Below are Hedgeye analysts' latest updates on our NINE current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

At the conclusion of this week's edition, we feature three recent research notes we believe offer valuable insight into the market and economy.

***Please note that Brent Oil (BNO) broke our Hedgeye TAIL risk line this week. We are removing it from Investing Ideas until further notice.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

Hedgeye Cartoon of the Week

IDEAS UPDATES

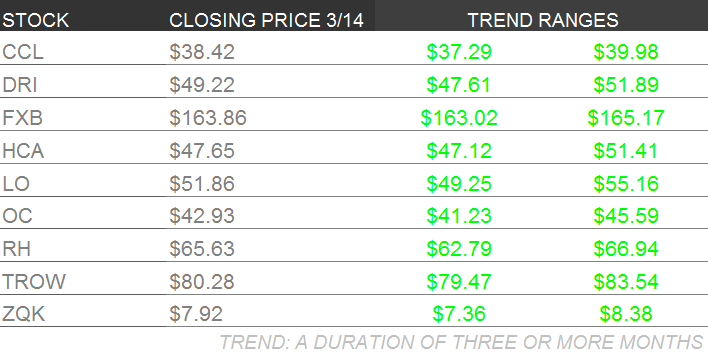

CCL – Cruise Shipping Miami (the largest cruise convention) was held in Miami this past week. While there was not much pertinent news for Carnival, we would point out that there was general optimism regarding Wave Season.

The Ukraine/Russia conflict is of some concern because of Baltic Sea exposure. While the Baltic Sea itineraries account for <10% of Carnival’s European itineraries, it will still sting if CCL is forced to cancel/reroute some of the itineraries.

Bottom line? Keep calm and Carnival will carry on. The next catalyst will be FQ1 earnings in two weeks.

DRI – As it stands, the bear case on Darden is that management will dig in their heels and continue to push forward with their value creation plan. This is a legitimate concern. However, Managing Director Howard Penney thinks it is more than reasonable to assume Starboard will be successful in gathering the appropriate votes to call a Special Meeting and prevent the Red Lobster spinoff.

In a recent research note to subscribers, Penney encouraged independent directors to speak directly with shareholders because, contrary to what management says, there appears to be a widespread lack of support for the company’s current value creation plan. He believes they have a fiduciary obligation to weigh shareholder concerns before making decisions that will materially affect the future’s company.

We continue to like DRI as a long and believe that, with the right plan in place, there is the potential for substantial value creation.

FXB – We remain bullish on the British Pound versus the US Dollar (etf FXB), a position supported over the intermediate term TREND by prudent management of interest rate policy from Mark Carney at the BOE (oriented towards hiking rather than cutting as conditions improve). Last week the Bank maintained the base interest rate at 0.50% along with its asset purchase program target (QE) at £375B.

UK high frequency data continues to offer evidence of emergent strength in the economy, and in many cases the data is outperforming that of its western European peers. This week UK Industrial Production came in strong at 2.9% in January Y/Y vs 1.9% in December and Manufacturing Production bounced to 3.3% vs 1.4% in December.

The British Pound is holding its Bullish Formation, trading above its intermediate term TREND and long term TAIL levels of support.

