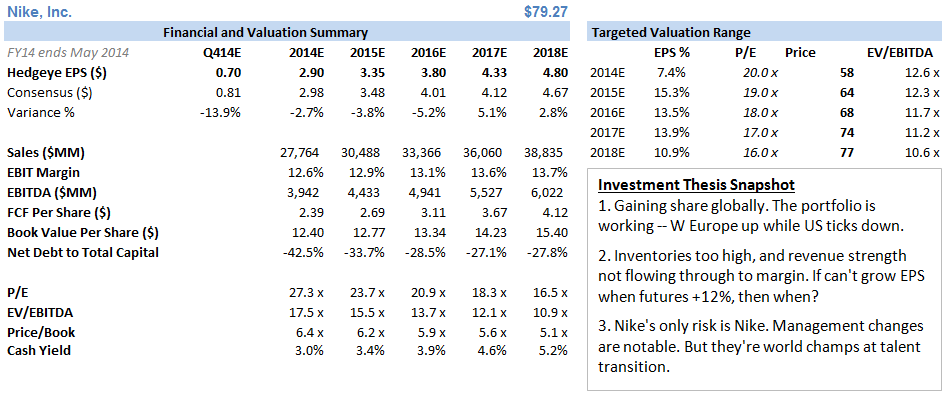

Conclusion: We don’t have any major changes to our thesis in the wake of Nike’s 3Q14 print – we don’t think it’s an outright short, but we simply can’t get comfortable with the risk/reward here. We expected a good quarter (see prior comments below), but did not like the lack of any room for error in this financial and operating model. And that’s pretty much what we got. The top line and order book both continue to show the tremendous Brand Heat that we've grown to both expect and admire. But with 13% growth in revenue, Nike only put up 4% EPS growth, and half of that came below the line. Looking ahead, the Street is expecting a 7.3% EPS growth rate in 4Q, but even after fronting Nike the high end of its sales and gross margin forecast, we get to $360mm of incremental Gross Profit – not bad at 12% growth vs. last year. The problem is that Nike is spending an incremental $400mm in SG&A. That puts it in the hole for $40mm. Add on another $40mm in incremental FX impact, and we’re looking at a 9% decline in EPS. We ‘get it’ that there are Macroeconomic crosscurrents that are hurting everyone – not just Nike. In that context, it’s growth should be commended. But if they can’t grow EPS at a Nike-esque 20% rate when futures are six months into a double-digit growth rate, then when will it happen? That’s a pretty good example of what we mean by minimal room for error in the model – particularly when it’s trading at 23x earnings.

Here’s a few other points that stood out for us:

- The Portfolio: We’ve got to give big props to Nike on this one… One of our concerns was that a potential slowdown in the US would leave the top line exposed given that other regions were not carrying their weight. Well…this quarter North America futures slowed to the single digits (9% -- vs. 11%-12% over the past four quarters). That’s not the end of the world as it’s easing to a range (about 6-8%) where it should be long term. But it slowed nonetheless. The great news – and something we did not see coming – is that Western Europe futures were up 33%. That’s the biggest number we can find on record. Western Europe is the second largest region for Nike – accounting for about 20% of cash flow. This is exactly what we want to see – when one region dips, another picks up the slack. (Though we like to see some flow-through to the bottom line as well – and that we did not see).

- China: China futures were down for the first time in forever (we think). The good news is that the strength in Western Europe took some of the pressure off China to perform in light of the downtick in the US. But what surprised us is that the company really did not dedicate much time to China on the call. Trevor Edwards (Nike Brand President) glossed right over it. Don Blair came to the rescue with some information about the disconnect between futures and revenue growth. But in the end it did not come across that the company has a concrete plan for reaccelerating growth in its most important country outside America.

- Futures v Revenue. We’re looking at a robust 12% futures growth rate headed into Nike’s fourth quarter. That was above expectations by 1-2 points. But the problem is that the company took down revenue guidance for 4Q from ‘low double digit’ to ‘high single digit’. They chalked it up to fewer expected closeout sales, which is surprising because inventories are up 15% to $3.8bn -- the biggest inventory increase Nike has seen in almost two years. In fairness, the company took up its Gross Margin guidance, which bolsters the case for fewer low-margin closeouts. But the reduction in top line guidance absent a slowdown in futures is simply odd for Nike.

- 2015: The company guided to a growth rate in EPS below its ‘mid-teens’ long term model. We’re not sure how much of that we believe. Nike has its own little biorhythm, and the Street usually feels the brunt of it about this time of year. The company is about to solidify financial targets for each business over the next 1-2 months. More often than not division heads will find tangible reasons as to why they cannot grow their business, just to give that ammo to the executive team. That way, low expectations are set, which also happens to be the hurdle by which people get paid. If you run a business at Nike and manage to convince your boss that your business can only grow 5%, and yet you end up growing 15%, you’re going to have a great payday.

HERE’S OUR NOTE FROM EARLIER THIS WEEK

3/19/14

NKE: Good Qtr, Bad Risk Profile

Takeaway: NKE at $70 had everything going right. Near $80 it’s all about top line. No room for error. Good Q, but we just don’t like the risk profile.

We don’t have a strong opinion on NKE headed into its print on Thursday, which is a rarity for us. As background we turned somewhat cautious on Nike coming out of last quarter for a couple of reasons.

