In advance of the release of Round 2 of our LULU Consumer Survey on Monday March 24th at 11:00am, we’ll be revisiting some of the themes that caused us to turn bearish last Fall.

As a reminder, we ran our first iteration of the LULU consumer survey in January. The impetus behind the study was to get a better understanding of how badly LULU's 2013 PR gaffes had damaged the brand. Our surveys are run through a third party vendor to ensure that the results are valid both statistically and methodologically, but we are always looking for data points to challenge our findings.

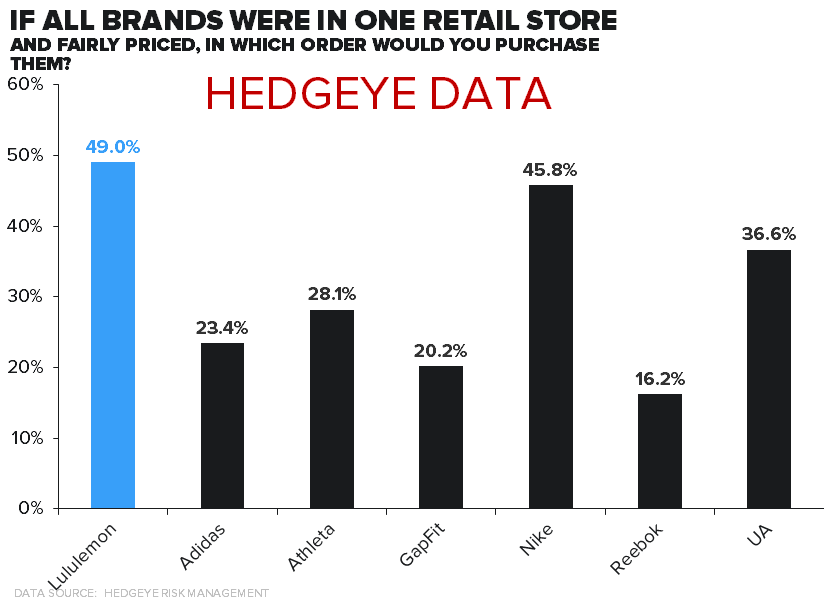

POINT 1:

As background regarding our methodology, we should point out that LULU ran a survey similar to our own soon after Chip's comments and were pretty tight lipped about the findings. At ICR the company flashed one image about brand desirability that we poached and compared to our data set (see both charts below). We won't claim that our data set is a carbon copy to LULU's, but the similarities are telling and lead us to believe that LULU must have been looking at the same troubling trends we called out in January prior to the company's 4Q guide-down.

POINT 2:

We’ll be calling out several items throughout this week. But one that we found particularly noteworthy is that there’s a gross disparity in pricing for LULU vs its’ competitors. Specifically, we asked consumers how much a pair of Yoga pants for each of the 17 brands that we used in our survey. The average price for LULU was $67, versus $45 for the rest of the industry. As you can see in the chart below, no other brand comes close. But when we charted the ACTUAL price of Yoga pants for each brand, we see that LULU is not even the highest, and several brands are within $10 of LULU’s $96 average price. The read-through is that the other pants are not materially more expensive, but consumers just think they are. That’s largely a function of discounting. At other stores, a shopper can find a pair of $90 pants, but get 2 for 1. But LULU has no real discounting strategy. Our sense is that in 2014, we’ll see that happen. Let’s see if the next round of our survey shows any improvement in the perceived value proposition.

More analysis to come tomorrow.