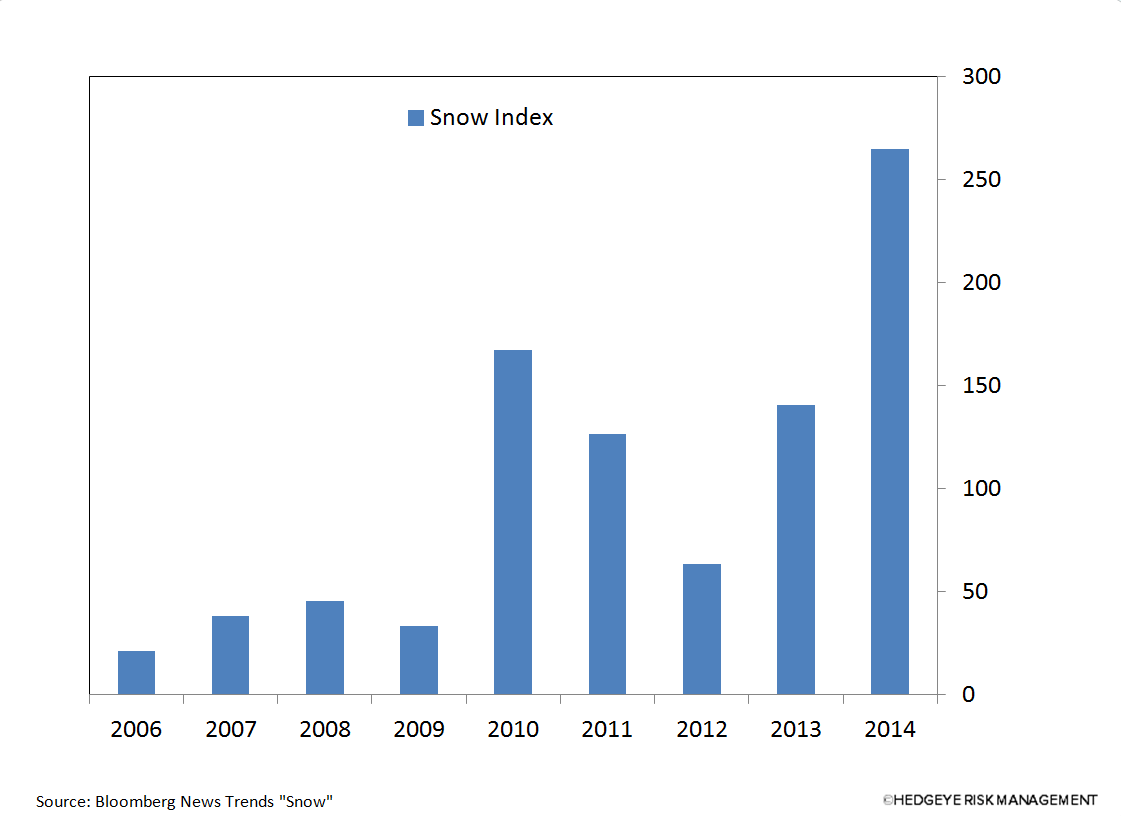

HCA – HCA traded down 4% this week and is now 9% from its YTD high reached last week. Compared to the S&P 500 (which was down roughly 2% over the same period) HCA has been clobbered. What we heard this week as an explanation for the weakness were comments from a number of companies who spoke at an investor conference this week, including HCA. HCA did not talk about Q1 or weather in their presentation, but many others did. While many were asked about weather related headwinds to Q114 results, we would characterize the responses as largely benign and at least consistent with comments made on Q4 earnings calls.

Taking a look at how the winter of 2014 compares to past winters, we indexed the number of snow related news stories as sourced in Bloomberg News Trends over the last several years. By that metric 2014 is significantly worse than any year since 2006.

But after the snow melts, we are expecting procedure volume to come back.

The best indicator we’ve found for surgical volume continues to forecast accelerating procedures. Our conclusion is that the weather headwind is well known, temperatures will rise, the snow will melt, and the underlying strength we saw in 2H13, at least after a snow-weakened January, is likely to continue.

LO – This week Lorillard bounced around on news that Imperial Tobacco Group unit Fortem Ventures has sued LO & NJOY and 9 other e-cig makers on infringement of its intellectual property; on rumors that BAT is considering buying the remaining stake in RAI (it currently owns 42%); and following last week’s rumor that Reynolds American (RAI) is considering acquiring LO. On this last point, we believe a RAI takeout of LO may be unlikely due to antitrust issues – combined the entity would own 67% of the U.S. menthol market.

On the e-cig suit, we’d expect it to be dismissed, as such cases have largely been in the past, on the inability to patent e-cigarette technology. Also keep in mind many companies in the industry are not seeking patents given the rapid pace of technological advancement versus the very long lead time (1-2 years) to get a patent approved.

OC – Owens Corning was added to Investing Ideas earlier this week. Click here to read the full report from Industrials Sector Head Jay Van Sciver.

