst Threatens to Worsen Water Scarcity, UN Says

- Wheat Trims Weekly Advance as Dollar Rally Seen Curbing Demand

- Hot-Rolled Coil Futures Debut in Shanghai to Complement Rebar

- Baoshan Is Top Steel Stock on China Car Demand: Chart of the Day

- Russia Senate Clears Crimea Annexation as EU Boosts Ukraine Ties

- Copper Traders Are Bullish on Speculation Prices Slumped Too Far

- Copper Advances to Trim Weekly Decline: LME Preview

- WTI Oil Seen Dropping in Survey on Rising U.S. Crude Supplies

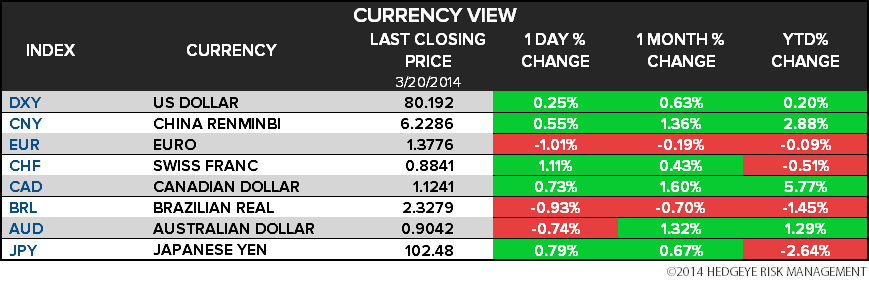

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

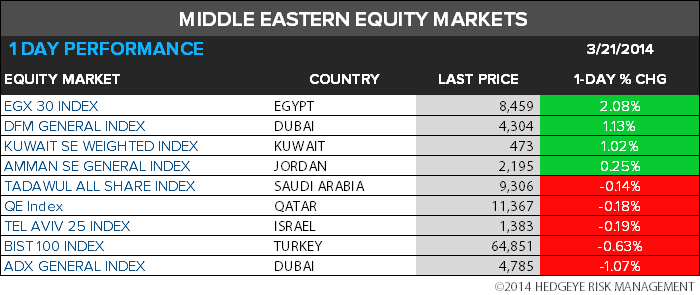

MIDDLE EAST

The Hedgeye Macro Team