- First is that we’re still not sold on the management transition at the company. We don’t like the circumstances that led up to the changes, and we’re not convinced that the right people are in the right places. That’s a bold statement in that Nike is all about people. And it’s success over the years has been driven by consistently putting the right people in the right roles. Some recent moves are a slam dunk (like putting Eric Sprunk in charge of operations), but others are not. We fully acknowledge an important point – that our opinion on who is doing what inside Nike is not very relevant. The opinion that matters is that of the employees who have acclimated to their new bosses. And our concern is that, at least by our measure, THEY don't seem to be as sold on the new management team anywhere near the extent that they were a year ago. Another thing we acknowledge is that management transitions in a company as big and complex as Nike take years to play out – either good or bad. None of our concerns will manifest in any way as soon as this quarter. But we remain concerned about solidarity throughout the organization.

- The second, and more pressing (near term) reason is that the Nike story six months ago had three massive pillars of support; 1) Severe Brand heat – with futures and revenue both accelerating, 2) Improving Gross Margins, and 3) Slowing inventory growth. That’s a trifecta that makes Nike pretty much bullet proof. But today, we have a) Gross Margins turning from a tailwind to a headwind, and b) Inventories growing above the rate of sales. In effect, it lost two of its three pillars of support. The positive is that the Brand is still on fire – both here and in Europe. That’s the most important pillar, thankfully. But there’s no question that the margin of error for Nike is dramatically tighter now than it was heading into last Fall.

So we’re looking at one longer-term concern – that won’t play out now – and a near-term concern that will likely be masked by the fact that revenue momentum remains so strong. And let’s face it, there’s not a long list of companies that are clobbering the competition like Nike is today – so on a relative basis, which is where many investors live, this one ain’t too shabby. So in the end, this will likely be a decent-enough print. But in the fall when NKE was a $70 stock it had everything going its way. Now it’s nearly an $80 stock, only one thing is going its way, and not much else can go wrong. We just don’t like the risk profile.

Here are some questions we have into the quarter:

1) North America vs. The World: Without question, the North American region has been carrying the company for the past two years. Europe kicked in to high gear last quarter and began to shoulder some of the Global Futures growth. That was great to see. That trend needs to sustain itself for Nike to maintain a 10%ish growth rate on the top line. We’d really like to see better consistency out of Emerging Markets (though we guess that once they’re consistent, they will no longer be ‘emerging’) and a meaningful step-up in China.

2) Gross Margins: We know that the company is facing input cost pressures, but the way we see it cost pressures were easing (mostly over the past year) and at the same time the company had a great two-year run in taking up price in footwear. Can it take up price further to offset the higher raw materials, or will they have to ‘eat it’ for another three quarters while raw materials go against them? Inflation is definitely not going down.

3)SG&A Spending: Very rarely have we EVERY questioned Nike on SG&A spend. The reality is that – despite splurges when it was in its younger days – Nike has grown up to be an extremely reliable and proficient steward of capital. But we question the recent signing of Jonny Manziel, who is taking home a reported $20mm annually. After blowups that Nike had with athletes like Lance, Kobe, and even the (once) squeaky clean Tiger Woods, we’re surprised that it is rolling the dice on someone that is not particularly likable and poses significant ‘blow-up risk’. Nike prides itself in paying up for what it calls ‘crossover athletes’ meaning that they could be on the cover of Sports Illustrated and Vogue/GQ in the same month. Not quite sure that Manziel is that kind of guy. While that might be nitpicking on one small asset in the context of a company that has $3.6bn in minimum obligations against endorsement deals in the coming 5-years, we should also note the recent deal with Manchester United. The company recently re-upped its 10-year ManU deal at a premium that stunned us. The company had been spending £23mm annually – an amount that now goes up to £60mm. We could understand if the team became meaningfully stronger in recent years, but unfortunately the reverse has happened. Nike is paying nearly 3x for a lesser team. Hopefully there are parts of this deal that we are not privy to that justifies the expense. We certainly hope that Nike will elaborate on both on the call.

4) FlyKnit – Changing the Conversation: As cool as the FlyKnit kicks are, we want to start hearing more about a few things a) unit cost savings per pair (which they won’t provide because then they’ll tell retailers what their real cost is), b) how much Nike saves in inventory costs (raw materials) for a pair of FlyKnits vs. traditionally-manufactured footwear, and c) when the production technology will be ready to roll out at retail, so consumers could order FlyKnit NikeID product in a store, then go get a burrito at the foodcourt, and come back an hour later and the product is created, fully customized, and ready to take home. Once they nail down that capability (something they’ve quietly been working on for four years) we’ll drop every concern we have about this name and pound the table faster than you can say ‘Prefontaine’.

5) Jordan Running: Nike is launching its first running shoe for the Jordan line on May 1. It’s about time…you can buy a Jordan basketball shoe, baseball cleat, football cleat, and golf shoe. Yet not for the largest shoe category of all – running? This is one of the biggest lay-up (no pun intended) opportunities for the Jordan brand we’ve seen in a decade. We’re interested in management’s plans here.

6) Dot.Com: For one of the most powerful brands in the world, Nike has one of the lowest dot.com ratios at about 4%. Granted, part of the reason Nike’s Direct business is half the size of UnderArmour’s (as a percent of total) is that its wholesale model is so incredibly powerful. But Nike needs to do a better job articulating its dot.com strategy.