RH – Williams Sonoma (WSM) released its earnings Wednesday after the close, and while it’s not a perfect comparison to Restoration Hardware – the print does provide a sneak peek behind the curtain on the health of the industry. WSM’s 10.4% comp (the street was looking for 4.6%) was driven by a big beat from Direct-to-Consumer, with considerable strength in the furniture concepts. This is the first meaningful beat we've seen this quarter by any retailer and it was possible for two reasons:

- E-commerce penetration, which like RH accounts for nearly 50% of sales, offset weather induced traffic declines and

- Furniture sales are more immune to inconsistent traffic patterns than impulse categories.

One key difference between the two names is Holiday strategy. WSM is much more dependent on Holiday and gift giving categories which forced its brands to be price competitive in order to compete in the promotional Holiday environment. The strategy fueled the top line, but margins came under considerable pressure.

Restoration Hardware is far less dependent on these categories, which gives us confidence in our modest 4Q margin expansion assumptions.

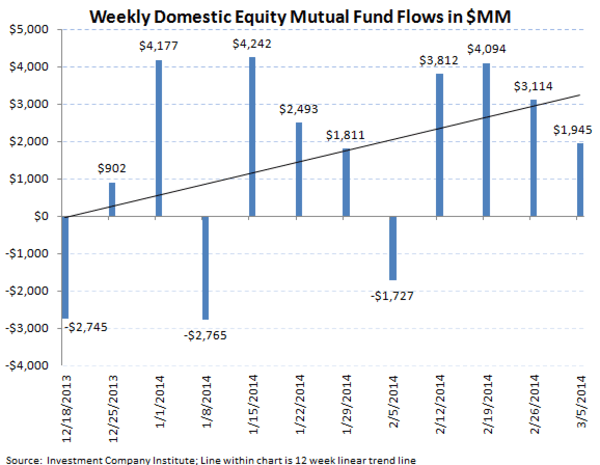

TROW – Financials analyst Jonathan Casteleyn notes that total equity mutual funds produced another strong week of inflow with $5.3 billion of net subscriptions, a slight acceleration from the $4.9 billion inflow the week prior. These flows continue to support our bullish case on T Rowe Price.

Casteleyn considers TROW to be one of the best run asset management companies in the sector along with BlackRock.

ZQK – Below is a brief overview of where we are in the Quiksilver timeline. We see one more quarter of restructuring before the ZQK story becomes about top-line growth.

- 4Q12-2Q13: Hire or replace 7 out of the 8 members of the executive management team. Layout initial restructuring and cost-cutting plan.

- 3Q/4Q13: Begin disposal of non-core assets, rationalize distribution, and execute on initial cost cutting plan. Lay out plans to begin to finally start to grow the business.

- 1Q/2Q14: Continue to drive cost reductions. Begin SKU rationalization to materially cut inventory – which should be a theme in 2014. In 1Q, sales should pick up sequentially from what we saw in 4Q – which shouldn’t be tough given that sales were -15%. But keep in mind that Quiksilver and Roxy are cycling through product discontinuations and were essentially flat in 4Q, it was aggressive clearance of DC inventory that drove the top line down. We have maybe another quarter of this, and then it’s done.

- 3Q/4Q14: ZQK returns to a consistent growth trajectory – something that we have not seen from ZQK in well over 5 years.

* * * * * * *

Click on each title below to unlock the content from Hedgeye analysts.

Darden: Are We Being Mushroomed?

Mushrooms can tolerate some light, but they thrive best in the dark while they grow in composted manure. If you are being “mushroomed,” you are likely being left in the dark and fed a steady diet of offal. Managing Director Howard Penney hopes this is not an accurate metaphor for Darden’s independent Directors.

Linn Energy: The Short Case Is As Strong As Ever

If it wasn’t for companies like LINN Energy (LINE, LNCO), this job wouldn’t be any fun writes Managing Director Kevin Kaiser… We’ve had SHORT LNCO on our Best Ideas List since 3/21/13 ($38.60/share), and it’s been quite the roller coaster.

Industrials Fishfinder: Who Is Overinvesting Now?

Looking at the recent declines in iron ore and copper prices, we are reminded of how challenging capacity additions can be in capital intensive industries. Industrials Sector Head Jay Van Sciver provides a deep dive into this and the attendant market implications.