This note was originally published at 8am on March 03, 2014 for Hedgeye subscribers.

“They have a detached-from-reality, academic, floating abstraction form of intelligence.”

-John Allison

While I was flying to LA last night (during the Oscars, because that’s how I roll), that is not a quote about Hollywood. That’s what the former CEO of one of the best banks in American #history said about the Fed’s finest.

“That free markets would make better price decisions than elitist central planners (members of the Federal Reserve) should not be a surprise. Ludwig von Mises proved the futility of central planning in his numerous books, including The Theory of Money and Credit (1913), Socialism (1922), and Human Action (1940).” (The Financial Crisis And The Free Market Cure, pg 34)

If you haven’t objectively studied any of those four books, no worries. Bush, Obama, Bernanke, and Yellen haven’t either.

But you can watch the real-world economics of currencies burning the purchasing power of their peoples this morning in Crimea. I’m hearing that with the Ukrainian currency crashing (-21% YTD), the Ukraine’s stock market being up +43.9% YTD (in burning FX terms) is bullish.

Back to the Global Macro Grind…

In Burning Bucks, the US Stock market was “up for 2014” too – for like 1.5 days. But, after US GDP almost getting cut in half sequentially, and some geopolitical risk pin-action in equity futures today, that will change. Life that is detached from reality generally does, in a hurry.

My inbox is jammed. I can’t count how many emails I received on Friday saying that the “market is up on a GDP slowdown – your research call feels right, but the market doesn’t care”, or something like that…

To be clear, I don’t go with the how markets and GDP “feel” thing. You can overpay to get that from someone else. While the SP500 was up a whopping +0.6% for 2014 YTD (it’s March fyi), it's mainly the inflation and #GrowthSlowing parts of the market leading that:

- Healthcare (XLV) = +7.2%

- Utilities (XLU) = +6.5%

- Basic Materials = +1.9%

The most meaningful parts of the economic cycle (the consumption economy) are actually down YTD:

- Consumer Staples (XLP) = -1.5%

- Financials (XLF) = -0.7%

- Industrials (XLI) = -0.4%

But no worries, as long as you aren’t long anything like Kinder Morgan (KMI, KMP, KMR) in Bernanke’s overvalued Yield Chasing space – or short anything that loves US #Stagflation (like Gold +11.4% YTD), you’re killing it with the whole “market is up” thing.

In other non-Crimean news, US GDP #GrowthSlowing sequentially (from 4.12% in Q313 to 2.37% in Q413) is only the beginning of the Down Dollar (USD down another -0.7% last wk, and down 3 of the last 4 weeks), Down Rates (UST 10yr Yield -38bps YTD) thing.

And, looking at the components of the US GDP report:

- The Deflator (made-up inflation rate) bounce, big time, off its almost 50 yr low

- Government Spending dropped -1.05% sequentially from a GDP contribution perspective

So, the key vectors in the P (Policy) piece of the Hedgeye GIP (Growth, inflation, Policy) model are going to require the US government to:

- MONETARY vector – have the Fed start telling you we need a Policy To Inflate in order to amplify “inequality”

- FISCAL vector – have Obama ramp up deficit spending again in order to pretend to slow the “inequality”

I know, both US monetary and fiscal policy going dovish on the margin is just fantastic. Because, without going to sub 2% US GDP growth and plus 2% made-up-reported-inflation growth, how the heck else could the Keynesians blame Russia?

I’m actually hearing from my contacts in Miami that the Mexicans are going to blame the Russians too. Instead of ripping on US GDP #GrowthSlowing on Friday, Mexico’s stock market dropped to -2.4% on the wk to -9.2% YTD.

Yep, life in Latin America is starting to suck. With the whole deficit-spending-debt-ramp thing, Venezuela and Argentina are reminding people that Latin American stock markets can go down on stagflation too (MSCI LATAM Index -0.1% last wk to -8.1% YTD).

So cheer up – the “market is up.” Away from food and energy prices ripping humanity another new one last week:

- CRB Foodstuffs Index +3.2% to +10.5% YTD

- Oats (I’m probably just a rich guy eating the stuff) +7.1% to +42.2% YTD

- Coffee up another +6.4% w/w to + 59.6% YTD

There’s not a lot to worry about re: the whole #InflationAccelerating thing either… Unless you aren’t detached from reality, of course.

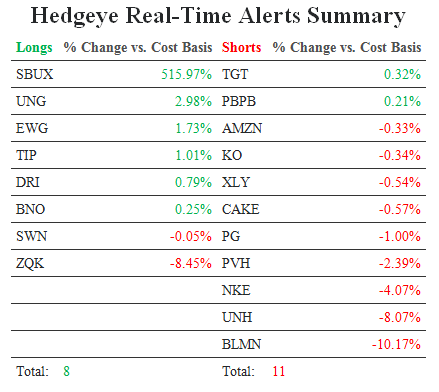

Our immediate-term Risk Ranges are now as follows (our Top 12 macro ranges are in our Daily Trading Range product):

SPX 1825-1861

VIX 13.28-16.99

USD 79.59-80.31

EUR/USD 1.36-1.38

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer