Here's the fourth note in a series of five in advance of our LULU Consumer Survey results on Monday March 24th at 11am ET. When we polled consumers three months ago, we pulled away some clear insights. The concerns largely outweighed the strengths, which foreshadowed the company's results, and ultimately the stock price.

We're re-running our survey to gauge the incremental change over the past quarter, with the goal of seeing whether LULU is making progress (which could get us more constructive on the name) or not.

In preparation for 'Round 2' we want to offer up some of the notable takeaways from our last survey, as they'll be framing the discussion on Monday.

'LIKELY TO RECOMMEND'

We asked consumers which Yoga brands they are likely to recommend to friends. The highest scores were Sweaty Betty, Prana, Nike, UnderArmour and Idealogy (Macy's). At the other end of the spectrum, unfortunately, was Lululemon, Old Navy, Puma and Roxy. Definitely a problem for LULU -- one that few people, even the company, are likely to debate.

On the flip side, we asked which brands are highest on the list of brands that you are UNLIKELY to recommend to friends. This is slightly different than the inverse of the first question, as it looks to measure negativity as opposed to lack of positivity. But the results are the same in that Lululemon scored higher than any other brand on the 'unlikely to recommend' scale. Other notables include Old Navy and VS/Pink.

WHY NOT PURCHASING

Next we asked the people who have never purchased anything at Lululemon why they don't shop there (this was about 30% of our sample). The primary factor is that there are no stores in their area -- which is actually a bullish factor for LULU. That speaks to the square footage growth opportunity for the company. The next factor -- and only other one that registered at a notable level -- is that prices are too high. We discount this to some degree, as certain people in the sample simply might not be able to afford high end Yoga apparel.

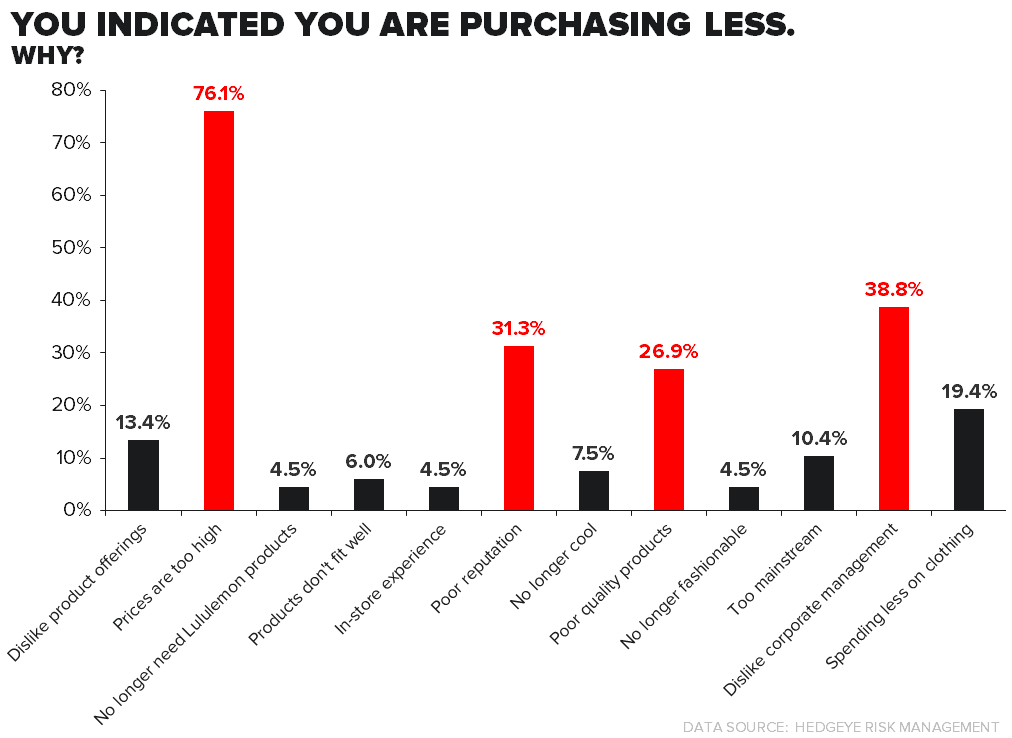

WHY PURCHASING LESS

More interesting to us is the rationale people who are purchasing less product than they used to gave as to their altered purchasing habits. This one was interesting.

The top answer -- by a country mile -- is that the prices are too high. In fact 76% of the people in this group said so. Importantly, they are preexisting customers of LULU, so you can't just say that they can't afford it. The reality is that at one point price was not a factor, but three months ago, it was.

#2 answer = Dislike Corporate Management. Seriously, have you ever heard Main Street talk about not liking a corporate management team? Wall Street says it all the time, but for this to be an issue with Main Street it has to be really bad.

#3 answer = Poor Reputation. Again, this is likely a function of LULU's self-inflicted wounds. It had nothing but a stellar reputation 13 months ago.

#4 answer = Poor Quality Products. We're the first to admit that Lululemon's product -- generally speaking -- is outstanding quality. In fact, that may be an issue for them in that a pair of Yoga pants can literally last 5-years (not good for the replacement cycle). But that's not a bad problem to have. In this case, most of us agree that any ding to LULU's reputation on quality is entirely a function of Luon. We'll see with our next survey on Monday if public perception on this issue is getting a bit more forgiving.